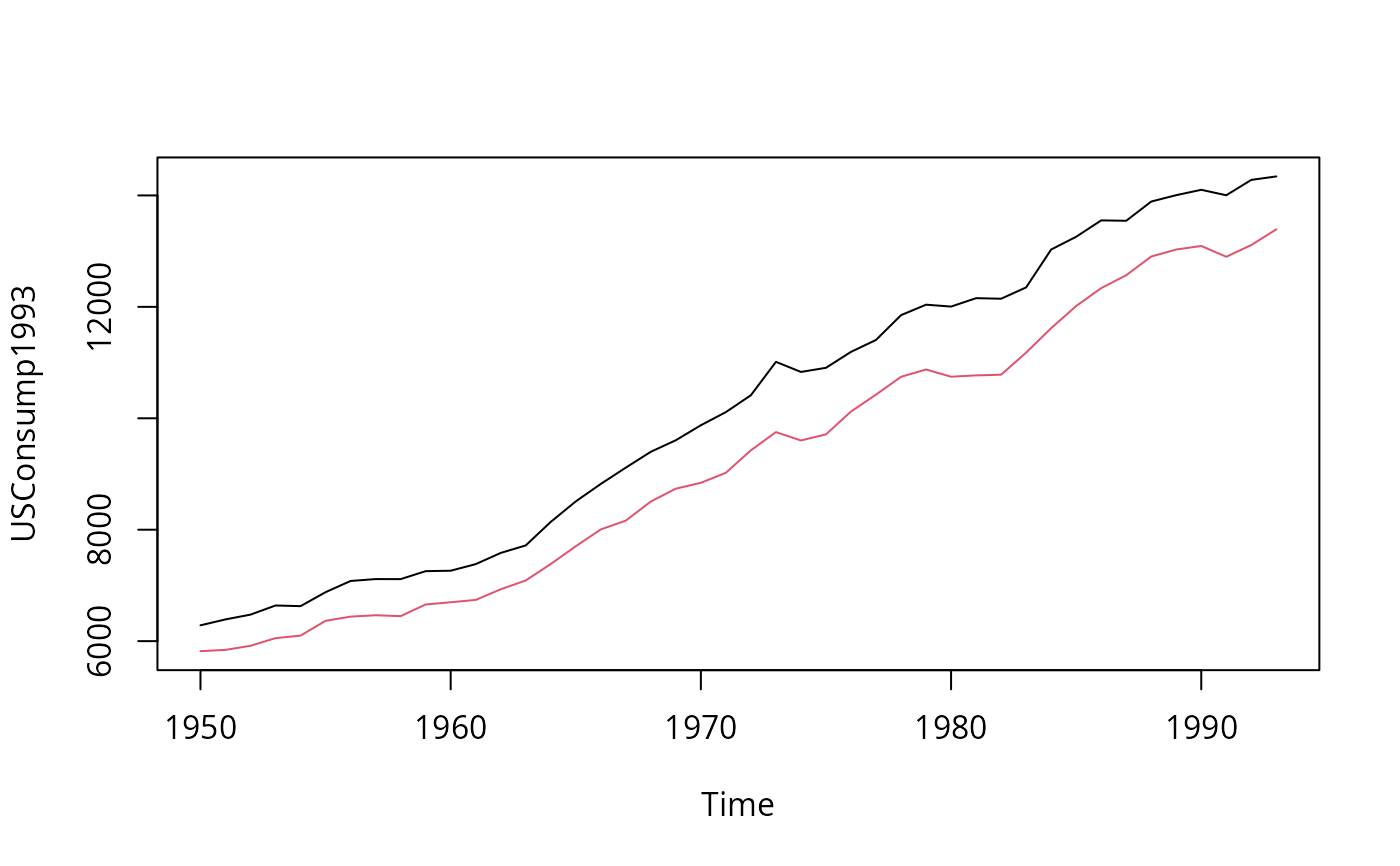

US Consumption Data (1950–1993)

USConsump1993.RdTime series data on US income and consumption expenditure, 1950–1993.

Usage

data("USConsump1993")Format

An annual multiple time series from 1950 to 1993 with 2 variables.

- income

Disposable personal income (in 1987 USD).

- expenditure

Personal consumption expenditures (in 1987 USD).

