Data and Examples from Stock and Watson (2007)

StockWatson2007.RdThis manual page collects a list of examples from the book. Some solutions might not be exact and the list is certainly not complete. If you have suggestions for improvement (preferably in the form of code), please contact the package maintainer.

References

Stock, J.H. and Watson, M.W. (2007). Introduction to Econometrics, 2nd ed. Boston: Addison Wesley.

See also

CartelStability, CASchools, CigarettesSW,

CollegeDistance, CPSSW04, CPSSW3, CPSSW8,

CPSSW9298, CPSSW9204, CPSSWEducation,

Fatalities, Fertility, Fertility2, FrozenJuice,

GrowthSW, Guns, HealthInsurance, HMDA,

Journals, MASchools, NYSESW, ResumeNames,

SmokeBan, SportsCards, STAR, TeachingRatings,

USMacroSW, USMacroSWM, USMacroSWQ, USSeatBelts,

USStocksSW, WeakInstrument

Examples

###############################

## Current Population Survey ##

###############################

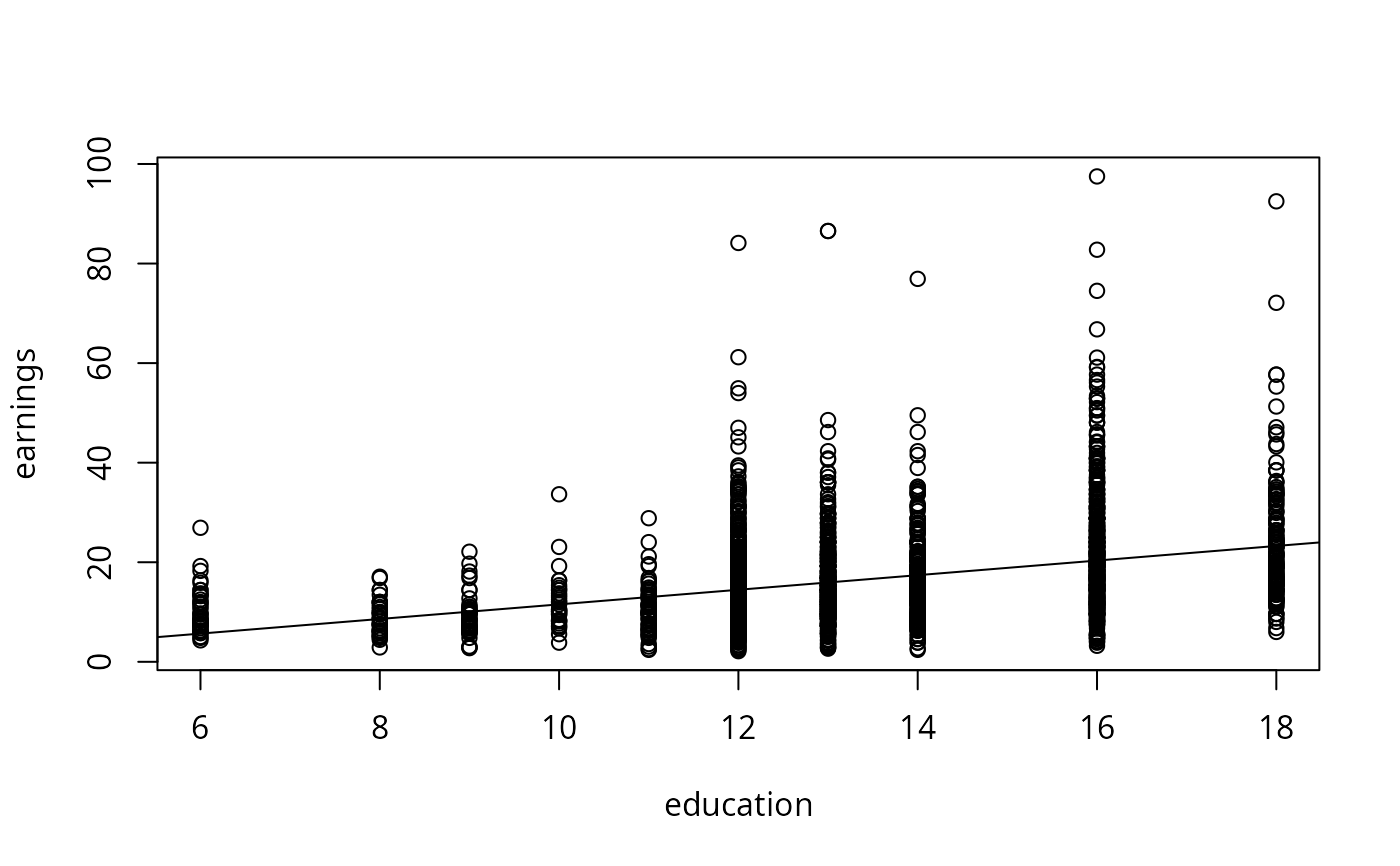

## p. 165

data("CPSSWEducation", package = "AER")

plot(earnings ~ education, data = CPSSWEducation)

fm <- lm(earnings ~ education, data = CPSSWEducation)

coeftest(fm, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -3.134371 0.925571 -3.3864 0.0007174 ***

#> education 1.466925 0.071918 20.3972 < 2.2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

abline(fm)

############################

## California test scores ##

############################

## data and transformations

data("CASchools", package = "AER")

CASchools <- transform(CASchools,

stratio = students/teachers,

score = (math + read)/2

)

## p. 152

fm1 <- lm(score ~ stratio, data = CASchools)

coeftest(fm1, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 698.93295 10.33966 67.597 < 2.2e-16 ***

#> stratio -2.27981 0.51825 -4.399 1.382e-05 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## p. 159

fm2 <- lm(score ~ I(stratio < 20), data = CASchools)

## p. 199

fm3 <- lm(score ~ stratio + english, data = CASchools)

## p. 224

fm4 <- lm(score ~ stratio + expenditure + english, data = CASchools)

## Table 7.1, p. 242 (numbers refer to columns)

fmc3 <- lm(score ~ stratio + english + lunch, data = CASchools)

fmc4 <- lm(score ~ stratio + english + calworks, data = CASchools)

fmc5 <- lm(score ~ stratio + english + lunch + calworks, data = CASchools)

## Equation 8.2, p. 258

fmquad <- lm(score ~ income + I(income^2), data = CASchools)

## Equation 8.11, p. 266

fmcub <- lm(score ~ income + I(income^2) + I(income^3), data = CASchools)

## Equation 8.23, p. 272

fmloglog <- lm(log(score) ~ log(income), data = CASchools)

## Equation 8.24, p. 274

fmloglin <- lm(log(score) ~ income, data = CASchools)

## Equation 8.26, p. 275

fmlinlogcub <- lm(score ~ log(income) + I(log(income)^2) + I(log(income)^3),

data = CASchools)

## Table 8.3, p. 292 (numbers refer to columns)

fmc2 <- lm(score ~ stratio + english + lunch + log(income), data = CASchools)

fmc7 <- lm(score ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch + log(income),

data = CASchools)

#####################################

## Economics journal Subscriptions ##

#####################################

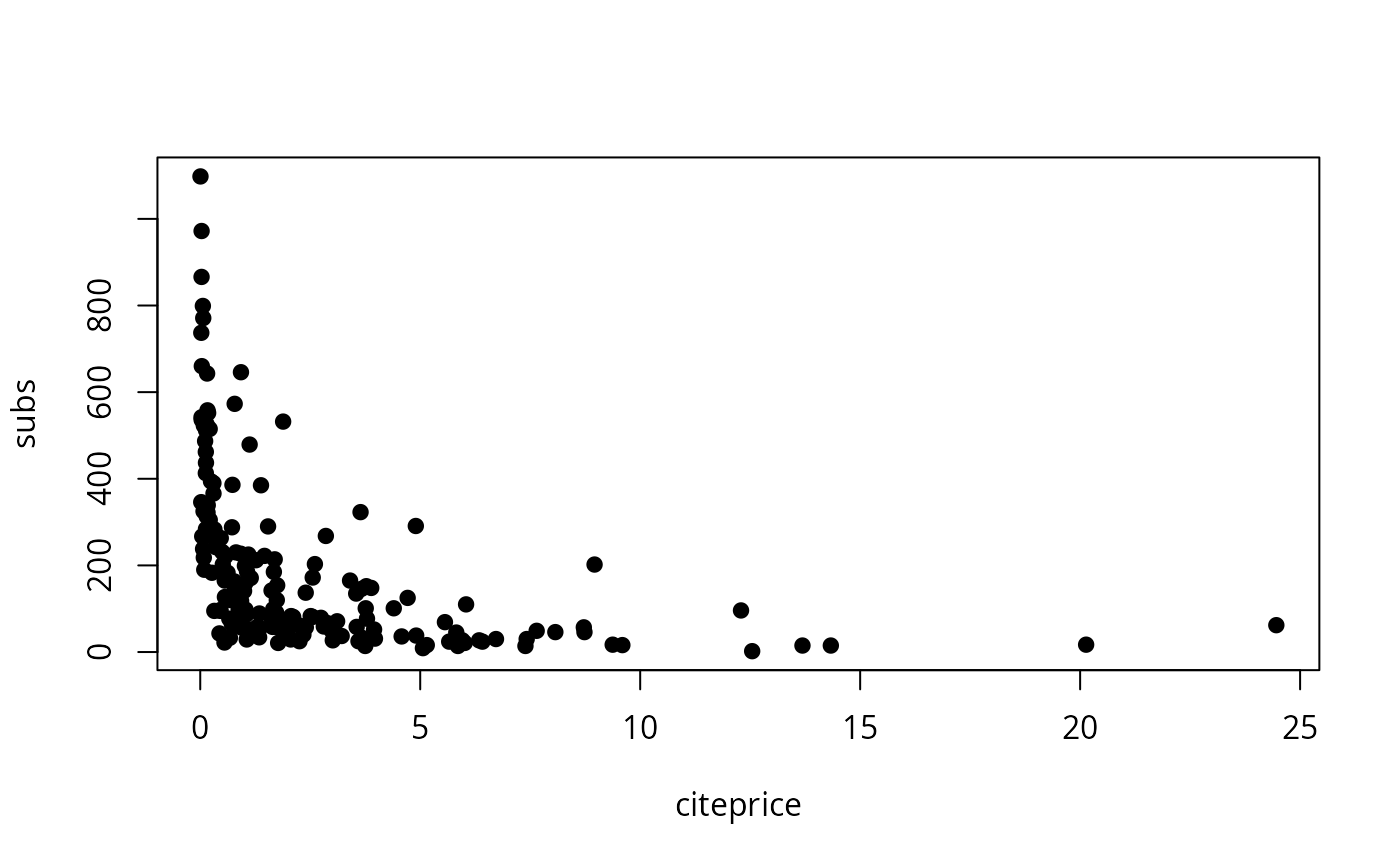

## data and transformed variables

data("Journals", package = "AER")

journals <- Journals[, c("subs", "price")]

journals$citeprice <- Journals$price/Journals$citations

journals$age <- 2000 - Journals$foundingyear

journals$chars <- Journals$charpp*Journals$pages/10^6

## Figure 8.9 (a) and (b)

plot(subs ~ citeprice, data = journals, pch = 19)

############################

## California test scores ##

############################

## data and transformations

data("CASchools", package = "AER")

