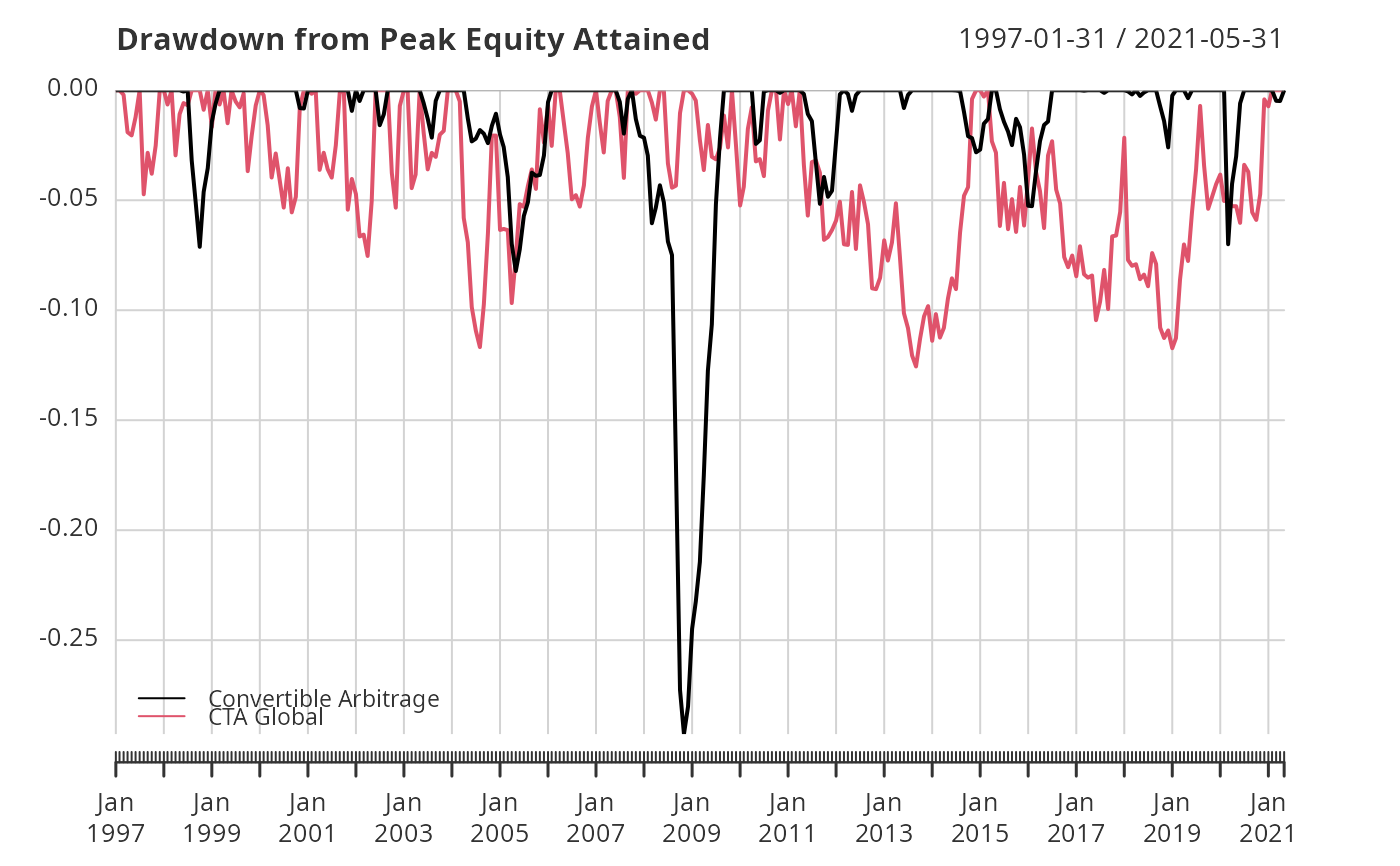

A time series chart demonstrating drawdowns from peak equity attained through time, calculated from periodic returns.

chart.Drawdown(

R,

geometric = TRUE,

legend.loc = NULL,

colorset = (1:12),

plot.engine = "default",

...

)Arguments

- R

an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns

- geometric

utilize geometric chaining (TRUE) or simple/arithmetic chaining (FALSE) to aggregate returns, default TRUE

- legend.loc

places a legend into one of nine locations on the chart: bottomright, bottom, bottomleft, left, topleft, top, topright, right, or center.

- colorset

color palette to use, set by default to rational choices

- plot.engine

choose the plot engine you wish to use: ggplot2, plotly,dygraph,googlevis and default

- ...

any other passthru parameters

Details

Any time the cumulative returns dips below the maximum cumulative returns, it's a drawdown. Drawdowns are measured as a percentage of that maximum cumulative return, in effect, measured from peak equity.

References

Bacon, C. Practical Portfolio Performance Measurement and

Attribution. Wiley. 2004. p. 88