Periodic returns in a bar chart with risk metric overlay

Source:R/chart.BarVaR.R, R/charts.BarVaR.R

chart.BarVaR.RdPlots the periodic returns as a bar chart overlayed with a risk metric calculation.

chart.BarVaR(

R,

width = 0,

gap = 12,

methods = c("none", "ModifiedVaR", "GaussianVaR", "HistoricalVaR", "StdDev",

"ModifiedES", "GaussianES", "HistoricalES"),

p = 0.95,

clean = c("none", "boudt", "geltner"),

all = FALSE,

...,

show.clean = FALSE,

show.horizontal = FALSE,

show.symmetric = FALSE,

show.endvalue = FALSE,

show.greenredbars = FALSE,

legend.loc = "bottomleft",

ylim = NA,

lwd = 2,

colorset = 1:12,

lty = c(1, 2, 4, 5, 6),

ypad = 0,

legend.cex = 0.8,

plot.engine = "default"

)

charts.BarVaR(

R,

main = "Returns",

cex.legend = 0.8,

colorset = 1:12,

ylim = NA,

...,

perpanel = NULL,

show.yaxis = c("all", "firstonly", "alternating", "none")

)Arguments

- R

an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns

- width

periods specified for rolling-period calculations. Note that VaR, ES, and Std Dev with width=0 are calculated from the start of the timeseries

- gap

numeric number of periods from start of series to use to train risk calculation

- methods

Used to select the risk parameter of trailing

widthreturns to use: May be any of:none - does not add a risk line,

ModifiedVaR - uses Cornish-Fisher modified VaR,

GaussianVaR - uses traditional Value at Risk,

HistoricalVaR - calculates historical Value at Risk,

ModifiedES - uses Cornish-Fisher modified Expected Shortfall,

GaussianES - uses traditional Expected Shortfall,

HistoricalES - calculates historical Expected Shortfall,

StdDev - per-period standard deviation

- p

confidence level for

VaRorModifiedVaRcalculation, default is .99- clean

the method to use to clean outliers from return data prior to risk metric estimation. See

Return.cleanandVaRfor more detail- all

if TRUE, calculates risk lines for each column given in R. If FALSE, only calculates the risk line for the first column

- ...

any other passthru parameters to

chart.TimeSeries- show.clean

if TRUE and a method for 'clean' is specified, overlays the actual data with the "cleaned" data. See

Return.cleanfor more detail- show.horizontal

if TRUE, shows a line across the timeseries at the value of the most recent VaR estimate, to help the reader evaluate the number of exceptions thus far

- show.symmetric

if TRUE and the metric is symmetric, this will show the metric's positive values as well as negative values, such as for method "StdDev".

- show.endvalue

if TRUE, show the final (out of sample) value

- show.greenredbars

if TRUE, show the per-period returns using green and red bars for positive and negative returns

- legend.loc

legend location, such as in

chart.TimeSeries- ylim

set the y-axis limit, same as in

plot- lwd

set the line width, same as in

plot- colorset

color palette to use, such as in

chart.TimeSeries- lty

set the line type, same as in

plot- ypad

adds a numerical padding to the y-axis to keep the data away when legend.loc="bottom". See examples below.

- legend.cex

sets the legend text size, such as in

chart.TimeSeries- plot.engine

Choose the engine for plotting, including "default","dygraph","ggplot","plotly" and "googleVis"

- main

sets the title text, such as in

chart.TimeSeries- cex.legend

sets the legend text size, such as in

chart.TimeSeries- perpanel

default NULL, controls column display

- show.yaxis

one of "all", "firstonly", "alternating", or "none" to control where y axis is plotted in multipanel charts

Details

Note that StdDev and VaR are symmetric calculations, so a high

and low measure will be plotted. ModifiedVaR, on the other hand, is

assymetric and only a lower bound will be drawn.