CASchools <- transform(CASchools,

stratio = students/teachers,

score = (math + read)/2

)

## p. 152

fm1 <- lm(score ~ stratio, data = CASchools)

coeftest(fm1, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 698.93295 10.33966 67.597 < 2.2e-16 ***

#> stratio -2.27981 0.51825 -4.399 1.382e-05 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## p. 159

fm2 <- lm(score ~ I(stratio < 20), data = CASchools)

## p. 199

fm3 <- lm(score ~ stratio + english, data = CASchools)

## p. 224

fm4 <- lm(score ~ stratio + expenditure + english, data = CASchools)

## Table 7.1, p. 242 (numbers refer to columns)

fmc3 <- lm(score ~ stratio + english + lunch, data = CASchools)

fmc4 <- lm(score ~ stratio + english + calworks, data = CASchools)

fmc5 <- lm(score ~ stratio + english + lunch + calworks, data = CASchools)

## Equation 8.2, p. 258

fmquad <- lm(score ~ income + I(income^2), data = CASchools)

## Equation 8.11, p. 266

fmcub <- lm(score ~ income + I(income^2) + I(income^3), data = CASchools)

## Equation 8.23, p. 272

fmloglog <- lm(log(score) ~ log(income), data = CASchools)

## Equation 8.24, p. 274

fmloglin <- lm(log(score) ~ income, data = CASchools)

## Equation 8.26, p. 275

fmlinlogcub <- lm(score ~ log(income) + I(log(income)^2) + I(log(income)^3),

data = CASchools)

## Table 8.3, p. 292 (numbers refer to columns)

fmc2 <- lm(score ~ stratio + english + lunch + log(income), data = CASchools)

fmc7 <- lm(score ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch + log(income),

data = CASchools)

#####################################

## Economics journal Subscriptions ##

#####################################

## data and transformed variables

data("Journals", package = "AER")

journals <- Journals[, c("subs", "price")]

journals$citeprice <- Journals$price/Journals$citations

journals$age <- 2000 - Journals$foundingyear

journals$chars <- Journals$charpp*Journals$pages/10^6

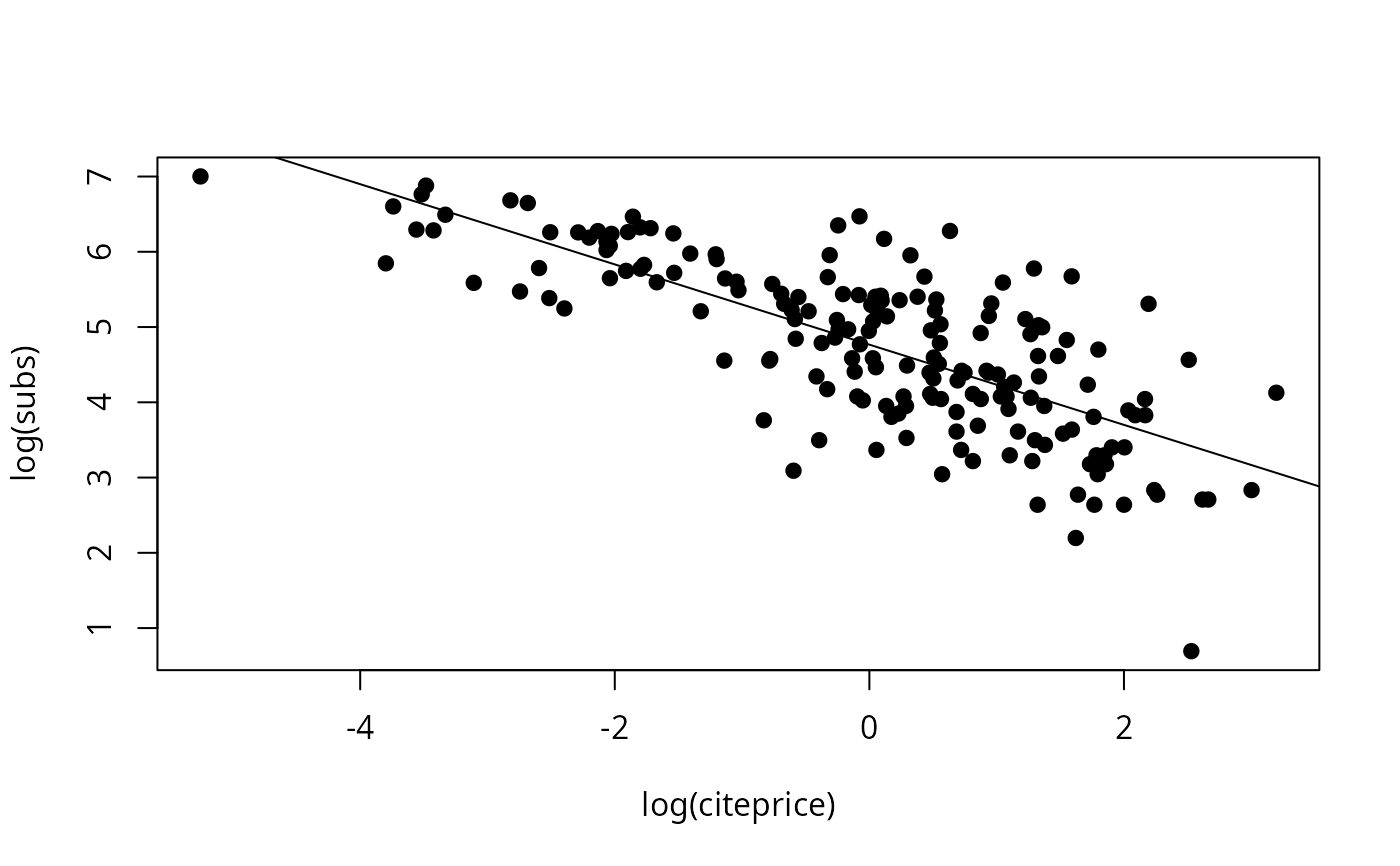

## Figure 8.9 (a) and (b)

plot(subs ~ citeprice, data = journals, pch = 19)

plot(log(subs) ~ log(citeprice), data = journals, pch = 19)

fm1 <- lm(log(subs) ~ log(citeprice), data = journals)

abline(fm1)

plot(log(subs) ~ log(citeprice), data = journals, pch = 19)

fm1 <- lm(log(subs) ~ log(citeprice), data = journals)

abline(fm1)

## Table 8.2, use HC1 for comparability with Stata

fm1 <- lm(subs ~ citeprice, data = log(journals))

fm2 <- lm(subs ~ citeprice + age + chars, data = log(journals))

fm3 <- lm(subs ~ citeprice + I(citeprice^2) + I(citeprice^3) +

age + I(age * citeprice) + chars, data = log(journals))

fm4 <- lm(subs ~ citeprice + age + I(age * citeprice) + chars, data = log(journals))

coeftest(fm1, vcov = vcovHC(fm1, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 4.766212 0.055258 86.253 < 2.2e-16 ***

#> citeprice -0.533053 0.033959 -15.697 < 2.2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm2, vcov = vcovHC(fm2, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.206648 0.379725 8.4447 1.102e-14 ***

#> citeprice -0.407718 0.043717 -9.3262 < 2.2e-16 ***

#> age 0.423649 0.119064 3.5581 0.0004801 ***

#> chars 0.205614 0.097751 2.1035 0.0368474 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm3, vcov = vcovHC(fm3, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.4075956 0.3735992 9.1210 < 2.2e-16 ***

#> citeprice -0.9609365 0.1601349 -6.0008 1.121e-08 ***

#> I(citeprice^2) 0.0165099 0.0254886 0.6477 0.518015

#> I(citeprice^3) 0.0036666 0.0055147 0.6649 0.507008

#> age 0.3730539 0.1176966 3.1696 0.001805 **

#> I(age * citeprice) 0.1557773 0.0518947 3.0018 0.003081 **

#> chars 0.2346178 0.0977318 2.4006 0.017428 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm4, vcov = vcovHC(fm4, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.433521 0.367471 9.3436 < 2.2e-16 ***

#> citeprice -0.898910 0.144648 -6.2144 3.656e-09 ***

#> age 0.373515 0.117527 3.1781 0.0017529 **

#> I(age * citeprice) 0.140959 0.040199 3.5065 0.0005769 ***

#> chars 0.229466 0.096493 2.3781 0.0184822 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

waldtest(fm3, fm4, vcov = vcovHC(fm3, type = "HC1"))

#> Wald test

#>

#> Model 1: subs ~ citeprice + I(citeprice^2) + I(citeprice^3) + age + I(age *

#> citeprice) + chars

#> Model 2: subs ~ citeprice + age + I(age * citeprice) + chars

#> Res.Df Df F Pr(>F)

#> 1 173

#> 2 175 -2 0.249 0.7799

###############################

## Massachusetts test scores ##

###############################

## compare Massachusetts with California

data("MASchools", package = "AER")

data("CASchools", package = "AER")

CASchools <- transform(CASchools,

stratio = students/teachers,

score4 = (math + read)/2

)

## parts of Table 9.1, p. 330

vars <- c("score4", "stratio", "english", "lunch", "income")

cbind(

CA_mean = sapply(CASchools[, vars], mean),

CA_sd = sapply(CASchools[, vars], sd),

MA_mean = sapply(MASchools[, vars], mean),

MA_sd = sapply(MASchools[, vars], sd))

#> CA_mean CA_sd MA_mean MA_sd

#> score4 654.15655 19.053347 709.827273 15.126474

#> stratio 19.64043 1.891812 17.344091 2.276666

#> english 15.76816 18.285927 1.117676 2.900940

#> lunch 44.70524 27.123381 15.315909 15.060068

#> income 15.31659 7.225890 18.746764 5.807637

## Table 9.2, pp. 332--333, numbers refer to columns

MASchools <- transform(MASchools, higheng = english > median(english))

fm1 <- lm(score4 ~ stratio, data = MASchools)

fm2 <- lm(score4 ~ stratio + english + lunch + log(income), data = MASchools)

fm3 <- lm(score4 ~ stratio + english + lunch + income + I(income^2) + I(income^3),

data = MASchools)

fm4 <- lm(score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

income + I(income^2) + I(income^3), data = MASchools)

fm5 <- lm(score4 ~ stratio + higheng + I(higheng * stratio) + lunch +

income + I(income^2) + I(income^3), data = MASchools)

fm6 <- lm(score4 ~ stratio + lunch + income + I(income^2) + I(income^3),

data = MASchools)

## for comparability with Stata use HC1 below

coeftest(fm1, vcov = vcovHC(fm1, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 739.62113 8.60727 85.9298 < 2.2e-16 ***

#> stratio -1.71781 0.49906 -3.4421 0.000692 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm2, vcov = vcovHC(fm2, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 682.431602 11.497244 59.3561 < 2.2e-16 ***

#> stratio -0.689179 0.269973 -2.5528 0.01138 *

#> english -0.410745 0.306377 -1.3407 0.18145

#> lunch -0.521465 0.077659 -6.7148 1.653e-10 ***

#> log(income) 16.529359 3.145722 5.2546 3.566e-07 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm3, vcov = vcovHC(fm3, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 7.4403e+02 2.1318e+01 34.9016 < 2.2e-16 ***

#> stratio -6.4091e-01 2.6848e-01 -2.3872 0.01785 *

#> english -4.3712e-01 3.0332e-01 -1.4411 0.15103

#> lunch -5.8182e-01 9.7353e-02 -5.9764 9.488e-09 ***

#> income -3.0667e+00 2.3525e+00 -1.3036 0.19379

#> I(income^2) 1.6369e-01 8.5330e-02 1.9183 0.05641 .