Examples

## data from Baltagi (2002)

data("USConsump1993", package = "AER")

plot(USConsump1993, plot.type = "single", col = 1:2)

## Chapter 5 (p. 122-125)

fm <- lm(expenditure ~ income, data = USConsump1993)

summary(fm)

#>

#> Call:

#> lm(formula = expenditure ~ income, data = USConsump1993)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -294.52 -67.02 4.64 90.02 325.84

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -65.795821 90.990824 -0.723 0.474

#> income 0.915623 0.008648 105.874 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 153.6 on 42 degrees of freedom

#> Multiple R-squared: 0.9963, Adjusted R-squared: 0.9962

#> F-statistic: 1.121e+04 on 1 and 42 DF, p-value: < 2.2e-16

#>

## Durbin-Watson test (p. 122)

dwtest(fm)

#>

#> Durbin-Watson test

#>

#> data: fm

#> DW = 0.46078, p-value = 3.274e-11

#> alternative hypothesis: true autocorrelation is greater than 0

#>

## Breusch-Godfrey test (Table 5.4, p. 124)

bgtest(fm)

#>

#> Breusch-Godfrey test for serial correlation of order up to 1

#>

#> data: fm

#> LM test = 24.901, df = 1, p-value = 6.034e-07

#>

## Newey-West standard errors (Table 5.5, p. 125)

coeftest(fm, vcov = NeweyWest(fm, lag = 3, prewhite = FALSE, adjust = TRUE))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -65.795821 133.345400 -0.4934 0.6243

#> income 0.915623 0.015458 59.2319 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Chapter 8

library("strucchange")

## Recursive residuals

rr <- recresid(fm)