Creates a plot of time on the x-axis and vertical lines for each period to indicate value on the y-axis. Overlays a line to indicate the value of a risk metric calculated at that time period.

charts.BarVaR places multile bar charts in a single

graphic, with associated risk measures

See also

Examples

if (FALSE) # not run on CRAN because of example time

data(managers)

# plain

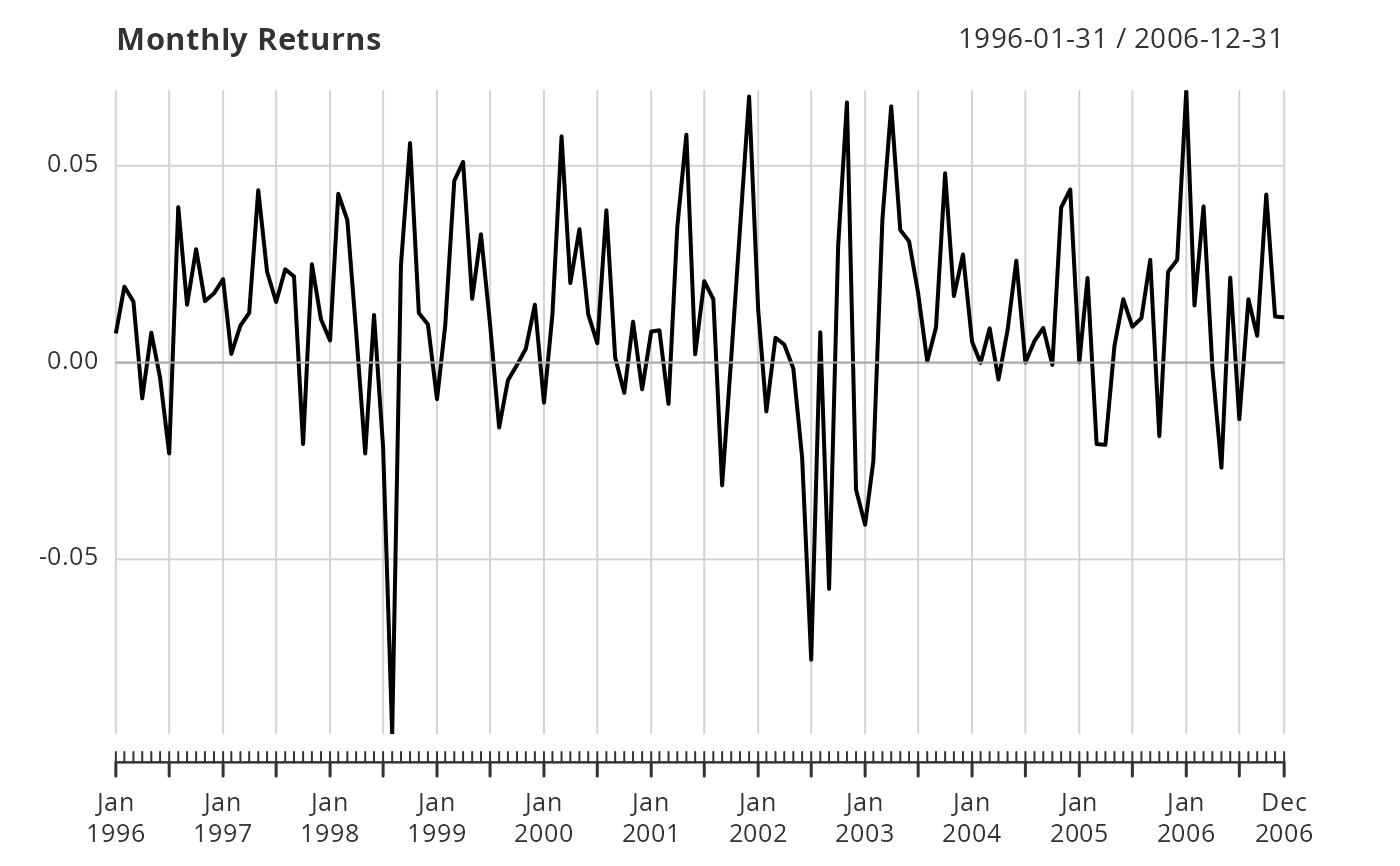

chart.BarVaR(managers[,1,drop=FALSE], main="Monthly Returns")