#> I(income^3) -2.1793e-03 9.7033e-04 -2.2459 0.02574 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm4, vcov = vcovHC(fm4, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 665.4960529 81.3317629 8.1825 2.600e-14 ***

#> stratio 12.4259758 14.0101690 0.8869 0.37613

#> I(stratio^2) -0.6803029 0.7365191 -0.9237 0.35671

#> I(stratio^3) 0.0114737 0.0126663 0.9058 0.36605

#> english -0.4341659 0.2997883 -1.4482 0.14903

#> lunch -0.5872165 0.1040207 -5.6452 5.283e-08 ***

#> income -3.3815370 2.4906830 -1.3577 0.17602

#> I(income^2) 0.1741018 0.0892596 1.9505 0.05244 .

#> I(income^3) -0.0022883 0.0010078 -2.2706 0.02418 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm5, vcov = vcovHC(fm5, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 759.9142249 23.2331213 32.7082 < 2.2e-16 ***

#> stratio -1.0176806 0.3703923 -2.7476 0.006521 **

#> highengTRUE -12.5607339 9.7934588 -1.2826 0.201046

#> I(higheng * stratio) 0.7986123 0.5552225 1.4384 0.151805

#> lunch -0.7085098 0.0908442 -7.7992 2.785e-13 ***

#> income -3.8665072 2.4884002 -1.5538 0.121721

#> I(income^2) 0.1841250 0.0898247 2.0498 0.041612 *

#> I(income^3) -0.0023364 0.0010153 -2.3013 0.022349 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm6, vcov = vcovHC(fm6, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 7.4736e+02 2.0278e+01 36.8563 < 2e-16 ***

#> stratio -6.7188e-01 2.7128e-01 -2.4767 0.01404 *

#> lunch -6.5308e-01 7.2980e-02 -8.9487 < 2e-16 ***

#> income -3.2180e+00 2.3057e+00 -1.3956 0.16427

#> I(income^2) 1.6479e-01 8.4634e-02 1.9471 0.05284 .

#> I(income^3) -2.1550e-03 9.6995e-04 -2.2218 0.02735 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Testing exclusion of groups of variables

fm3r <- update(fm3, . ~ . - I(income^2) - I(income^3))

waldtest(fm3, fm3r, vcov = vcovHC(fm3, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + english + lunch + income + I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + english + lunch + income

#> Res.Df Df F Pr(>F)

#> 1 213

#> 2 215 -2 7.7448 0.0005664 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm4r_str1 <- update(fm4, . ~ . - stratio - I(stratio^2) - I(stratio^3))

waldtest(fm4, fm4r_str1, vcov = vcovHC(fm4, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

#> income + I(income^2) + I(income^3)

#> Model 2: score4 ~ english + lunch + income + I(income^2) + I(income^3)

#> Res.Df Df F Pr(>F)

#> 1 211

#> 2 214 -3 2.8565 0.03809 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm4r_str2 <- update(fm4, . ~ . - I(stratio^2) - I(stratio^3))

waldtest(fm4, fm4r_str2, vcov = vcovHC(fm4, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

#> income + I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + english + lunch + income + I(income^2) + I(income^3)

#> Res.Df Df F Pr(>F)

#> 1 211

#> 2 213 -2 0.4463 0.6406

fm4r_inc <- update(fm4, . ~ . - I(income^2) - I(income^3))

waldtest(fm4, fm4r_inc, vcov = vcovHC(fm4, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

#> income + I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

#> income

#> Res.Df Df F Pr(>F)

#> 1 211

#> 2 213 -2 7.7487 0.0005657 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r_str <- update(fm5, . ~ . - stratio - I(higheng * stratio))

waldtest(fm5, fm5r_str, vcov = vcovHC(fm5, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + higheng + I(higheng * stratio) + lunch + income +

#> I(income^2) + I(income^3)

#> Model 2: score4 ~ higheng + lunch + income + I(income^2) + I(income^3)

#> Res.Df Df F Pr(>F)

#> 1 212

#> 2 214 -2 4.0062 0.0196 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r_inc <- update(fm5, . ~ . - I(income^2) - I(income^3))

waldtest(fm5, fm5r_inc, vcov = vcovHC(fm5, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + higheng + I(higheng * stratio) + lunch + income +

#> I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + higheng + I(higheng * stratio) + lunch + income

#> Res.Df Df F Pr(>F)

#> 1 212

#> 2 214 -2 5.8468 0.003375 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r_high <- update(fm5, . ~ . - higheng - I(higheng * stratio))

waldtest(fm5, fm5r_high, vcov = vcovHC(fm5, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + higheng + I(higheng * stratio) + lunch + income +

#> I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + lunch + income + I(income^2) + I(income^3)

#> Res.Df Df F Pr(>F)

#> 1 212

#> 2 214 -2 1.5835 0.2077

fm6r_inc <- update(fm6, . ~ . - I(income^2) - I(income^3))

waldtest(fm6, fm6r_inc, vcov = vcovHC(fm6, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + lunch + income + I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + lunch + income

#> Res.Df Df F Pr(>F)

#> 1 214

#> 2 216 -2 6.5479 0.001737 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

##################################

## Home mortgage disclosure act ##

##################################

## data

data("HMDA", package = "AER")

## 11.1, 11.3, 11.7, 11.8 and 11.10, pp. 387--395

fm1 <- lm(I(as.numeric(deny) - 1) ~ pirat, data = HMDA)

fm2 <- lm(I(as.numeric(deny) - 1) ~ pirat + afam, data = HMDA)

fm3 <- glm(deny ~ pirat, family = binomial(link = "probit"), data = HMDA)

fm4 <- glm(deny ~ pirat + afam, family = binomial(link = "probit"), data = HMDA)

fm5 <- glm(deny ~ pirat + afam, family = binomial(link = "logit"), data = HMDA)

## Table 11.1, p. 401

mean(HMDA$pirat)

#> [1] 0.3308136

mean(HMDA$hirat)

#> [1] 0.2553461

mean(HMDA$lvrat)

#> [1] 0.7377759

mean(as.numeric(HMDA$chist))

#> [1] 2.116387

mean(as.numeric(HMDA$mhist))

#> [1] 1.721008

mean(as.numeric(HMDA$phist)-1)

#> [1] 0.07352941

prop.table(table(HMDA$insurance))

#>

#> no yes

#> 0.97983193 0.02016807

prop.table(table(HMDA$selfemp))

#>

#> no yes

#> 0.8836134 0.1163866

prop.table(table(HMDA$single))

#>

#> no yes

#> 0.6067227 0.3932773

prop.table(table(HMDA$hschool))

#>

#> no yes

#> 0.01638655 0.98361345

mean(HMDA$unemp)

#> [1] 3.774496

prop.table(table(HMDA$condomin))

#>

#> no yes

#> 0.7117647 0.2882353

prop.table(table(HMDA$afam))

#>

#> no yes

#> 0.857563 0.142437

prop.table(table(HMDA$deny))

#>

#> no yes

#> 0.8802521 0.1197479

## Table 11.2, pp. 403--404, numbers refer to columns

HMDA$lvrat <- factor(ifelse(HMDA$lvrat < 0.8, "low",

ifelse(HMDA$lvrat >= 0.8 & HMDA$lvrat <= 0.95, "medium", "high")),

levels = c("low", "medium", "high"))

HMDA$mhist <- as.numeric(HMDA$mhist)

HMDA$chist <- as.numeric(HMDA$chist)

fm1 <- lm(I(as.numeric(deny) - 1) ~ afam + pirat + hirat + lvrat + chist + mhist +

phist + insurance + selfemp, data = HMDA)

fm2 <- glm(deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist + insurance +

selfemp, family = binomial, data = HMDA)

fm3 <- glm(deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist + insurance +

selfemp, family = binomial(link = "probit"), data = HMDA)

fm4 <- glm(deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist + insurance +

selfemp + single + hschool + unemp, family = binomial(link = "probit"), data = HMDA)

fm5 <- glm(deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist + insurance +

selfemp + single + hschool + unemp + condomin +

I(mhist==3) + I(mhist==4) + I(chist==3) + I(chist==4) + I(chist==5) + I(chist==6),

family = binomial(link = "probit"), data = HMDA)

fm6 <- glm(deny ~ afam * (pirat + hirat) + lvrat + chist + mhist + phist + insurance +

selfemp + single + hschool + unemp, family = binomial(link = "probit"), data = HMDA)

coeftest(fm1, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.1829933 0.0276089 -6.6281 4.197e-11 ***

#> afamyes 0.0836967 0.0225101 3.7182 0.0002053 ***

#> pirat 0.4487963 0.1133333 3.9600 7.717e-05 ***

#> hirat -0.0480227 0.1093055 -0.4393 0.6604528

#> lvratmedium 0.0314498 0.0127097 2.4745 0.0134125 *

#> lvrathigh 0.1890511 0.0500520 3.7771 0.0001626 ***

#> chist 0.0307716 0.0045737 6.7279 2.150e-11 ***

#> mhist 0.0209104 0.0112637 1.8565 0.0635134 .

#> phistyes 0.1970876 0.0348005 5.6634 1.664e-08 ***

#> insuranceyes 0.7018841 0.0450008 15.5972 < 2.2e-16 ***

#> selfempyes 0.0598438 0.0204759 2.9227 0.0035035 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

fm4r <- update(fm4, . ~ . - single - hschool - unemp)

waldtest(fm4, fm4r, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp

#> Model 2: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp

#> Res.Df Df F Pr(>F)

#> 1 2366

#> 2 2369 -3 5.9463 0.0004893 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r <- update(fm5, . ~ . - single - hschool - unemp)

waldtest(fm5, fm5r, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp + condomin +

#> I(mhist == 3) + I(mhist == 4) + I(chist == 3) + I(chist ==

#> 4) + I(chist == 5) + I(chist == 6)

#> Model 2: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + condomin + I(mhist == 3) + I(mhist ==

#> 4) + I(chist == 3) + I(chist == 4) + I(chist == 5) + I(chist ==

#> 6)

#> Res.Df Df F Pr(>F)

#> 1 2359

#> 2 2362 -3 5.1601 0.001482 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm6r <- update(fm6, . ~ . - single - hschool - unemp)

waldtest(fm6, fm6r, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam * (pirat + hirat) + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp

#> Model 2: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + afam:pirat + afam:hirat

#> Res.Df Df F Pr(>F)

#> 1 2364

#> 2 2367 -3 5.8876 0.0005316 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r2 <- update(fm5, . ~ . - I(mhist==3) - I(mhist==4) - I(chist==3) - I(chist==4) -

I(chist==5) - I(chist==6))

waldtest(fm5, fm5r2, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp + condomin +

#> I(mhist == 3) + I(mhist == 4) + I(chist == 3) + I(chist ==

#> 4) + I(chist == 5) + I(chist == 6)

#> Model 2: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp + condomin

#> Res.Df Df F Pr(>F)

