Downside Risk Summary: Statistics and Stylized Facts

Source:R/table.DownsideRisk.R

table.DownsideRisk.RdCreates a table of estimates of downside risk measures for comparison across multiple instruments or funds.

table.DownsideRisk(

R,

ci = 0.95,

scale = NA,

Rf = 0,

MAR = 0.1/12,

p = 0.95,

digits = 4

)Arguments

- R

an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns

- ci

confidence interval, defaults to 95%

- scale

number of periods in a year (daily scale = 252, monthly scale = 12, quarterly scale = 4)

- Rf

risk free rate, in same period as your returns

- MAR

Minimum Acceptable Return, in the same periodicity as your returns

- p

confidence level for calculation, default p=.99

- digits

number of digits to round results to

See also

Examples

data(edhec)

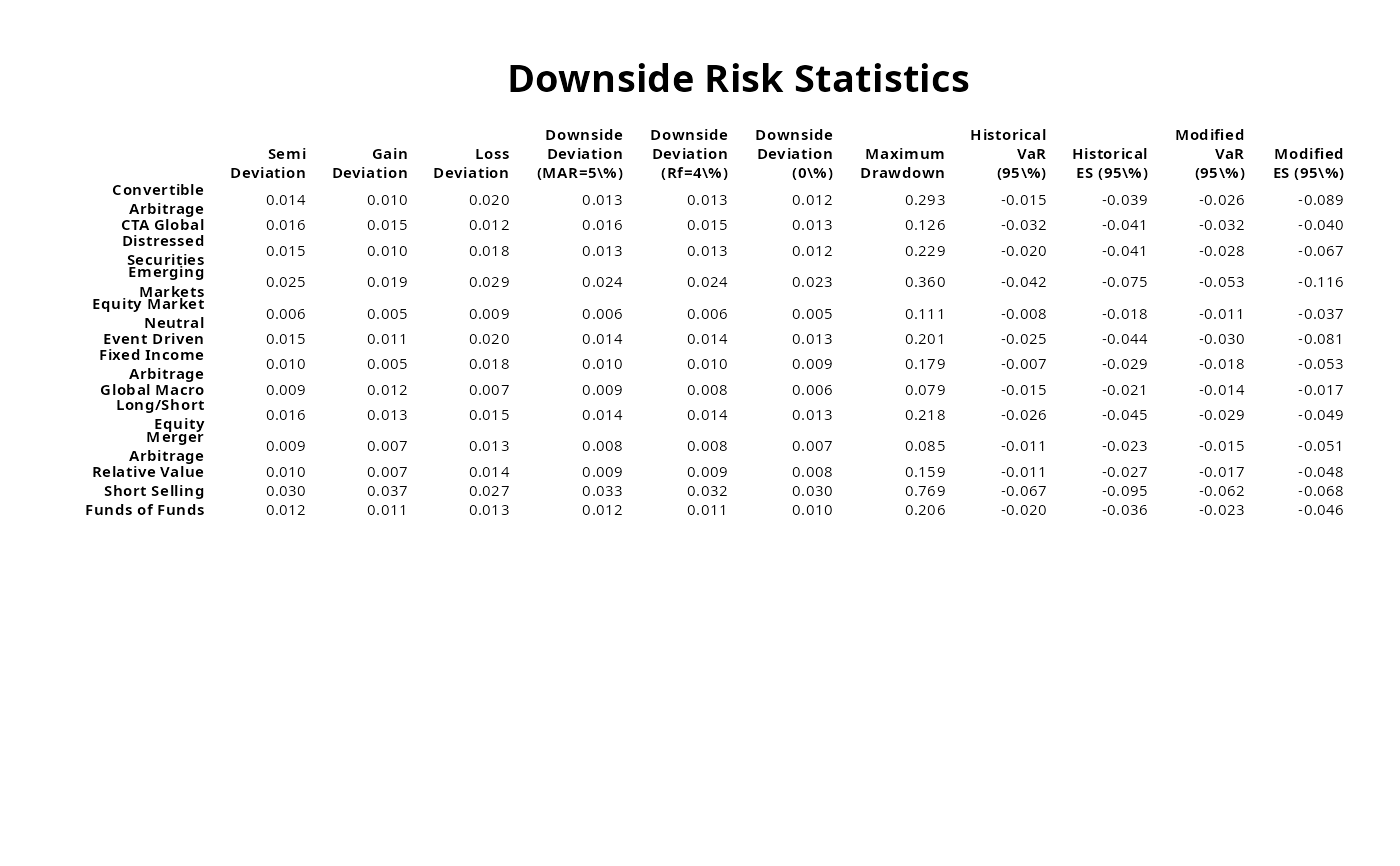

table.DownsideRisk(edhec, Rf=.04/12, MAR =.05/12, p=.95)