# with risk line

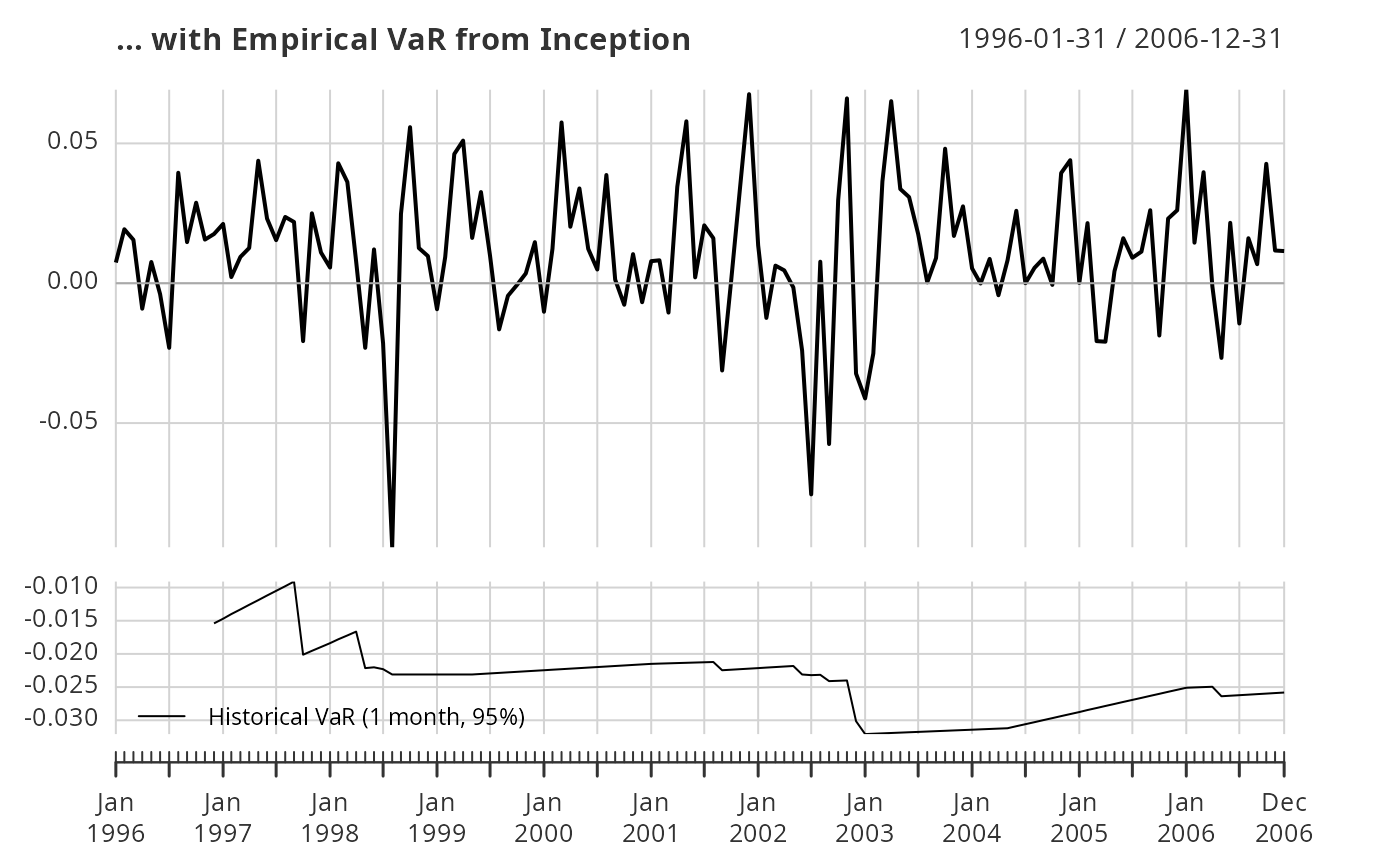

chart.BarVaR(managers[,1,drop=FALSE],

methods="HistoricalVaR",

main="... with Empirical VaR from Inception")

# with risk line

chart.BarVaR(managers[,1,drop=FALSE],

methods="HistoricalVaR",

main="... with Empirical VaR from Inception")