#> 1 2359

#> 2 2365 -6 1.2305 0.2873

fm6r2 <- update(fm6, . ~ . - afam * (pirat + hirat) + pirat + hirat)

waldtest(fm6, fm6r2, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam * (pirat + hirat) + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp

#> Model 2: deny ~ lvrat + chist + mhist + phist + insurance + selfemp +

#> single + hschool + unemp + pirat + hirat

#> Res.Df Df F Pr(>F)

#> 1 2364

#> 2 2367 -3 4.9217 0.00207 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm6r3 <- update(fm6, . ~ . - afam * (pirat + hirat) + pirat + hirat + afam)

waldtest(fm6, fm6r3, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam * (pirat + hirat) + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp

#> Model 2: deny ~ lvrat + chist + mhist + phist + insurance + selfemp +

#> single + hschool + unemp + pirat + hirat + afam

#> Res.Df Df F Pr(>F)

#> 1 2364

#> 2 2366 -2 0.2634 0.7685

#########################################################

## Shooting down the "More Guns Less Crime" hypothesis ##

#########################################################

## data

data("Guns", package = "AER")

## Empirical Exercise 10.1

fm1 <- lm(log(violent) ~ law, data = Guns)

fm2 <- lm(log(violent) ~ law + prisoners + density + income +

population + afam + cauc + male, data = Guns)

fm3 <- lm(log(violent) ~ law + prisoners + density + income +

population + afam + cauc + male + state, data = Guns)

fm4 <- lm(log(violent) ~ law + prisoners + density + income +

population + afam + cauc + male + state + year, data = Guns)

coeftest(fm1, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 6.134919 0.019287 318.078 < 2.2e-16 ***

#> lawyes -0.442965 0.047488 -9.328 < 2.2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm2, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 2.9817e+00 6.0668e-01 4.9149 1.016e-06 ***

#> lawyes -3.6839e-01 3.4654e-02 -10.6304 < 2.2e-16 ***

#> prisoners 1.6126e-03 1.8000e-04 8.9591 < 2.2e-16 ***

#> density 2.6688e-02 1.4294e-02 1.8671 0.062142 .

#> income 1.2051e-06 7.2498e-06 0.1662 0.868007

#> population 4.2710e-02 3.1345e-03 13.6255 < 2.2e-16 ***

#> afam 8.0853e-02 1.9916e-02 4.0598 5.241e-05 ***

#> cauc 3.1200e-02 9.6897e-03 3.2200 0.001317 **

#> male 8.8709e-03 1.2014e-02 0.7384 0.460435

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

printCoefmat(coeftest(fm3, vcov = sandwich)[1:9,])

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 4.0368e+00 3.7479e-01 10.7708 < 2.2e-16 ***

#> lawyes -4.6141e-02 1.9435e-02 -2.3741 0.01776 *

#> prisoners -7.1008e-05 9.4831e-05 -0.7488 0.45414

#> density -1.7229e-01 1.0221e-01 -1.6857 0.09213 .

#> income -9.2037e-06 6.5619e-06 -1.4026 0.16102

#> population 1.1525e-02 9.4572e-03 1.2186 0.22325

#> afam 1.0428e-01 1.6133e-02 6.4636 1.526e-10 ***

#> cauc 4.0861e-02 5.2487e-03 7.7850 1.585e-14 ***

#> male -5.0273e-02 7.5923e-03 -6.6215 5.518e-11 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

printCoefmat(coeftest(fm4, vcov = sandwich)[1:9,])

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.9720e+00 4.3322e-01 9.1685 < 2.2e-16 ***

#> lawyes -2.7994e-02 1.8692e-02 -1.4976 0.1345

#> prisoners 7.5994e-05 8.0008e-05 0.9498 0.3424

#> density -9.1555e-02 6.2588e-02 -1.4628 0.1438

#> income 9.5859e-07 6.9440e-06 0.1380 0.8902

#> population -4.7545e-03 6.4673e-03 -0.7351 0.4624

#> afam 2.9186e-02 2.0298e-02 1.4379 0.1507

#> cauc 9.2500e-03 8.2188e-03 1.1255 0.2606

#> male 7.3326e-02 1.8116e-02 4.0475 5.542e-05 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

###########################

## US traffic fatalities ##

###########################

## data from Stock and Watson (2007)

data("Fatalities", package = "AER")

Fatalities <- transform(Fatalities,

## fatality rate (number of traffic deaths per 10,000 people living in that state in that year)

frate = fatal/pop * 10000,

## add discretized version of minimum legal drinking age

drinkagec = relevel(cut(drinkage, breaks = 18:22, include.lowest = TRUE, right = FALSE), ref = 4),

## any punishment?

punish = factor(jail == "yes" | service == "yes", labels = c("no", "yes"))

)

## plm package

library("plm")

## for comparability with Stata we use HC1 below

## p. 351, Eq. (10.2)

f1982 <- subset(Fatalities, year == "1982")

fm_1982 <- lm(frate ~ beertax, data = f1982)

coeftest(fm_1982, vcov = vcovHC(fm_1982, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 2.01038 0.14957 13.4408 <2e-16 ***

#> beertax 0.14846 0.13261 1.1196 0.2687

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## p. 353, Eq. (10.3)

f1988 <- subset(Fatalities, year == "1988")

fm_1988 <- lm(frate ~ beertax, data = f1988)

coeftest(fm_1988, vcov = vcovHC(fm_1988, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1.85907 0.11461 16.2205 < 2.2e-16 ***

#> beertax 0.43875 0.12786 3.4314 0.001279 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## pp. 355, Eq. (10.8)

fm_diff <- lm(I(f1988$frate - f1982$frate) ~ I(f1988$beertax - f1982$beertax))

coeftest(fm_diff, vcov = vcovHC(fm_diff, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.072037 0.065355 -1.1022 0.276091

#> I(f1988$beertax - f1982$beertax) -1.040973 0.355006 -2.9323 0.005229 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## pp. 360, Eq. (10.15)

## (1) via formula

fm_sfe <- lm(frate ~ beertax + state - 1, data = Fatalities)

## (2) by hand

fat <- with(Fatalities,

data.frame(frates = frate - ave(frate, state),

beertaxs = beertax - ave(beertax, state)))

fm_sfe2 <- lm(frates ~ beertaxs - 1, data = fat)

## (3) via plm()

fm_sfe3 <- plm(frate ~ beertax, data = Fatalities,

index = c("state", "year"), model = "within")

coeftest(fm_sfe, vcov = vcovHC(fm_sfe, type = "HC1"))[1,]

#> Estimate Std. Error t value Pr(>|t|)

#> -0.655873722 0.203279719 -3.226459220 0.001398372

## uses different df in sd and p-value

coeftest(fm_sfe2, vcov = vcovHC(fm_sfe2, type = "HC1"))[1,]

#> Estimate Std. Error t value Pr(>|t|)

#> -0.655873722 0.188153627 -3.485841496 0.000555894

## uses different df in p-value

coeftest(fm_sfe3, vcov = vcovHC(fm_sfe3, type = "HC1", method = "white1"))[1,]

#> Estimate Std. Error t value Pr(>|t|)

#> -0.6558737222 0.1881536274 -3.4858414958 0.0005673213

## pp. 363, Eq. (10.21)

## via lm()

fm_stfe <- lm(frate ~ beertax + state + year - 1, data = Fatalities)

coeftest(fm_stfe, vcov = vcovHC(fm_stfe, type = "HC1"))[1,]

#> Estimate Std. Error t value Pr(>|t|)

#> -0.6399800 0.2547149 -2.5125346 0.0125470

## via plm()

fm_stfe2 <- plm(frate ~ beertax, data = Fatalities,

index = c("state", "year"), model = "within", effect = "twoways")

coeftest(fm_stfe2, vcov = vcovHC) ## different

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> beertax -0.63998 0.34963 -1.8305 0.06824 .

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## p. 368, Table 10.1, numbers refer to cols.

fm1 <- plm(frate ~ beertax, data = Fatalities, index = c("state", "year"),

model = "pooling")

fm2 <- plm(frate ~ beertax, data = Fatalities, index = c("state", "year"),

model = "within")

fm3 <- plm(frate ~ beertax, data = Fatalities, index = c("state", "year"),

model = "within", effect = "twoways")

fm4 <- plm(frate ~ beertax + drinkagec + jail + service + miles + unemp + log(income),

data = Fatalities, index = c("state", "year"), model = "within", effect = "twoways")

fm5 <- plm(frate ~ beertax + drinkagec + jail + service + miles,

data = Fatalities, index = c("state", "year"), model = "within", effect = "twoways")

fm6 <- plm(frate ~ beertax + drinkage + punish + miles + unemp + log(income),

data = Fatalities, index = c("state", "year"), model = "within", effect = "twoways")

fm7 <- plm(frate ~ beertax + drinkagec + jail + service + miles + unemp + log(income),

data = Fatalities, index = c("state", "year"), model = "within", effect = "twoways")

## summaries not too close, s.e.s generally too small

coeftest(fm1, vcov = vcovHC)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1.85331 0.11710 15.8263 < 2.2e-16 ***

#> beertax 0.36461 0.11826 3.0832 0.002218 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm2, vcov = vcovHC)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> beertax -0.65587 0.28837 -2.2744 0.02368 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm3, vcov = vcovHC)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> beertax -0.63998 0.34963 -1.8305 0.06824 .

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm4, vcov = vcovHC)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> beertax -4.4895e-01 2.8850e-01 -1.5562 0.120828

#> drinkagec[18,19) 2.8149e-02 6.8014e-02 0.4139 0.679299

#> drinkagec[19,20) -1.8550e-02 4.8162e-02 -0.3852 0.700416

#> drinkagec[20,21) 3.1375e-02 4.8744e-02 0.6437 0.520323

#> jailyes 1.3058e-02 1.6115e-02 0.8103 0.418458

#> serviceyes 3.3446e-02 1.2873e-01 0.2598 0.795197

#> miles 8.2275e-06 6.6313e-06 1.2407 0.215785

#> unemp -6.3111e-02 1.2615e-02 -5.0028 1.015e-06 ***

#> log(income) 1.8146e+00 6.1659e-01 2.9429 0.003532 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm5, vcov = vcovHC)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> beertax -7.0442e-01 3.3804e-01 -2.0838 0.03810 *

#> drinkagec[18,19) -1.1360e-02 8.0764e-02 -0.1407 0.88825

#> drinkagec[19,20) -7.8033e-02 6.5591e-02 -1.1897 0.23520

#> drinkagec[20,21) -1.0224e-01 5.4695e-02 -1.8692 0.06266 .

#> jailyes -2.5965e-02 1.8624e-02 -1.3942 0.16439

#> serviceyes 1.4690e-01 1.3970e-01 1.0515 0.29395

#> miles 1.7372e-05 1.0221e-05 1.6996 0.09033 .