rr

#> [1] 24.900681 30.354827 50.893291 63.260389 -49.805907 -28.404311

#> [7] -31.520559 53.194256 67.696114 -2.646556 9.679147 39.658827

#> [13] -40.126557 -30.260756 2.605633 -78.941467 27.185066 64.363195

#> [19] -64.906717 -71.641013 70.095867 -113.475323 -85.633171 -29.427630

#> [25] 128.328459 220.693133 126.591749 78.394247 -25.955574 -124.178686

#> [31] -90.845193 127.830581 -30.794629 159.780872 201.707127 405.310561

#> [37] 390.953841 373.370919 316.431235 188.109683 134.461285 339.300414

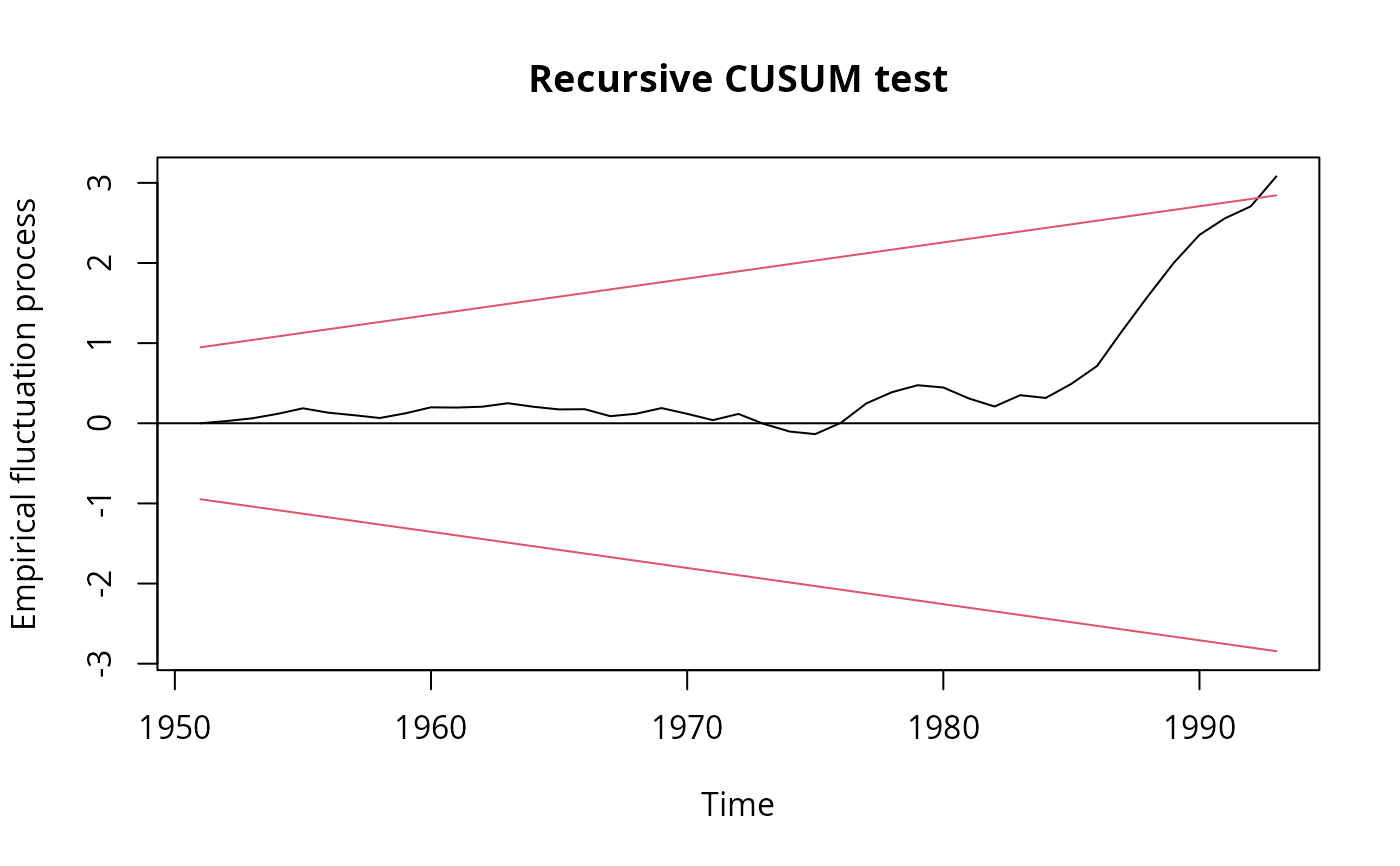

## Recursive CUSUM test

rcus <- efp(expenditure ~ income, data = USConsump1993)

plot(rcus)

## Chapter 5 (p. 122-125)

fm <- lm(expenditure ~ income, data = USConsump1993)

summary(fm)

#>

#> Call:

#> lm(formula = expenditure ~ income, data = USConsump1993)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -294.52 -67.02 4.64 90.02 325.84

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -65.795821 90.990824 -0.723 0.474

#> income 0.915623 0.008648 105.874 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 153.6 on 42 degrees of freedom

#> Multiple R-squared: 0.9963, Adjusted R-squared: 0.9962

#> F-statistic: 1.121e+04 on 1 and 42 DF, p-value: < 2.2e-16

#>

## Durbin-Watson test (p. 122)

dwtest(fm)

#>

#> Durbin-Watson test

#>

#> data: fm

#> DW = 0.46078, p-value = 3.274e-11

#> alternative hypothesis: true autocorrelation is greater than 0

#>

## Breusch-Godfrey test (Table 5.4, p. 124)

bgtest(fm)

#>

#> Breusch-Godfrey test for serial correlation of order up to 1

#>

#> data: fm

#> LM test = 24.901, df = 1, p-value = 6.034e-07

#>

## Newey-West standard errors (Table 5.5, p. 125)

coeftest(fm, vcov = NeweyWest(fm, lag = 3, prewhite = FALSE, adjust = TRUE))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -65.795821 133.345400 -0.4934 0.6243

#> income 0.915623 0.015458 59.2319 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Chapter 8

library("strucchange")

## Recursive residuals

rr <- recresid(fm)

rr

#> [1] 24.900681 30.354827 50.893291 63.260389 -49.805907 -28.404311

#> [7] -31.520559 53.194256 67.696114 -2.646556 9.679147 39.658827

#> [13] -40.126557 -30.260756 2.605633 -78.941467 27.185066 64.363195

#> [19] -64.906717 -71.641013 70.095867 -113.475323 -85.633171 -29.427630

#> [25] 128.328459 220.693133 126.591749 78.394247 -25.955574 -124.178686

#> [31] -90.845193 127.830581 -30.794629 159.780872 201.707127 405.310561

#> [37] 390.953841 373.370919 316.431235 188.109683 134.461285 339.300414

## Recursive CUSUM test

rcus <- efp(expenditure ~ income, data = USConsump1993)

plot(rcus)

sctest(rcus)

#>

#> Recursive CUSUM test

#>

#> data: rcus

#> S = 1.0267, p-value = 0.02707

#>

## Harvey-Collier test

harvtest(fm)

#>

#> Harvey-Collier test

#>

#> data: fm

#> HC = 3.0802, df = 41, p-value = 0.003685

#>

## NOTE" Mistake in Baltagi (2002) who computes

## the t-statistic incorrectly as 0.0733 via

mean(rr)/sd(rr)/sqrt(length(rr))

#> [1] 0.07333754

## whereas it should be (as in harvtest)

mean(rr)/sd(rr) * sqrt(length(rr))

#> [1] 3.080177

## Rainbow test

raintest(fm, center = 23)