# with lines for all managers in the sample

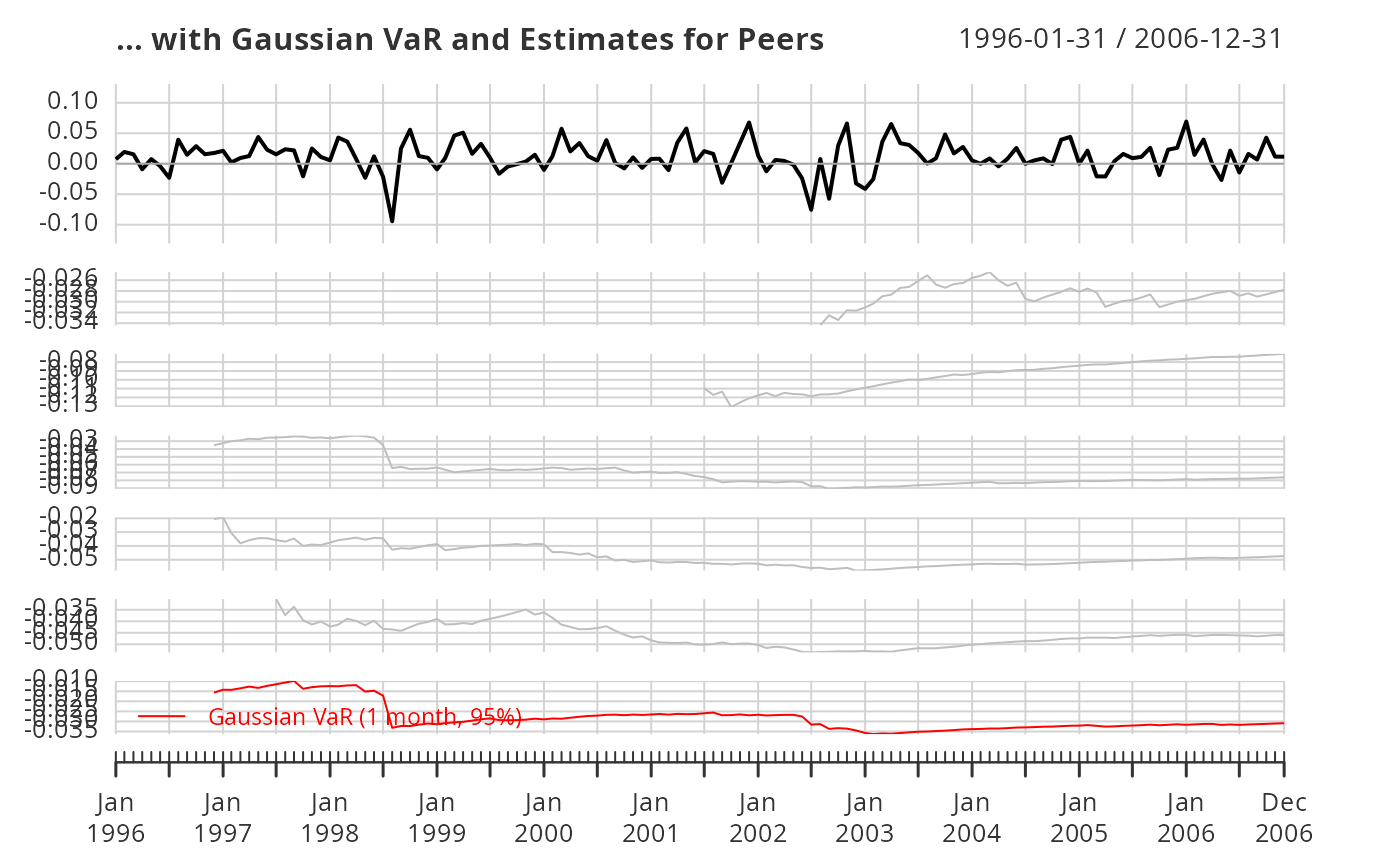

chart.BarVaR(managers[,1:6],

methods="GaussianVaR",

all=TRUE, lty=1, lwd=2,

colorset= c("red", rep("gray", 5)),

main="... with Gaussian VaR and Estimates for Peers")

# with lines for all managers in the sample

chart.BarVaR(managers[,1:6],

methods="GaussianVaR",

all=TRUE, lty=1, lwd=2,

colorset= c("red", rep("gray", 5)),

main="... with Gaussian VaR and Estimates for Peers")