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm6, vcov = vcovHC)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> beertax -4.5647e-01 2.9809e-01 -1.5313 0.126845

#> drinkage -2.1567e-03 2.0908e-02 -0.1032 0.917916

#> punishyes 3.8981e-02 1.0023e-01 0.3889 0.697636

#> miles 8.9787e-06 6.8958e-06 1.3020 0.193991

#> unemp -6.2694e-02 1.2854e-02 -4.8776 1.82e-06 ***

#> log(income) 1.7864e+00 6.2511e-01 2.8578 0.004592 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm7, vcov = vcovHC)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> beertax -4.4895e-01 2.8850e-01 -1.5562 0.120828

#> drinkagec[18,19) 2.8149e-02 6.8014e-02 0.4139 0.679299

#> drinkagec[19,20) -1.8550e-02 4.8162e-02 -0.3852 0.700416

#> drinkagec[20,21) 3.1375e-02 4.8744e-02 0.6437 0.520323

#> jailyes 1.3058e-02 1.6115e-02 0.8103 0.418458

#> serviceyes 3.3446e-02 1.2873e-01 0.2598 0.795197

#> miles 8.2275e-06 6.6313e-06 1.2407 0.215785

#> unemp -6.3111e-02 1.2615e-02 -5.0028 1.015e-06 ***

#> log(income) 1.8146e+00 6.1659e-01 2.9429 0.003532 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

######################################

## Cigarette consumption panel data ##

######################################

## data and transformations

data("CigarettesSW", package = "AER")

CigarettesSW <- transform(CigarettesSW,

rprice = price/cpi,

rincome = income/population/cpi,

rtax = tax/cpi,

rtdiff = (taxs - tax)/cpi

)

c1985 <- subset(CigarettesSW, year == "1985")

c1995 <- subset(CigarettesSW, year == "1995")

## convenience function: HC1 covariances

hc1 <- function(x) vcovHC(x, type = "HC1")

## Equations 12.9--12.11

fm_s1 <- lm(log(rprice) ~ rtdiff, data = c1995)

coeftest(fm_s1, vcov = hc1)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 4.6165463 0.0289177 159.6444 < 2.2e-16 ***

#> rtdiff 0.0307289 0.0048354 6.3549 8.489e-08 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

fm_s2 <- lm(log(packs) ~ fitted(fm_s1), data = c1995)

fm_ivreg <- ivreg(log(packs) ~ log(rprice) | rtdiff, data = c1995)

coeftest(fm_ivreg, vcov = hc1)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 9.71988 1.52832 6.3598 8.346e-08 ***

#> log(rprice) -1.08359 0.31892 -3.3977 0.001411 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Equation 12.15

fm_ivreg2 <- ivreg(log(packs) ~ log(rprice) + log(rincome) | log(rincome) + rtdiff, data = c1995)

coeftest(fm_ivreg2, vcov = hc1)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 9.43066 1.25939 7.4883 1.935e-09 ***

#> log(rprice) -1.14338 0.37230 -3.0711 0.003611 **

#> log(rincome) 0.21452 0.31175 0.6881 0.494917

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Equation 12.16

fm_ivreg3 <- ivreg(log(packs) ~ log(rprice) + log(rincome) | log(rincome) + rtdiff + rtax,

data = c1995)

coeftest(fm_ivreg3, vcov = hc1)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 9.89496 0.95922 10.3157 1.947e-13 ***

#> log(rprice) -1.27742 0.24961 -5.1177 6.211e-06 ***

#> log(rincome) 0.28040 0.25389 1.1044 0.2753

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Table 12.1, p. 448

ydiff <- log(c1995$packs) - log(c1985$packs)

pricediff <- log(c1995$price/c1995$cpi) - log(c1985$price/c1985$cpi)

incdiff <- log(c1995$income/c1995$population/c1995$cpi) -

log(c1985$income/c1985$population/c1985$cpi)

taxsdiff <- (c1995$taxs - c1995$tax)/c1995$cpi - (c1985$taxs - c1985$tax)/c1985$cpi

taxdiff <- c1995$tax/c1995$cpi - c1985$tax/c1985$cpi

fm_diff1 <- ivreg(ydiff ~ pricediff + incdiff | incdiff + taxsdiff)

fm_diff2 <- ivreg(ydiff ~ pricediff + incdiff | incdiff + taxdiff)

fm_diff3 <- ivreg(ydiff ~ pricediff + incdiff | incdiff + taxsdiff + taxdiff)

coeftest(fm_diff1, vcov = hc1)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.117962 0.068217 -1.7292 0.09062 .

#> pricediff -0.938014 0.207502 -4.5205 4.454e-05 ***

#> incdiff 0.525970 0.339494 1.5493 0.12832

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm_diff2, vcov = hc1)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.017049 0.067217 -0.2536 0.8009

#> pricediff -1.342515 0.228661 -5.8712 4.848e-07 ***

#> incdiff 0.428146 0.298718 1.4333 0.1587

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm_diff3, vcov = hc1)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.052003 0.062488 -0.8322 0.4097

#> pricediff -1.202403 0.196943 -6.1053 2.178e-07 ***

#> incdiff 0.462030 0.309341 1.4936 0.1423

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## checking instrument relevance

fm_rel1 <- lm(pricediff ~ taxsdiff + incdiff)

fm_rel2 <- lm(pricediff ~ taxdiff + incdiff)

fm_rel3 <- lm(pricediff ~ incdiff + taxsdiff + taxdiff)

linearHypothesis(fm_rel1, "taxsdiff = 0", vcov = hc1)

#>

#> Linear hypothesis test:

#> taxsdiff = 0

#>

#> Model 1: restricted model

#> Model 2: pricediff ~ taxsdiff + incdiff

#>

#> Note: Coefficient covariance matrix supplied.

#>

#> Res.Df Df F Pr(>F)

#> 1 46

#> 2 45 1 33.674 6.119e-07 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

linearHypothesis(fm_rel2, "taxdiff = 0", vcov = hc1)

#>

#> Linear hypothesis test:

#> taxdiff = 0

#>

#> Model 1: restricted model

#> Model 2: pricediff ~ taxdiff + incdiff

#>

#> Note: Coefficient covariance matrix supplied.

#>

#> Res.Df Df F Pr(>F)

#> 1 46

#> 2 45 1 107.18 1.735e-13 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

linearHypothesis(fm_rel3, c("taxsdiff = 0", "taxdiff = 0"), vcov = hc1)

#>

#> Linear hypothesis test:

#> taxsdiff = 0

#> taxdiff = 0

#>

#> Model 1: restricted model

#> Model 2: pricediff ~ incdiff + taxsdiff + taxdiff

#>

#> Note: Coefficient covariance matrix supplied.

#>

#> Res.Df Df F Pr(>F)

#> 1 46

#> 2 44 2 88.616 3.709e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

## testing overidentifying restrictions (J test)

fm_or <- lm(residuals(fm_diff3) ~ incdiff + taxsdiff + taxdiff)

(fm_or_test <- linearHypothesis(fm_or, c("taxsdiff = 0", "taxdiff = 0"), test = "Chisq"))

#>

#> Linear hypothesis test:

#> taxsdiff = 0

#> taxdiff = 0

#>

#> Model 1: restricted model

#> Model 2: residuals(fm_diff3) ~ incdiff + taxsdiff + taxdiff

#>

#> Res.Df RSS Df Sum of Sq Chisq Pr(>Chisq)

#> 1 46 0.37472

#> 2 44 0.33695 2 0.037769 4.932 0.08492 .

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

## warning: df (and hence p-value) invalid above.

## correct df: # instruments - # endogenous variables

pchisq(fm_or_test[2,5], df.residual(fm_diff3) - df.residual(fm_or), lower.tail = FALSE)

#> [1] 0.02636406

#####################################################

## Project STAR: Student-teacher achievement ratio ##

#####################################################

## data

data("STAR", package = "AER")

## p. 488

fmk <- lm(I(readk + mathk) ~ stark, data = STAR)

fm1 <- lm(I(read1 + math1) ~ star1, data = STAR)

fm2 <- lm(I(read2 + math2) ~ star2, data = STAR)

fm3 <- lm(I(read3 + math3) ~ star3, data = STAR)

coeftest(fm3, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1228.50636 1.67959 731.4322 < 2.2e-16 ***

#> star3small 15.58660 2.39544 6.5068 8.303e-11 ***

#> star3regular+aide -0.29094 2.27214 -0.1280 0.8981

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## p. 489

fmke <- lm(I(readk + mathk) ~ stark + experiencek, data = STAR)

coeftest(fmke, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 904.72124 2.22157 407.2433 < 2.2e-16 ***

#> starksmall 14.00613 2.44620 5.7257 1.082e-08 ***

#> starkregular+aide -0.60058 2.25352 -0.2665 0.7899

#> experiencek 1.46903 0.16923 8.6808 < 2.2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## equivalently:

## - reshape data from wide into long format

## - fit a single model nested in grade

## (a) variables and their levels

nam <- c("star", "read", "math", "lunch", "school", "degree", "ladder",

"experience", "tethnicity", "system", "schoolid")

lev <- c("k", "1", "2", "3")

## (b) reshaping

star <- reshape(STAR, idvar = "id", ids = row.names(STAR),

times = lev, timevar = "grade", direction = "long",

varying = lapply(nam, function(x) paste(x, lev, sep = "")))

## (c) improve variable names and type

names(star)[5:15] <- nam

star$id <- factor(star$id)

star$grade <- factor(star$grade, levels = lev,

labels = c("kindergarten", "1st", "2nd", "3rd"))

rm(nam, lev)

## (d) model fitting

fm <- lm(I(read + math) ~ 0 + grade/star, data = star)

#################################################

## Quarterly US macroeconomic data (1957-2005) ##

#################################################

## data

data("USMacroSW", package = "AER")

library("dynlm")

usm <- ts.intersect(USMacroSW, 4 * 100 * diff(log(USMacroSW[, "cpi"])))

colnames(usm) <- c(colnames(USMacroSW), "infl")

## Equation 14.7, p. 536

fm_ar1 <- dynlm(d(infl) ~ L(d(infl)),

data = usm, start = c(1962,1), end = c(2004,4))

coeftest(fm_ar1, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.017101 0.126145 0.1356 0.89233

#> L(d(infl)) -0.238047 0.095939 -2.4812 0.01407 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Equation 14.13, p. 538

fm_ar4 <- dynlm(d(infl) ~ L(d(infl), 1:4),

data = usm, start = c(1962,1), end = c(2004,4))

coeftest(fm_ar4, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.022429 0.115912 0.1935 0.846799

#> L(d(infl), 1:4)1 -0.257943 0.091238 -2.8272 0.005271 **

#> L(d(infl), 1:4)2 -0.322031 0.079367 -4.0575 7.602e-05 ***

#> L(d(infl), 1:4)3 0.157609 0.082870 1.9019 0.058909 .