#>

#> Rainbow test

#>

#> data: fm

#> Rain = 4.1448, df1 = 22, df2 = 20, p-value = 0.001116

#>

## J test for non-nested models

library("dynlm")

fm1 <- dynlm(expenditure ~ income + L(income), data = USConsump1993)

fm2 <- dynlm(expenditure ~ income + L(expenditure), data = USConsump1993)

jtest(fm1, fm2)

#> J test

#>

#> Model 1: expenditure ~ income + L(income)

#> Model 2: expenditure ~ income + L(expenditure)

#> Estimate Std. Error t value Pr(>|t|)

#> M1 + fitted(M2) 1.6378 0.20984 7.8051 1.726e-09 ***

#> M2 + fitted(M1) -2.5419 0.61603 -4.1262 0.0001874 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

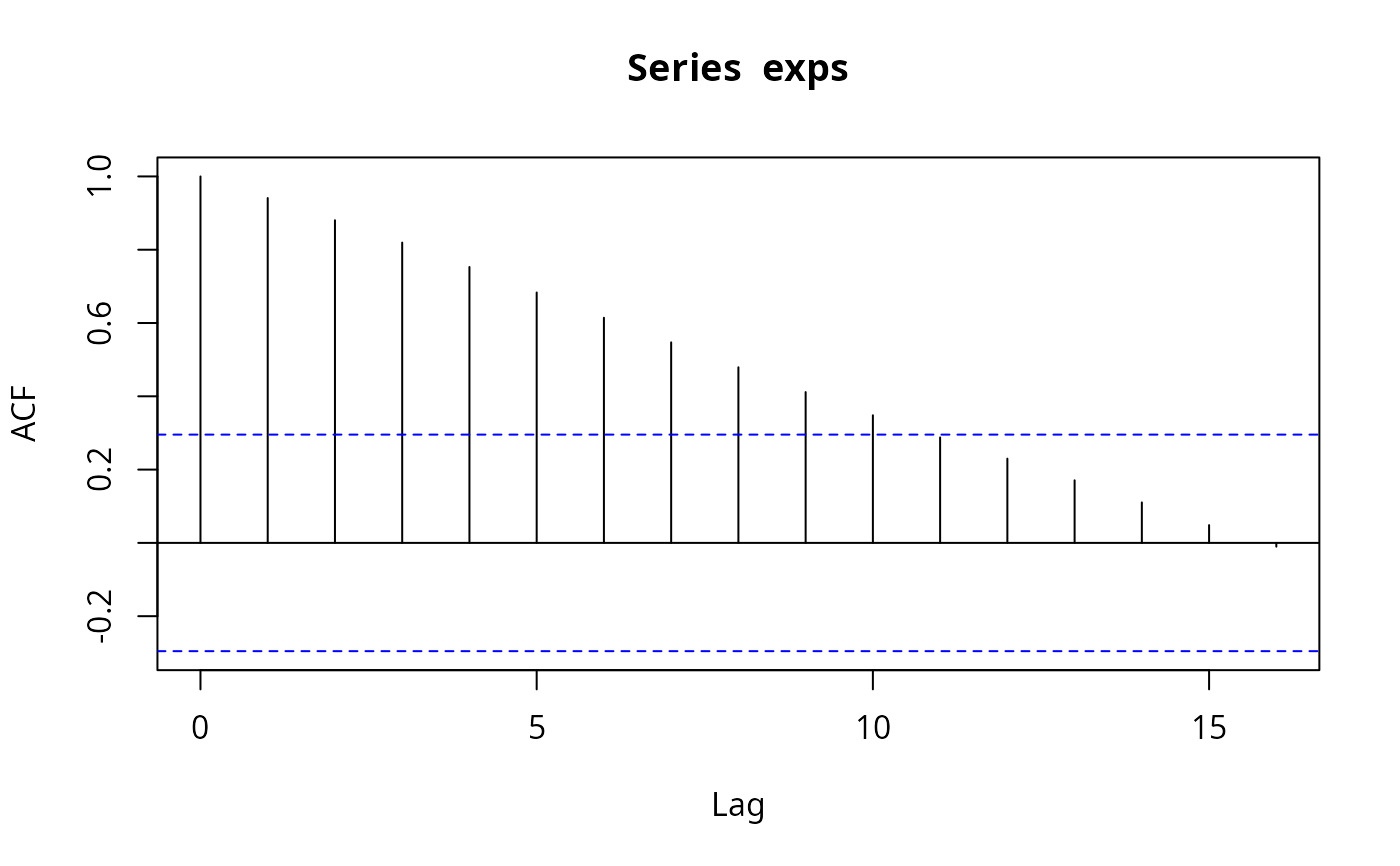

## Chapter 14

## ACF and PACF for expenditures and first differences

exps <- USConsump1993[, "expenditure"]