# with multiple methods

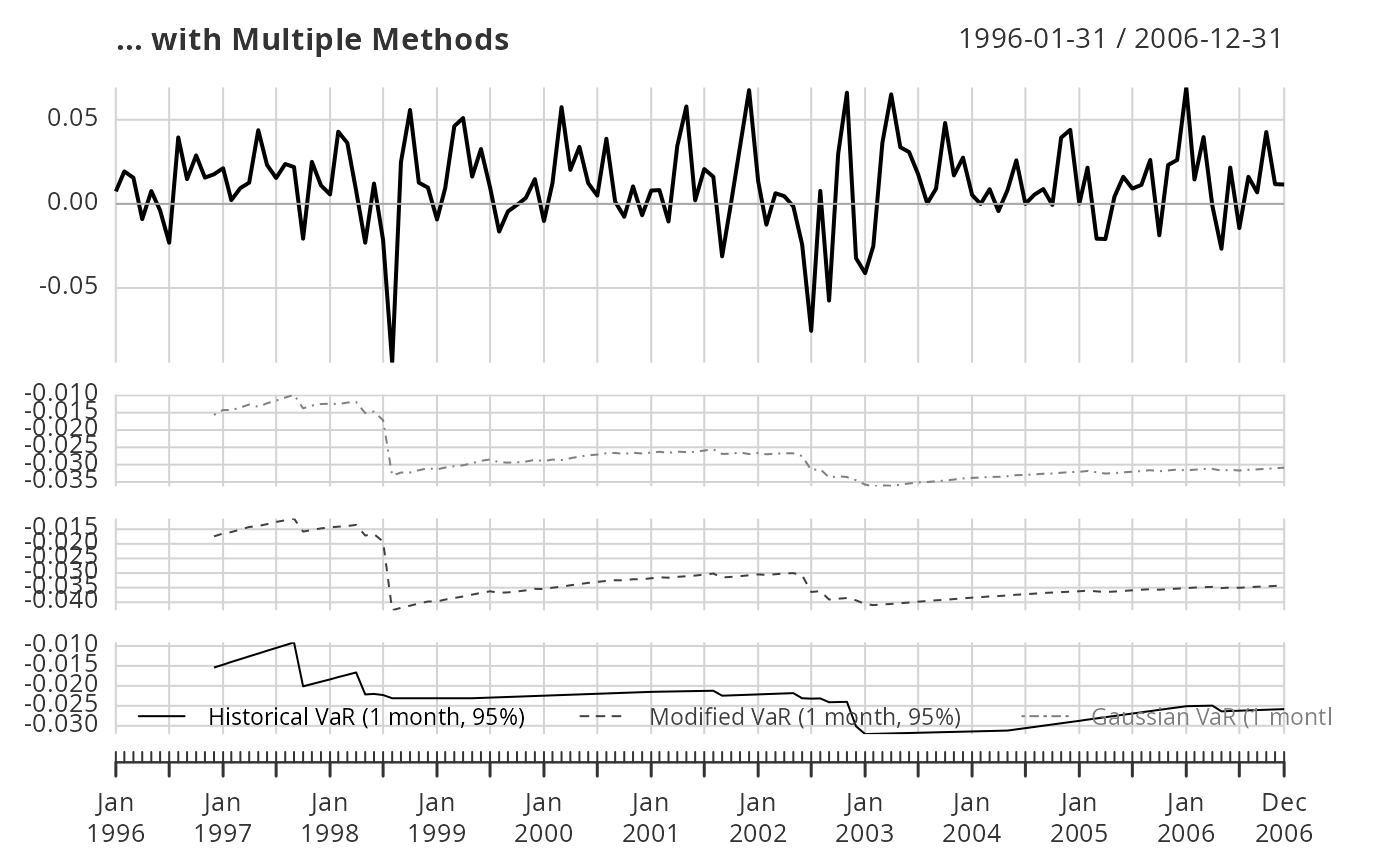

chart.BarVaR(managers[,1,drop=FALSE],

methods=c("HistoricalVaR", "ModifiedVaR", "GaussianVaR"),

main="... with Multiple Methods")

# with multiple methods

chart.BarVaR(managers[,1,drop=FALSE],

methods=c("HistoricalVaR", "ModifiedVaR", "GaussianVaR"),

main="... with Multiple Methods")