#> L(d(infl), 1:4)4 -0.030251 0.091685 -0.3299 0.741853

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Equation 14.16, p. 542

fm_adl41 <- dynlm(d(infl) ~ L(d(infl), 1:4) + L(unemp),

data = usm, start = c(1962,1), end = c(2004,4))

coeftest(fm_adl41, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1.279561 0.526634 2.4297 0.0161775 *

#> L(d(infl), 1:4)1 -0.305587 0.086918 -3.5158 0.0005653 ***

#> L(d(infl), 1:4)2 -0.390967 0.089016 -4.3921 1.994e-05 ***

#> L(d(infl), 1:4)3 0.086472 0.084000 1.0294 0.3047748

#> L(d(infl), 1:4)4 -0.081073 0.088541 -0.9156 0.3611790

#> L(unemp) -0.212146 0.095227 -2.2278 0.0272387 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Equation 14.17, p. 542

fm_adl44 <- dynlm(d(infl) ~ L(d(infl), 1:4) + L(unemp, 1:4),

data = usm, start = c(1962,1), end = c(2004,4))

coeftest(fm_adl44, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1.304286 0.439631 2.9668 0.0034624 **

#> L(d(infl), 1:4)1 -0.419822 0.086345 -4.8622 2.714e-06 ***

#> L(d(infl), 1:4)2 -0.366630 0.091544 -4.0049 9.407e-05 ***

#> L(d(infl), 1:4)3 0.056568 0.082549 0.6853 0.4941479

#> L(d(infl), 1:4)4 -0.036458 0.081314 -0.4484 0.6544868

#> L(unemp, 1:4)1 -2.635568 0.462228 -5.7019 5.435e-08 ***

#> L(unemp, 1:4)2 3.043088 0.856420 3.5533 0.0004979 ***

#> L(unemp, 1:4)3 -0.377371 0.887477 -0.4252 0.6712384

#> L(unemp, 1:4)4 -0.248424 0.448296 -0.5542 0.5802345

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Granger causality test mentioned on p. 547

waldtest(fm_ar4, fm_adl44, vcov = sandwich)

#> Wald test

#>

#> Model 1: d(infl) ~ L(d(infl), 1:4)

#> Model 2: d(infl) ~ L(d(infl), 1:4) + L(unemp, 1:4)

#> Res.Df Df F Pr(>F)

#> 1 167

#> 2 163 4 8.9095 1.567e-06 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

## Equation 14.28, p. 559

fm_sp1 <- dynlm(infl ~ log(gdpjp), start = c(1965,1), end = c(1981,4), data = usm)

coeftest(fm_sp1, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -37.78017 3.98722 -9.4753 6.274e-14 ***

#> log(gdpjp) 3.83150 0.35905 10.6713 5.212e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Equation 14.29, p. 559

fm_sp2 <- dynlm(infl ~ log(gdpjp), start = c(1982,1), end = c(2004,4), data = usm)

coeftest(fm_sp2, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 31.20293 10.41216 2.9968 0.003526 **

#> log(gdpjp) -2.16712 0.79841 -2.7143 0.007960 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Equation 14.34, p. 563: ADF by hand

fm_adf <- dynlm(d(infl) ~ L(infl) + L(d(infl), 1:4),

data = usm, start = c(1962,1), end = c(2004,4))

coeftest(fm_adf)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.5068158 0.2141807 2.3663 0.019120 *

#> L(infl) -0.1134169 0.0422344 -2.6854 0.007980 **

#> L(d(infl), 1:4)1 -0.1864426 0.0805144 -2.3156 0.021801 *

#> L(d(infl), 1:4)2 -0.2563879 0.0814630 -3.1473 0.001954 **

#> L(d(infl), 1:4)3 0.1990491 0.0793514 2.5085 0.013086 *

#> L(d(infl), 1:4)4 0.0099994 0.0779921 0.1282 0.898137

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

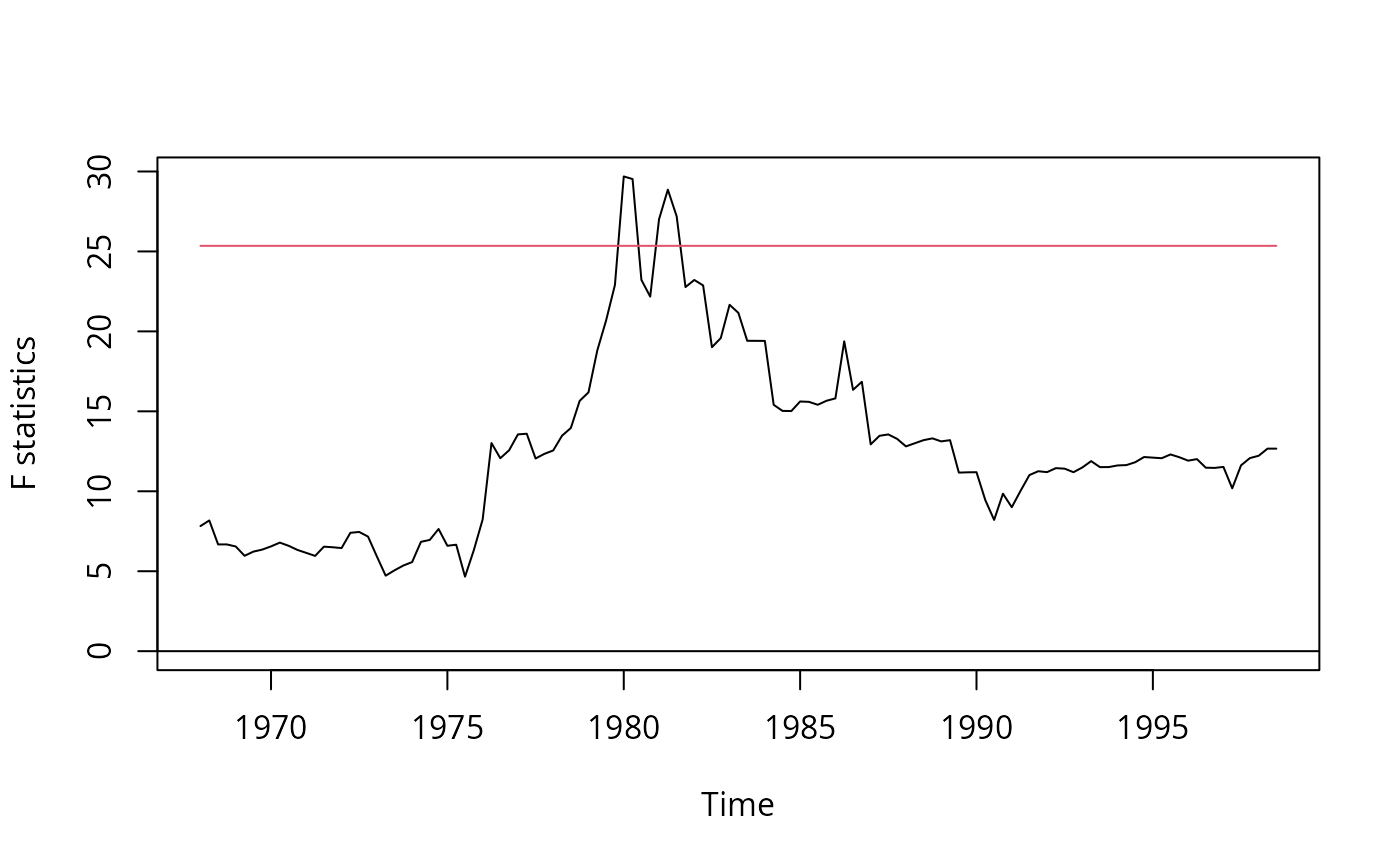

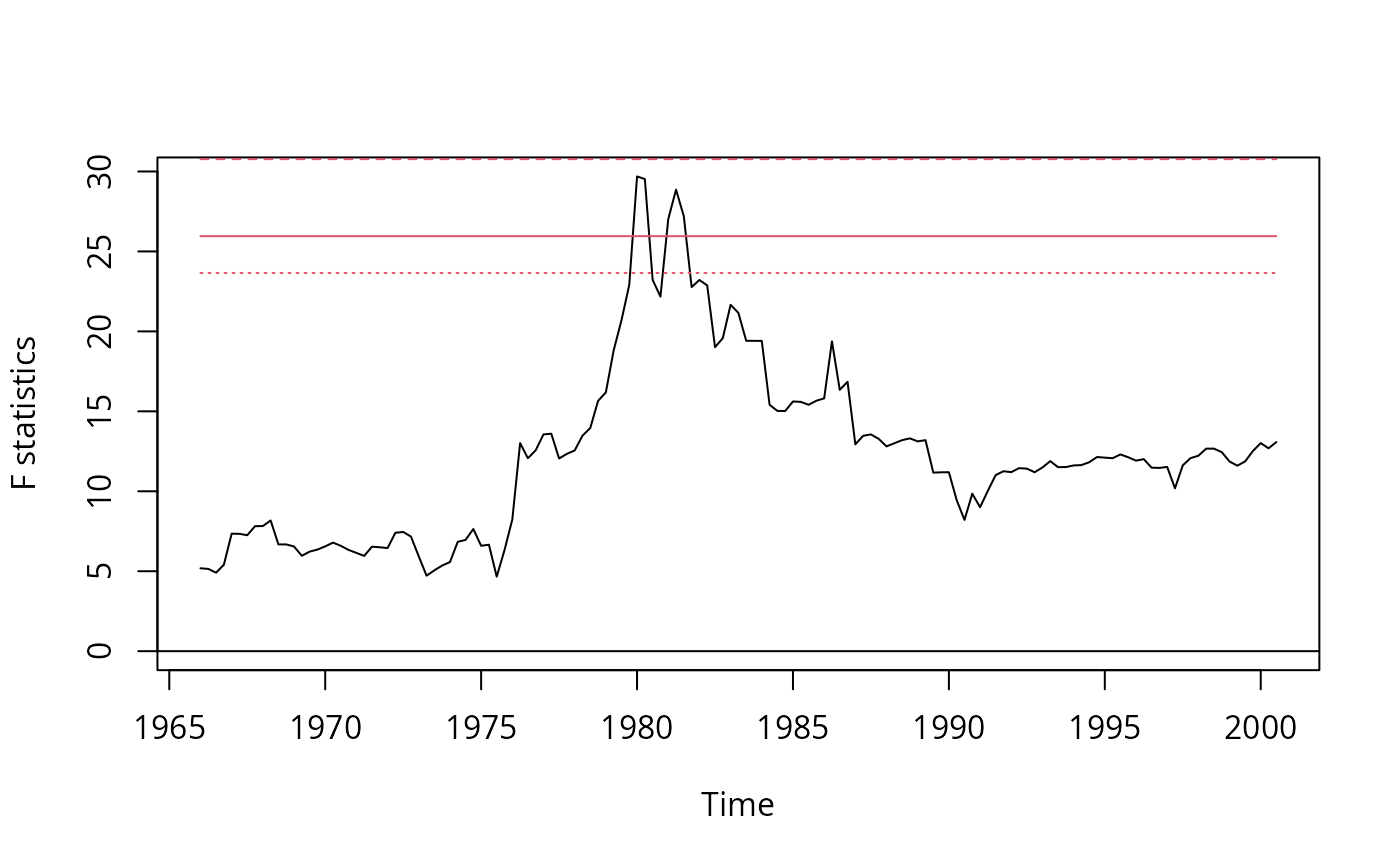

## Figure 14.5, p. 570

## SW perform partial break test of unemp coefs

## here full model is used

library("strucchange")

infl <- usm[, "infl"]

unemp <- usm[, "unemp"]

usm <- ts.intersect(diff(infl), lag(diff(infl), k = -1), lag(diff(infl), k = -2),

lag(diff(infl), k = -3), lag(diff(infl), k = -4), lag(unemp, k = -1),

lag(unemp, k = -2), lag(unemp, k = -3), lag(unemp, k = -4))

colnames(usm) <- c("dinfl", paste("dinfl", 1:4, sep = ""), paste("unemp", 1:4, sep = ""))

usm <- window(usm, start = c(1962, 1), end = c(2004, 4))

fs <- Fstats(dinfl ~ ., data = usm)

sctest(fs, type = "supF")

#>

#> supF test

#>

#> data: fs

#> sup.F = 29.691, p-value = 0.01193

#>

plot(fs)

