Single Factor Asset-Pricing Model Summary: Statistics and Stylized Facts

Source:R/table.CAPM.R

table.CAPM.RdTakes a set of returns and relates them to a benchmark return. Provides a set of measures related to an excess return single factor model, or CAPM.

table.SFM(Ra, Rb, scale = NA, Rf = 0, digits = 4)Arguments

- Ra

a vector of returns to test, e.g., the asset to be examined

- Rb

a matrix, data.frame, or timeSeries of benchmark(s) to test the asset against.

- scale

number of periods in a year (daily scale = 252, monthly scale = 12, quarterly scale = 4)

- Rf

risk free rate, in same period as your returns

- digits

number of digits to round results to

Details

This table will show statistics pertaining to an asset against a set of benchmarks, or statistics for a set of assets against a benchmark.

Examples

# CRAN does not allow examples to load suggested packages in one of its tests

data(managers)

table.SFM(managers[,1:3], managers[,8], Rf = managers[,10])

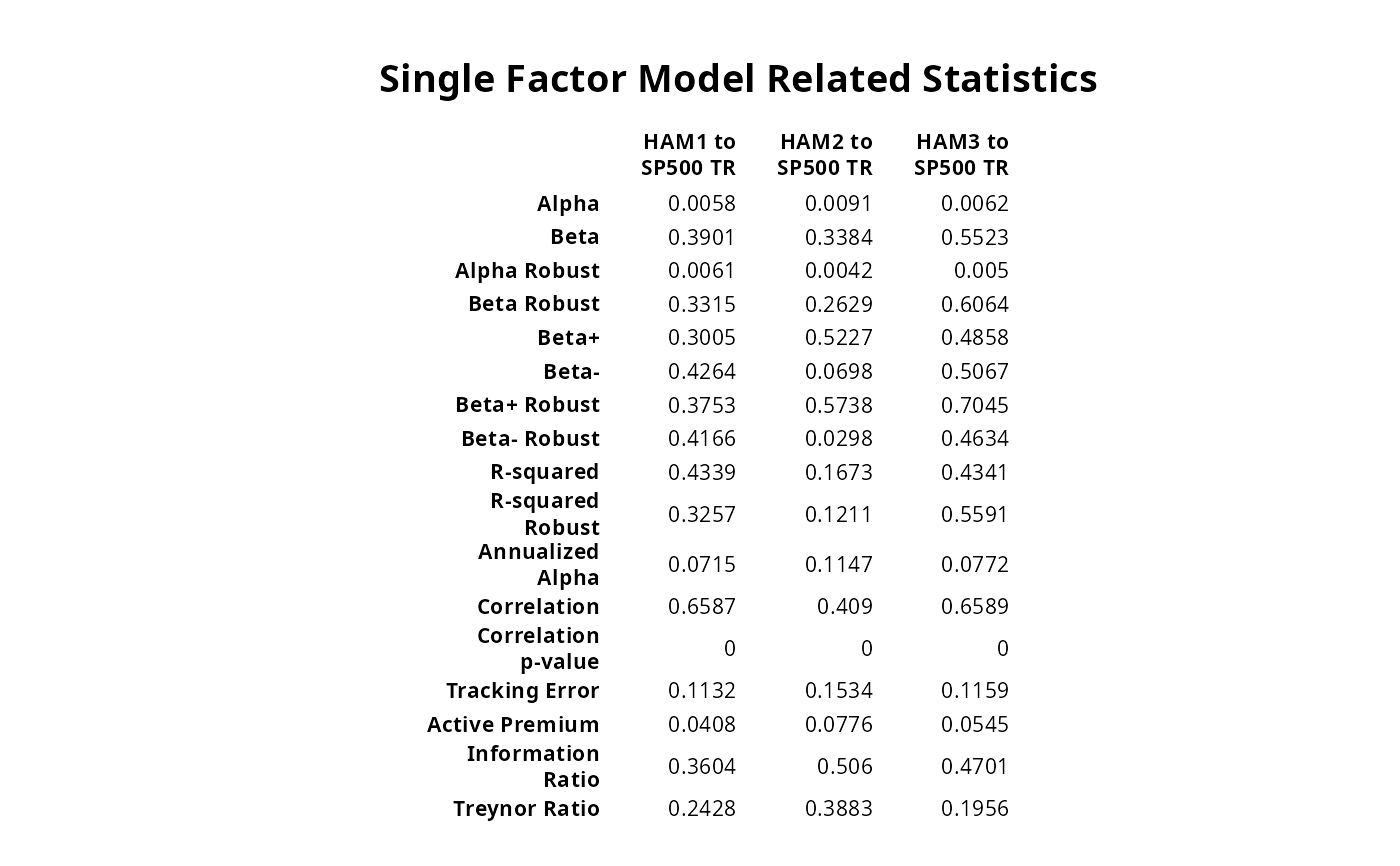

#> HAM1 to SP500 TR HAM2 to SP500 TR HAM3 to SP500 TR

#> Alpha 0.0058 0.0091 0.0062

#> Beta 0.3901 0.3384 0.5523

#> Alpha Robust 0.0061 0.0042 0.0050

#> Beta Robust 0.3315 0.2629 0.6064

#> Beta+ 0.3005 0.5227 0.4858

#> Beta- 0.4264 0.0698 0.5067

#> Beta+ Robust 0.3753 0.5738 0.7045

#> Beta- Robust 0.4166 0.0298 0.4634

#> R-squared 0.4339 0.1673 0.4341

#> R-squared Robust 0.3257 0.1211 0.5591

#> Annualized Alpha 0.0715 0.1147 0.0772

#> Correlation 0.6587 0.4090 0.6589

#> Correlation p-value 0.0000 0.0000 0.0000

#> Tracking Error 0.1132 0.1534 0.1159

#> Active Premium 0.0408 0.0776 0.0545

#> Information Ratio 0.3604 0.5060 0.4701

#> Treynor Ratio 0.2428 0.3883 0.1956

result = table.SFM(managers[,1:3], managers[,8], Rf = managers[,10])

require(Hmisc)

textplot(result, rmar = 0.8, cmar = 1.5, max.cex=.9,

halign = "center", valign = "top", row.valign="center",

wrap.rownames=15, wrap.colnames=10, mar = c(0,0,3,0)+0.1)

title(main="Single Factor Model Related Statistics")