#> Convertible Arbitrage CTA Global

#> Semi Deviation 0.0136 0.0156

#> Gain Deviation 0.0095 0.0153

#> Loss Deviation 0.0203 0.0123

#> Downside Deviation (MAR=5%) 0.0131 0.0156

#> Downside Deviation (Rf=4%) 0.0128 0.0151

#> Downside Deviation (0%) 0.0118 0.0132

#> Maximum Drawdown 0.2927 0.1256

#> Historical VaR (95%) -0.0151 -0.0315

#> Historical ES (95%) -0.0388 -0.0406

#> Modified VaR (95%) -0.0257 -0.0320

#> Modified ES (95%) -0.0894 -0.0404

#> Distressed Securities Emerging Markets

#> Semi Deviation 0.0146 0.0255

#> Gain Deviation 0.0099 0.0186

#> Loss Deviation 0.0177 0.0287

#> Downside Deviation (MAR=5%) 0.0134 0.0244

#> Downside Deviation (Rf=4%) 0.0131 0.0240

#> Downside Deviation (0%) 0.0119 0.0226

#> Maximum Drawdown 0.2292 0.3598

#> Historical VaR (95%) -0.0198 -0.0423

#> Historical ES (95%) -0.0413 -0.0754

#> Modified VaR (95%) -0.0280 -0.0534

#> Modified ES (95%) -0.0673 -0.1157

#> Equity Market Neutral Event Driven

#> Semi Deviation 0.0065 0.0154

#> Gain Deviation 0.0051 0.0106

#> Loss Deviation 0.0093 0.0198

#> Downside Deviation (MAR=5%) 0.0064 0.0143

#> Downside Deviation (Rf=4%) 0.0061 0.0140

#> Downside Deviation (0%) 0.0050 0.0129

#> Maximum Drawdown 0.1108 0.2008

#> Historical VaR (95%) -0.0084 -0.0255

#> Historical ES (95%) -0.0175 -0.0445

#> Modified VaR (95%) -0.0110 -0.0296

#> Modified ES (95%) -0.0367 -0.0811

#> Fixed Income Arbitrage Global Macro

#> Semi Deviation 0.0099 0.0093

#> Gain Deviation 0.0055 0.0119

#> Loss Deviation 0.0179 0.0067

#> Downside Deviation (MAR=5%) 0.0098 0.0085

#> Downside Deviation (Rf=4%) 0.0096 0.0080

#> Downside Deviation (0%) 0.0088 0.0063

#> Maximum Drawdown 0.1788 0.0792

#> Historical VaR (95%) -0.0072 -0.0149

#> Historical ES (95%) -0.0291 -0.0211

#> Modified VaR (95%) -0.0177 -0.0138

#> Modified ES (95%) -0.0531 -0.0170

#> Long/Short Equity Merger Arbitrage Relative Value

#> Semi Deviation 0.0155 0.0089 0.0097

#> Gain Deviation 0.0132 0.0073 0.0066

#> Loss Deviation 0.0154 0.0125 0.0137

#> Downside Deviation (MAR=5%) 0.0143 0.0084 0.0091

#> Downside Deviation (Rf=4%) 0.0139 0.0081 0.0088

#> Downside Deviation (0%) 0.0125 0.0070 0.0078

#> Maximum Drawdown 0.2182 0.0850 0.1594

#> Historical VaR (95%) -0.0262 -0.0107 -0.0114

#> Historical ES (95%) -0.0448 -0.0233 -0.0271

#> Modified VaR (95%) -0.0295 -0.0150 -0.0174

#> Modified ES (95%) -0.0486 -0.0513 -0.0475

#> Short Selling Funds of Funds

#> Semi Deviation 0.0296 0.0120

#> Gain Deviation 0.0372 0.0105

#> Loss Deviation 0.0271 0.0132

#> Downside Deviation (MAR=5%) 0.0326 0.0118

#> Downside Deviation (Rf=4%) 0.0322 0.0114

#> Downside Deviation (0%) 0.0303 0.0101

#> Maximum Drawdown 0.7687 0.2059

#> Historical VaR (95%) -0.0668 -0.0203

#> Historical ES (95%) -0.0948 -0.0357

#> Modified VaR (95%) -0.0622 -0.0231

#> Modified ES (95%) -0.0675 -0.0459

result=t(table.DownsideRisk(edhec, Rf=.04/12, MAR =.05/12, p=.95))

# don't test on CRAN, since it requires Suggested packages

require("Hmisc")

textplot(format.df(result, na.blank=TRUE, numeric.dollar=FALSE,

cdec=rep(3,dim(result)[2])), rmar = 0.8, cmar = 1.5,

max.cex=.9, halign = "center", valign = "top", row.valign="center",

wrap.rownames=15, wrap.colnames=10, mar = c(0,0,3,0)+0.1)

title(main="Downside Risk Statistics")