(acf(exps))

sctest(rcus)

#>

#> Recursive CUSUM test

#>

#> data: rcus

#> S = 1.0267, p-value = 0.02707

#>

## Harvey-Collier test

harvtest(fm)

#>

#> Harvey-Collier test

#>

#> data: fm

#> HC = 3.0802, df = 41, p-value = 0.003685

#>

## NOTE" Mistake in Baltagi (2002) who computes

## the t-statistic incorrectly as 0.0733 via

mean(rr)/sd(rr)/sqrt(length(rr))

#> [1] 0.07333754

## whereas it should be (as in harvtest)

mean(rr)/sd(rr) * sqrt(length(rr))

#> [1] 3.080177

## Rainbow test

raintest(fm, center = 23)

#>

#> Rainbow test

#>

#> data: fm

#> Rain = 4.1448, df1 = 22, df2 = 20, p-value = 0.001116

#>

## J test for non-nested models

library("dynlm")

fm1 <- dynlm(expenditure ~ income + L(income), data = USConsump1993)

fm2 <- dynlm(expenditure ~ income + L(expenditure), data = USConsump1993)

jtest(fm1, fm2)

#> J test

#>

#> Model 1: expenditure ~ income + L(income)

#> Model 2: expenditure ~ income + L(expenditure)

#> Estimate Std. Error t value Pr(>|t|)

#> M1 + fitted(M2) 1.6378 0.20984 7.8051 1.726e-09 ***

#> M2 + fitted(M1) -2.5419 0.61603 -4.1262 0.0001874 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

## Chapter 14

## ACF and PACF for expenditures and first differences

exps <- USConsump1993[, "expenditure"]

(acf(exps))