## Table 8.2, use HC1 for comparability with Stata

fm1 <- lm(subs ~ citeprice, data = log(journals))

fm2 <- lm(subs ~ citeprice + age + chars, data = log(journals))

fm3 <- lm(subs ~ citeprice + I(citeprice^2) + I(citeprice^3) +

age + I(age * citeprice) + chars, data = log(journals))

fm4 <- lm(subs ~ citeprice + age + I(age * citeprice) + chars, data = log(journals))

coeftest(fm1, vcov = vcovHC(fm1, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 4.766212 0.055258 86.253 < 2.2e-16 ***

#> citeprice -0.533053 0.033959 -15.697 < 2.2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm2, vcov = vcovHC(fm2, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.206648 0.379725 8.4447 1.102e-14 ***

#> citeprice -0.407718 0.043717 -9.3262 < 2.2e-16 ***

#> age 0.423649 0.119064 3.5581 0.0004801 ***

#> chars 0.205614 0.097751 2.1035 0.0368474 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm3, vcov = vcovHC(fm3, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.4075956 0.3735992 9.1210 < 2.2e-16 ***

#> citeprice -0.9609365 0.1601349 -6.0008 1.121e-08 ***

#> I(citeprice^2) 0.0165099 0.0254886 0.6477 0.518015

#> I(citeprice^3) 0.0036666 0.0055147 0.6649 0.507008

#> age 0.3730539 0.1176966 3.1696 0.001805 **

#> I(age * citeprice) 0.1557773 0.0518947 3.0018 0.003081 **

#> chars 0.2346178 0.0977318 2.4006 0.017428 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm4, vcov = vcovHC(fm4, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.433521 0.367471 9.3436 < 2.2e-16 ***

#> citeprice -0.898910 0.144648 -6.2144 3.656e-09 ***

#> age 0.373515 0.117527 3.1781 0.0017529 **

#> I(age * citeprice) 0.140959 0.040199 3.5065 0.0005769 ***

#> chars 0.229466 0.096493 2.3781 0.0184822 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

waldtest(fm3, fm4, vcov = vcovHC(fm3, type = "HC1"))

#> Wald test

#>

#> Model 1: subs ~ citeprice + I(citeprice^2) + I(citeprice^3) + age + I(age *

#> citeprice) + chars

#> Model 2: subs ~ citeprice + age + I(age * citeprice) + chars

#> Res.Df Df F Pr(>F)

#> 1 173

#> 2 175 -2 0.249 0.7799

###############################

## Massachusetts test scores ##

###############################

## compare Massachusetts with California

data("MASchools", package = "AER")

data("CASchools", package = "AER")

CASchools <- transform(CASchools,

stratio = students/teachers,

score4 = (math + read)/2

)

## parts of Table 9.1, p. 330

vars <- c("score4", "stratio", "english", "lunch", "income")

cbind(

CA_mean = sapply(CASchools[, vars], mean),

CA_sd = sapply(CASchools[, vars], sd),

MA_mean = sapply(MASchools[, vars], mean),

MA_sd = sapply(MASchools[, vars], sd))

#> CA_mean CA_sd MA_mean MA_sd

#> score4 654.15655 19.053347 709.827273 15.126474

#> stratio 19.64043 1.891812 17.344091 2.276666

#> english 15.76816 18.285927 1.117676 2.900940

#> lunch 44.70524 27.123381 15.315909 15.060068

#> income 15.31659 7.225890 18.746764 5.807637

## Table 9.2, pp. 332--333, numbers refer to columns

MASchools <- transform(MASchools, higheng = english > median(english))

fm1 <- lm(score4 ~ stratio, data = MASchools)

fm2 <- lm(score4 ~ stratio + english + lunch + log(income), data = MASchools)

fm3 <- lm(score4 ~ stratio + english + lunch + income + I(income^2) + I(income^3),

data = MASchools)

fm4 <- lm(score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

income + I(income^2) + I(income^3), data = MASchools)

fm5 <- lm(score4 ~ stratio + higheng + I(higheng * stratio) + lunch +

income + I(income^2) + I(income^3), data = MASchools)

fm6 <- lm(score4 ~ stratio + lunch + income + I(income^2) + I(income^3),

data = MASchools)

## for comparability with Stata use HC1 below

coeftest(fm1, vcov = vcovHC(fm1, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 739.62113 8.60727 85.9298 < 2.2e-16 ***

#> stratio -1.71781 0.49906 -3.4421 0.000692 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm2, vcov = vcovHC(fm2, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 682.431602 11.497244 59.3561 < 2.2e-16 ***

#> stratio -0.689179 0.269973 -2.5528 0.01138 *

#> english -0.410745 0.306377 -1.3407 0.18145

#> lunch -0.521465 0.077659 -6.7148 1.653e-10 ***

#> log(income) 16.529359 3.145722 5.2546 3.566e-07 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm3, vcov = vcovHC(fm3, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 7.4403e+02 2.1318e+01 34.9016 < 2.2e-16 ***

#> stratio -6.4091e-01 2.6848e-01 -2.3872 0.01785 *

#> english -4.3712e-01 3.0332e-01 -1.4411 0.15103

#> lunch -5.8182e-01 9.7353e-02 -5.9764 9.488e-09 ***

#> income -3.0667e+00 2.3525e+00 -1.3036 0.19379

#> I(income^2) 1.6369e-01 8.5330e-02 1.9183 0.05641 .

#> I(income^3) -2.1793e-03 9.7033e-04 -2.2459 0.02574 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm4, vcov = vcovHC(fm4, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 665.4960529 81.3317629 8.1825 2.600e-14 ***

#> stratio 12.4259758 14.0101690 0.8869 0.37613

#> I(stratio^2) -0.6803029 0.7365191 -0.9237 0.35671

#> I(stratio^3) 0.0114737 0.0126663 0.9058 0.36605

#> english -0.4341659 0.2997883 -1.4482 0.14903

#> lunch -0.5872165 0.1040207 -5.6452 5.283e-08 ***

#> income -3.3815370 2.4906830 -1.3577 0.17602

#> I(income^2) 0.1741018 0.0892596 1.9505 0.05244 .

#> I(income^3) -0.0022883 0.0010078 -2.2706 0.02418 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm5, vcov = vcovHC(fm5, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 759.9142249 23.2331213 32.7082 < 2.2e-16 ***

#> stratio -1.0176806 0.3703923 -2.7476 0.006521 **

#> highengTRUE -12.5607339 9.7934588 -1.2826 0.201046

#> I(higheng * stratio) 0.7986123 0.5552225 1.4384 0.151805

#> lunch -0.7085098 0.0908442 -7.7992 2.785e-13 ***

#> income -3.8665072 2.4884002 -1.5538 0.121721

#> I(income^2) 0.1841250 0.0898247 2.0498 0.041612 *

#> I(income^3) -0.0023364 0.0010153 -2.3013 0.022349 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm6, vcov = vcovHC(fm6, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 7.4736e+02 2.0278e+01 36.8563 < 2e-16 ***

#> stratio -6.7188e-01 2.7128e-01 -2.4767 0.01404 *

#> lunch -6.5308e-01 7.2980e-02 -8.9487 < 2e-16 ***

#> income -3.2180e+00 2.3057e+00 -1.3956 0.16427

#> I(income^2) 1.6479e-01 8.4634e-02 1.9471 0.05284 .

#> I(income^3) -2.1550e-03 9.6995e-04 -2.2218 0.02735 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## Testing exclusion of groups of variables

fm3r <- update(fm3, . ~ . - I(income^2) - I(income^3))

waldtest(fm3, fm3r, vcov = vcovHC(fm3, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + english + lunch + income + I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + english + lunch + income

#> Res.Df Df F Pr(>F)

#> 1 213

#> 2 215 -2 7.7448 0.0005664 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm4r_str1 <- update(fm4, . ~ . - stratio - I(stratio^2) - I(stratio^3))

waldtest(fm4, fm4r_str1, vcov = vcovHC(fm4, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

#> income + I(income^2) + I(income^3)

#> Model 2: score4 ~ english + lunch + income + I(income^2) + I(income^3)

#> Res.Df Df F Pr(>F)

#> 1 211

#> 2 214 -3 2.8565 0.03809 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm4r_str2 <- update(fm4, . ~ . - I(stratio^2) - I(stratio^3))

waldtest(fm4, fm4r_str2, vcov = vcovHC(fm4, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

#> income + I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + english + lunch + income + I(income^2) + I(income^3)

#> Res.Df Df F Pr(>F)

#> 1 211

#> 2 213 -2 0.4463 0.6406

fm4r_inc <- update(fm4, . ~ . - I(income^2) - I(income^3))

waldtest(fm4, fm4r_inc, vcov = vcovHC(fm4, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

#> income + I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + I(stratio^2) + I(stratio^3) + english + lunch +

#> income

#> Res.Df Df F Pr(>F)

#> 1 211

#> 2 213 -2 7.7487 0.0005657 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r_str <- update(fm5, . ~ . - stratio - I(higheng * stratio))

waldtest(fm5, fm5r_str, vcov = vcovHC(fm5, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + higheng + I(higheng * stratio) + lunch + income +

#> I(income^2) + I(income^3)

#> Model 2: score4 ~ higheng + lunch + income + I(income^2) + I(income^3)

#> Res.Df Df F Pr(>F)

#> 1 212

#> 2 214 -2 4.0062 0.0196 *

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r_inc <- update(fm5, . ~ . - I(income^2) - I(income^3))

waldtest(fm5, fm5r_inc, vcov = vcovHC(fm5, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + higheng + I(higheng * stratio) + lunch + income +

#> I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + higheng + I(higheng * stratio) + lunch + income

#> Res.Df Df F Pr(>F)

#> 1 212

#> 2 214 -2 5.8468 0.003375 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r_high <- update(fm5, . ~ . - higheng - I(higheng * stratio))

waldtest(fm5, fm5r_high, vcov = vcovHC(fm5, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + higheng + I(higheng * stratio) + lunch + income +

#> I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + lunch + income + I(income^2) + I(income^3)

#> Res.Df Df F Pr(>F)

#> 1 212

#> 2 214 -2 1.5835 0.2077

fm6r_inc <- update(fm6, . ~ . - I(income^2) - I(income^3))

waldtest(fm6, fm6r_inc, vcov = vcovHC(fm6, type = "HC1"))

#> Wald test

#>

#> Model 1: score4 ~ stratio + lunch + income + I(income^2) + I(income^3)

#> Model 2: score4 ~ stratio + lunch + income

#> Res.Df Df F Pr(>F)

#> 1 214

#> 2 216 -2 6.5479 0.001737 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

##################################

## Home mortgage disclosure act ##

##################################

## data

data("HMDA", package = "AER")

## 11.1, 11.3, 11.7, 11.8 and 11.10, pp. 387--395

fm1 <- lm(I(as.numeric(deny) - 1) ~ pirat, data = HMDA)

fm2 <- lm(I(as.numeric(deny) - 1) ~ pirat + afam, data = HMDA)

fm3 <- glm(deny ~ pirat, family = binomial(link = "probit"), data = HMDA)

fm4 <- glm(deny ~ pirat + afam, family = binomial(link = "probit"), data = HMDA)

fm5 <- glm(deny ~ pirat + afam, family = binomial(link = "logit"), data = HMDA)

## Table 11.1, p. 401

mean(HMDA$pirat)