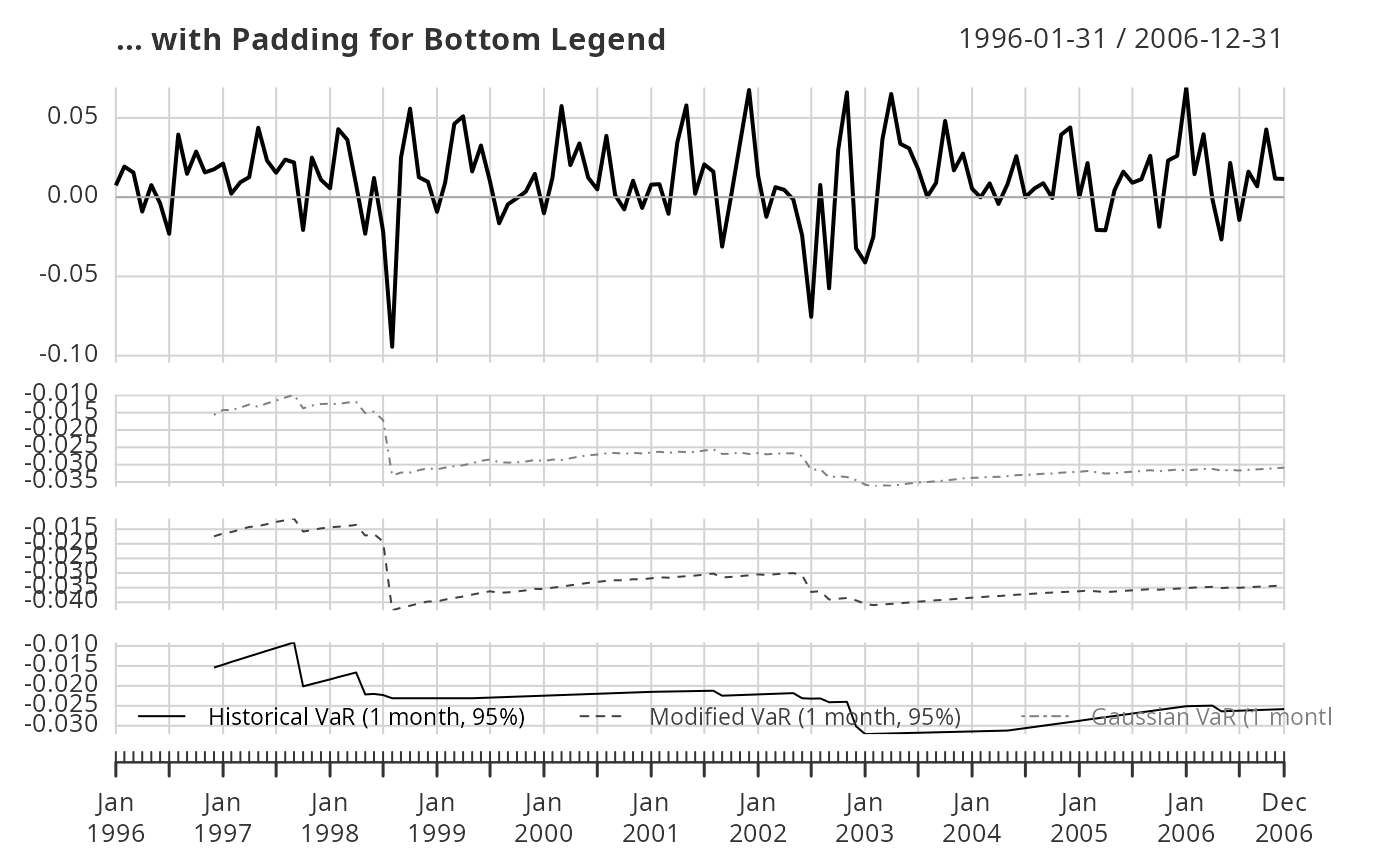

# cleaned up a bit

chart.BarVaR(managers[,1,drop=FALSE],

methods=c("HistoricalVaR", "ModifiedVaR", "GaussianVaR"),

lwd=2, ypad=.01,

main="... with Padding for Bottom Legend")