#>

#> Autocorrelations of series ‘exps’, by lag

#>

#> 0 1 2 3 4 5 6 7 8 9 10

#> 1.000 0.941 0.880 0.820 0.753 0.683 0.614 0.547 0.479 0.412 0.348

#> 11 12 13 14 15 16

#> 0.288 0.230 0.171 0.110 0.049 -0.010

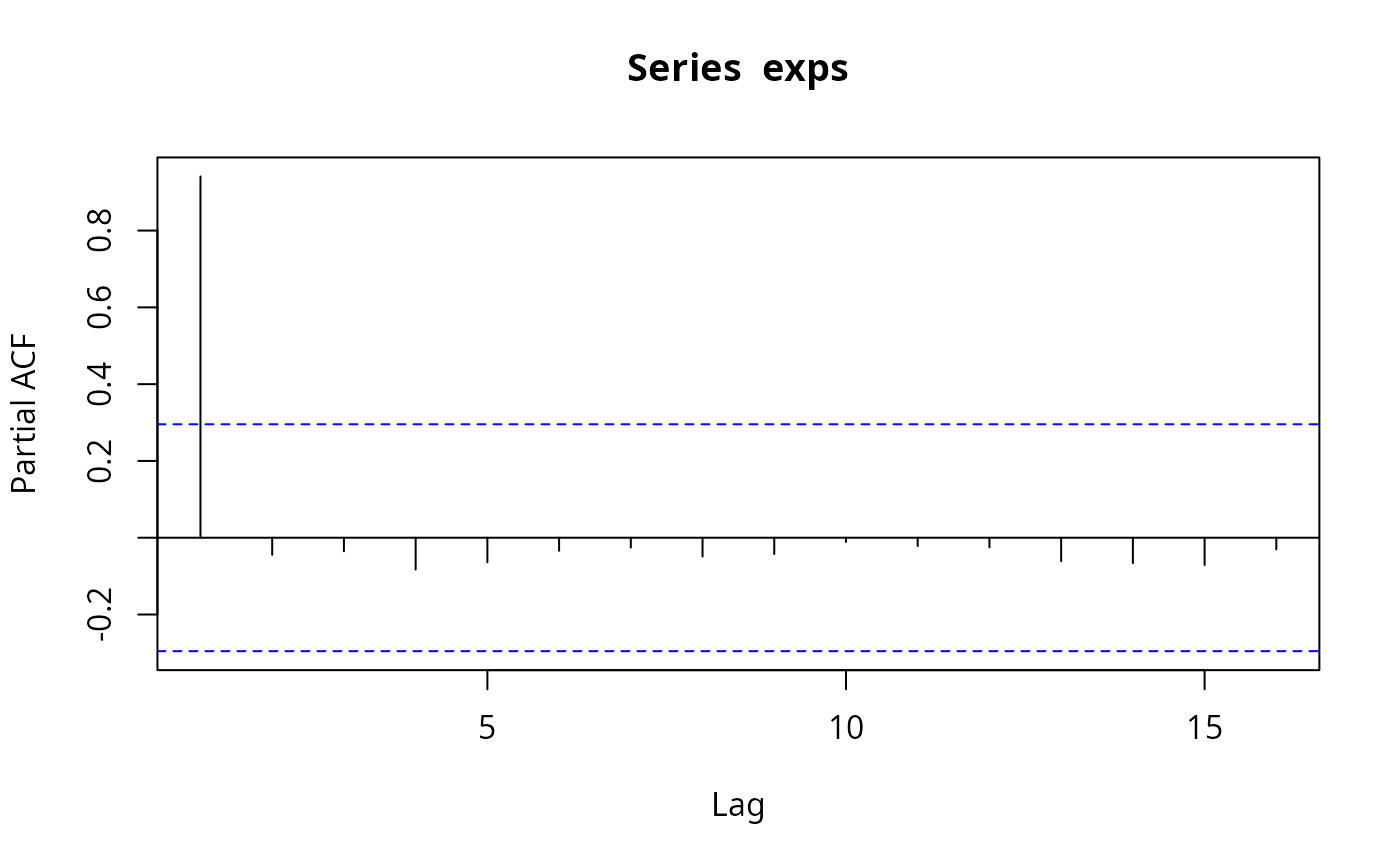

(pacf(exps))

#>

#> Autocorrelations of series ‘exps’, by lag

#>

#> 0 1 2 3 4 5 6 7 8 9 10

#> 1.000 0.941 0.880 0.820 0.753 0.683 0.614 0.547 0.479 0.412 0.348

#> 11 12 13 14 15 16

#> 0.288 0.230 0.171 0.110 0.049 -0.010

(pacf(exps))