#> [1] 0.3308136

mean(HMDA$hirat)

#> [1] 0.2553461

mean(HMDA$lvrat)

#> [1] 0.7377759

mean(as.numeric(HMDA$chist))

#> [1] 2.116387

mean(as.numeric(HMDA$mhist))

#> [1] 1.721008

mean(as.numeric(HMDA$phist)-1)

#> [1] 0.07352941

prop.table(table(HMDA$insurance))

#>

#> no yes

#> 0.97983193 0.02016807

prop.table(table(HMDA$selfemp))

#>

#> no yes

#> 0.8836134 0.1163866

prop.table(table(HMDA$single))

#>

#> no yes

#> 0.6067227 0.3932773

prop.table(table(HMDA$hschool))

#>

#> no yes

#> 0.01638655 0.98361345

mean(HMDA$unemp)

#> [1] 3.774496

prop.table(table(HMDA$condomin))

#>

#> no yes

#> 0.7117647 0.2882353

prop.table(table(HMDA$afam))

#>

#> no yes

#> 0.857563 0.142437

prop.table(table(HMDA$deny))

#>

#> no yes

#> 0.8802521 0.1197479

## Table 11.2, pp. 403--404, numbers refer to columns

HMDA$lvrat <- factor(ifelse(HMDA$lvrat < 0.8, "low",

ifelse(HMDA$lvrat >= 0.8 & HMDA$lvrat <= 0.95, "medium", "high")),

levels = c("low", "medium", "high"))

HMDA$mhist <- as.numeric(HMDA$mhist)

HMDA$chist <- as.numeric(HMDA$chist)

fm1 <- lm(I(as.numeric(deny) - 1) ~ afam + pirat + hirat + lvrat + chist + mhist +

phist + insurance + selfemp, data = HMDA)

fm2 <- glm(deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist + insurance +

selfemp, family = binomial, data = HMDA)

fm3 <- glm(deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist + insurance +

selfemp, family = binomial(link = "probit"), data = HMDA)

fm4 <- glm(deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist + insurance +

selfemp + single + hschool + unemp, family = binomial(link = "probit"), data = HMDA)

fm5 <- glm(deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist + insurance +

selfemp + single + hschool + unemp + condomin +

I(mhist==3) + I(mhist==4) + I(chist==3) + I(chist==4) + I(chist==5) + I(chist==6),

family = binomial(link = "probit"), data = HMDA)

fm6 <- glm(deny ~ afam * (pirat + hirat) + lvrat + chist + mhist + phist + insurance +

selfemp + single + hschool + unemp, family = binomial(link = "probit"), data = HMDA)

coeftest(fm1, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.1829933 0.0276089 -6.6281 4.197e-11 ***

#> afamyes 0.0836967 0.0225101 3.7182 0.0002053 ***

#> pirat 0.4487963 0.1133333 3.9600 7.717e-05 ***

#> hirat -0.0480227 0.1093055 -0.4393 0.6604528

#> lvratmedium 0.0314498 0.0127097 2.4745 0.0134125 *

#> lvrathigh 0.1890511 0.0500520 3.7771 0.0001626 ***

#> chist 0.0307716 0.0045737 6.7279 2.150e-11 ***

#> mhist 0.0209104 0.0112637 1.8565 0.0635134 .

#> phistyes 0.1970876 0.0348005 5.6634 1.664e-08 ***

#> insuranceyes 0.7018841 0.0450008 15.5972 < 2.2e-16 ***

#> selfempyes 0.0598438 0.0204759 2.9227 0.0035035 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

fm4r <- update(fm4, . ~ . - single - hschool - unemp)

waldtest(fm4, fm4r, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp

#> Model 2: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp

#> Res.Df Df F Pr(>F)

#> 1 2366

#> 2 2369 -3 5.9463 0.0004893 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r <- update(fm5, . ~ . - single - hschool - unemp)

waldtest(fm5, fm5r, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp + condomin +

#> I(mhist == 3) + I(mhist == 4) + I(chist == 3) + I(chist ==

#> 4) + I(chist == 5) + I(chist == 6)

#> Model 2: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + condomin + I(mhist == 3) + I(mhist ==

#> 4) + I(chist == 3) + I(chist == 4) + I(chist == 5) + I(chist ==

#> 6)

#> Res.Df Df F Pr(>F)

#> 1 2359

#> 2 2362 -3 5.1601 0.001482 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm6r <- update(fm6, . ~ . - single - hschool - unemp)

waldtest(fm6, fm6r, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam * (pirat + hirat) + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp

#> Model 2: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + afam:pirat + afam:hirat

#> Res.Df Df F Pr(>F)

#> 1 2364

#> 2 2367 -3 5.8876 0.0005316 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm5r2 <- update(fm5, . ~ . - I(mhist==3) - I(mhist==4) - I(chist==3) - I(chist==4) -

I(chist==5) - I(chist==6))

waldtest(fm5, fm5r2, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp + condomin +

#> I(mhist == 3) + I(mhist == 4) + I(chist == 3) + I(chist ==

#> 4) + I(chist == 5) + I(chist == 6)

#> Model 2: deny ~ afam + pirat + hirat + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp + condomin

#> Res.Df Df F Pr(>F)

#> 1 2359

#> 2 2365 -6 1.2305 0.2873

fm6r2 <- update(fm6, . ~ . - afam * (pirat + hirat) + pirat + hirat)

waldtest(fm6, fm6r2, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam * (pirat + hirat) + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp

#> Model 2: deny ~ lvrat + chist + mhist + phist + insurance + selfemp +

#> single + hschool + unemp + pirat + hirat

#> Res.Df Df F Pr(>F)

#> 1 2364

#> 2 2367 -3 4.9217 0.00207 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

fm6r3 <- update(fm6, . ~ . - afam * (pirat + hirat) + pirat + hirat + afam)

waldtest(fm6, fm6r3, vcov = sandwich)

#> Wald test

#>

#> Model 1: deny ~ afam * (pirat + hirat) + lvrat + chist + mhist + phist +

#> insurance + selfemp + single + hschool + unemp

#> Model 2: deny ~ lvrat + chist + mhist + phist + insurance + selfemp +

#> single + hschool + unemp + pirat + hirat + afam

#> Res.Df Df F Pr(>F)

#> 1 2364

#> 2 2366 -2 0.2634 0.7685

#########################################################

## Shooting down the "More Guns Less Crime" hypothesis ##

#########################################################

## data

data("Guns", package = "AER")

## Empirical Exercise 10.1

fm1 <- lm(log(violent) ~ law, data = Guns)

fm2 <- lm(log(violent) ~ law + prisoners + density + income +

population + afam + cauc + male, data = Guns)

fm3 <- lm(log(violent) ~ law + prisoners + density + income +

population + afam + cauc + male + state, data = Guns)

fm4 <- lm(log(violent) ~ law + prisoners + density + income +

population + afam + cauc + male + state + year, data = Guns)

coeftest(fm1, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 6.134919 0.019287 318.078 < 2.2e-16 ***

#> lawyes -0.442965 0.047488 -9.328 < 2.2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

coeftest(fm2, vcov = sandwich)

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 2.9817e+00 6.0668e-01 4.9149 1.016e-06 ***

#> lawyes -3.6839e-01 3.4654e-02 -10.6304 < 2.2e-16 ***

#> prisoners 1.6126e-03 1.8000e-04 8.9591 < 2.2e-16 ***

#> density 2.6688e-02 1.4294e-02 1.8671 0.062142 .

#> income 1.2051e-06 7.2498e-06 0.1662 0.868007

#> population 4.2710e-02 3.1345e-03 13.6255 < 2.2e-16 ***

#> afam 8.0853e-02 1.9916e-02 4.0598 5.241e-05 ***

#> cauc 3.1200e-02 9.6897e-03 3.2200 0.001317 **

#> male 8.8709e-03 1.2014e-02 0.7384 0.460435

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

printCoefmat(coeftest(fm3, vcov = sandwich)[1:9,])

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 4.0368e+00 3.7479e-01 10.7708 < 2.2e-16 ***

#> lawyes -4.6141e-02 1.9435e-02 -2.3741 0.01776 *

#> prisoners -7.1008e-05 9.4831e-05 -0.7488 0.45414

#> density -1.7229e-01 1.0221e-01 -1.6857 0.09213 .

#> income -9.2037e-06 6.5619e-06 -1.4026 0.16102

#> population 1.1525e-02 9.4572e-03 1.2186 0.22325

#> afam 1.0428e-01 1.6133e-02 6.4636 1.526e-10 ***

#> cauc 4.0861e-02 5.2487e-03 7.7850 1.585e-14 ***

#> male -5.0273e-02 7.5923e-03 -6.6215 5.518e-11 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

printCoefmat(coeftest(fm4, vcov = sandwich)[1:9,])

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.9720e+00 4.3322e-01 9.1685 < 2.2e-16 ***

#> lawyes -2.7994e-02 1.8692e-02 -1.4976 0.1345

#> prisoners 7.5994e-05 8.0008e-05 0.9498 0.3424

#> density -9.1555e-02 6.2588e-02 -1.4628 0.1438

#> income 9.5859e-07 6.9440e-06 0.1380 0.8902

#> population -4.7545e-03 6.4673e-03 -0.7351 0.4624

#> afam 2.9186e-02 2.0298e-02 1.4379 0.1507

#> cauc 9.2500e-03 8.2188e-03 1.1255 0.2606

#> male 7.3326e-02 1.8116e-02 4.0475 5.542e-05 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

###########################

## US traffic fatalities ##

###########################

## data from Stock and Watson (2007)

data("Fatalities", package = "AER")

Fatalities <- transform(Fatalities,

## fatality rate (number of traffic deaths per 10,000 people living in that state in that year)

frate = fatal/pop * 10000,

## add discretized version of minimum legal drinking age

drinkagec = relevel(cut(drinkage, breaks = 18:22, include.lowest = TRUE, right = FALSE), ref = 4),

## any punishment?

punish = factor(jail == "yes" | service == "yes", labels = c("no", "yes"))

)

## plm package

library("plm")

## for comparability with Stata we use HC1 below

## p. 351, Eq. (10.2)

f1982 <- subset(Fatalities, year == "1982")

fm_1982 <- lm(frate ~ beertax, data = f1982)

coeftest(fm_1982, vcov = vcovHC(fm_1982, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 2.01038 0.14957 13.4408 <2e-16 ***

#> beertax 0.14846 0.13261 1.1196 0.2687

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## p. 353, Eq. (10.3)

f1988 <- subset(Fatalities, year == "1988")

fm_1988 <- lm(frate ~ beertax, data = f1988)

coeftest(fm_1988, vcov = vcovHC(fm_1988, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1.85907 0.11461 16.2205 < 2.2e-16 ***

#> beertax 0.43875 0.12786 3.4314 0.001279 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## pp. 355, Eq. (10.8)

fm_diff <- lm(I(f1988$frate - f1982$frate) ~ I(f1988$beertax - f1982$beertax))

coeftest(fm_diff, vcov = vcovHC(fm_diff, type = "HC1"))

#>

#> t test of coefficients:

#>

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.072037 0.065355 -1.1022 0.276091

#> I(f1988$beertax - f1982$beertax) -1.040973 0.355006 -2.9323 0.005229 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

## pp. 360, Eq. (10.15)

## (1) via formula