#>

#> Partial autocorrelations of series ‘exps’, by lag

#>

#> 1 2 3 4 5 6 7 8 9 10 11

#> 0.941 -0.045 -0.035 -0.083 -0.064 -0.034 -0.025 -0.049 -0.043 -0.011 -0.022

#> 12 13 14 15 16

#> -0.025 -0.061 -0.066 -0.071 -0.030

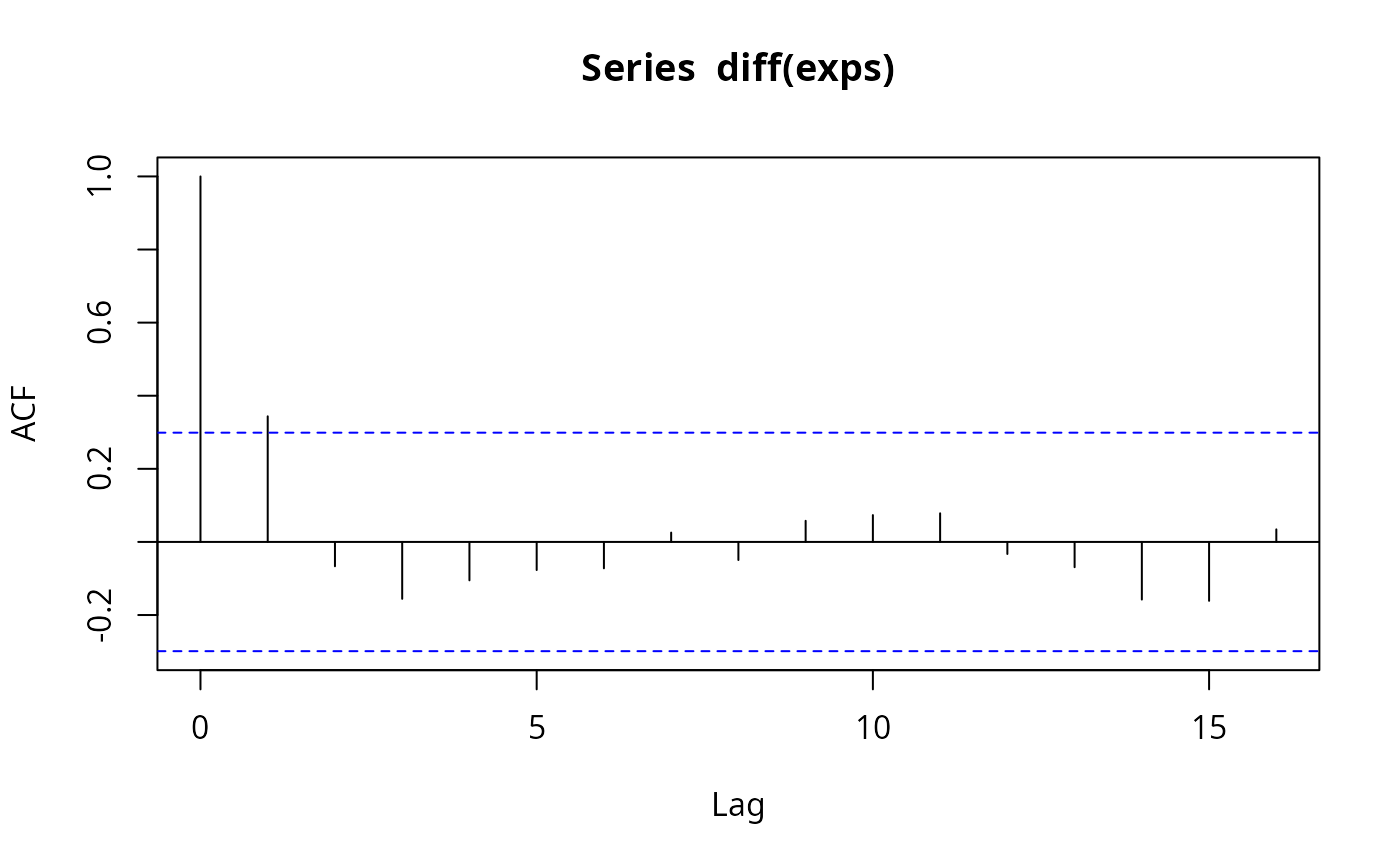

(acf(diff(exps)))

#>

#> Partial autocorrelations of series ‘exps’, by lag

#>

#> 1 2 3 4 5 6 7 8 9 10 11

#> 0.941 -0.045 -0.035 -0.083 -0.064 -0.034 -0.025 -0.049 -0.043 -0.011 -0.022

#> 12 13 14 15 16

#> -0.025 -0.061 -0.066 -0.071 -0.030

(acf(diff(exps)))

#>

#> Autocorrelations of series ‘diff(exps)’, by lag

#>

#> 0 1 2 3 4 5 6 7 8 9 10

#> 1.000 0.344 -0.067 -0.156 -0.105 -0.077 -0.072 0.026 -0.050 0.058 0.073

#> 11 12 13 14 15 16

#> 0.078 -0.033 -0.069 -0.158 -0.161 0.034

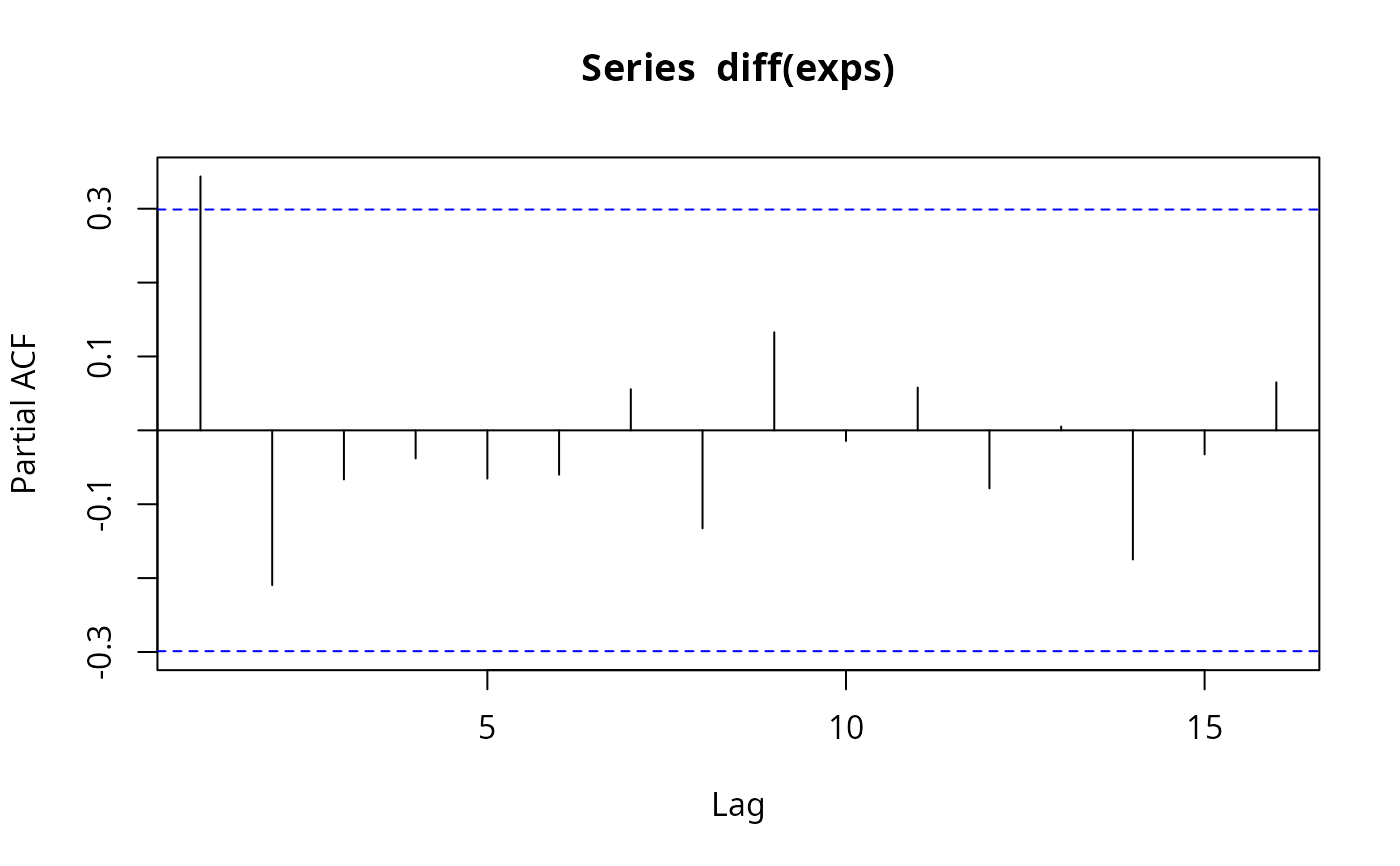

(pacf(diff(exps)))

#>

#> Autocorrelations of series ‘diff(exps)’, by lag

#>

#> 0 1 2 3 4 5 6 7 8 9 10

#> 1.000 0.344 -0.067 -0.156 -0.105 -0.077 -0.072 0.026 -0.050 0.058 0.073

#> 11 12 13 14 15 16

#> 0.078 -0.033 -0.069 -0.158 -0.161 0.034

(pacf(diff(exps)))

#>

#> Partial autocorrelations of series ‘diff(exps)’, by lag

#>

#> 1 2 3 4 5 6 7 8 9 10 11

#> 0.344 -0.209 -0.066 -0.038 -0.065 -0.060 0.056 -0.133 0.133 -0.014 0.058

#> 12 13 14 15 16

#> -0.079 0.005 -0.175 -0.032 0.065

## dynamic regressions, eq. (14.8)

fm <- dynlm(d(exps) ~ I(time(exps) - 1949) + L(exps))

summary(fm)

#>

#> Time series regression with "ts" data:

#> Start = 1951, End = 1993

#>

#> Call:

#> dynlm(formula = d(exps) ~ I(time(exps) - 1949) + L(exps))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -357.76 -78.18 22.49 108.97 201.06

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1048.96039 353.81291 2.965 0.00509 **

#> I(time(exps) - 1949) 39.90164 14.31344 2.788 0.00808 **

#> L(exps) -0.19561 0.07398 -2.644 0.01164 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 147.4 on 40 degrees of freedom

#> Multiple R-squared: 0.1784, Adjusted R-squared: 0.1373

#> F-statistic: 4.343 on 2 and 40 DF, p-value: 0.01963

#>

#>

#> Partial autocorrelations of series ‘diff(exps)’, by lag

#>

#> 1 2 3 4 5 6 7 8 9 10 11

#> 0.344 -0.209 -0.066 -0.038 -0.065 -0.060 0.056 -0.133 0.133 -0.014 0.058

#> 12 13 14 15 16

#> -0.079 0.005 -0.175 -0.032 0.065

## dynamic regressions, eq. (14.8)

fm <- dynlm(d(exps) ~ I(time(exps) - 1949) + L(exps))

summary(fm)

#>

#> Time series regression with "ts" data:

#> Start = 1951, End = 1993

#>

#> Call:

#> dynlm(formula = d(exps) ~ I(time(exps) - 1949) + L(exps))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -357.76 -78.18 22.49 108.97 201.06

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1048.96039 353.81291 2.965 0.00509 **

#> I(time(exps) - 1949) 39.90164 14.31344 2.788 0.00808 **

#> L(exps) -0.19561 0.07398 -2.644 0.01164 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 147.4 on 40 degrees of freedom

#> Multiple R-squared: 0.1784, Adjusted R-squared: 0.1373

#> F-statistic: 4.343 on 2 and 40 DF, p-value: 0.01963

#>