# cleaned up a bit

chart.BarVaR(managers[,1,drop=FALSE],

methods=c("HistoricalVaR", "ModifiedVaR", "GaussianVaR"),

lwd=2, ypad=.01,

main="... with Padding for Bottom Legend")

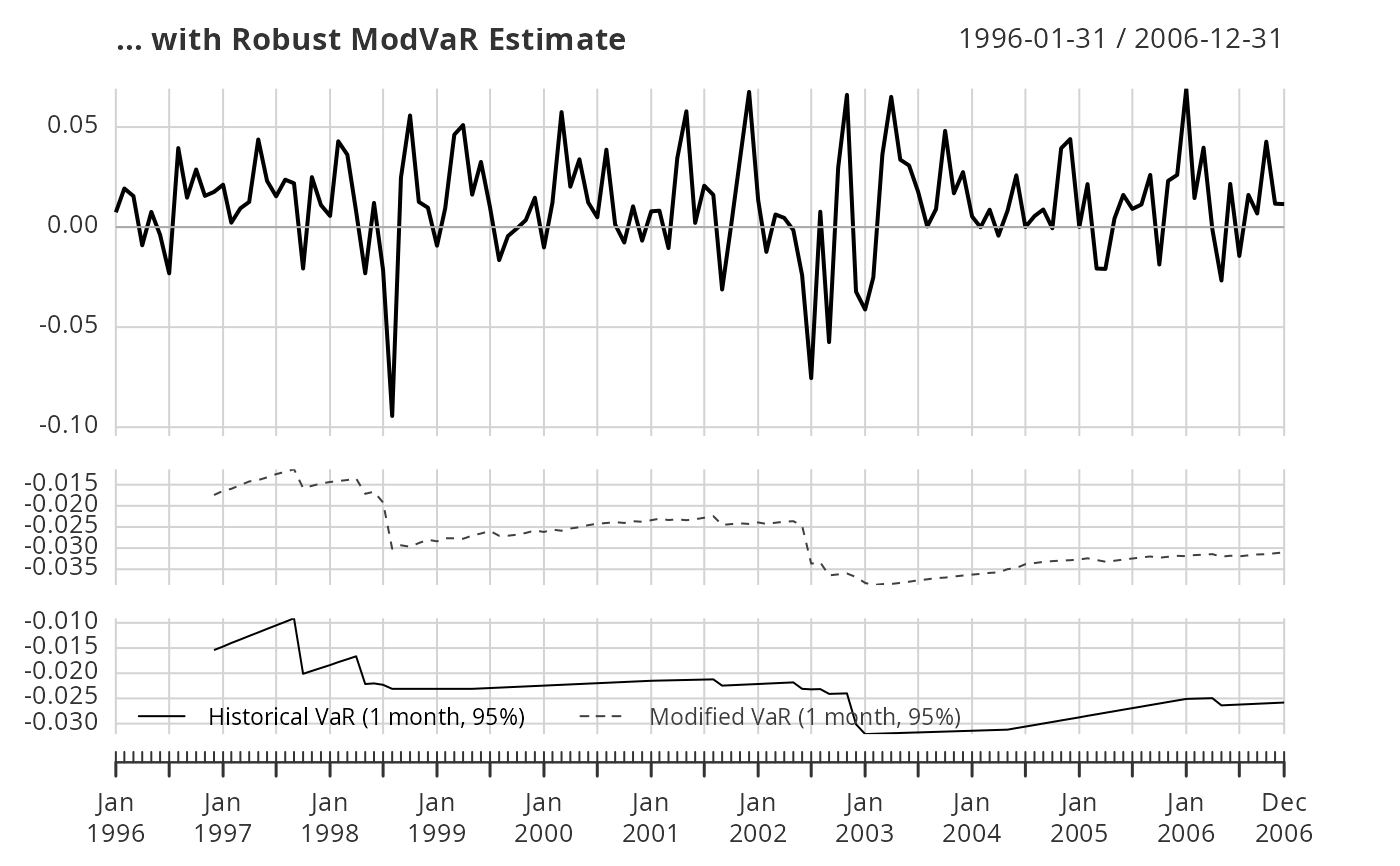

# with 'cleaned' data for VaR estimates

chart.BarVaR(managers[,1,drop=FALSE],

methods=c("HistoricalVaR", "ModifiedVaR"),

lwd=2, ypad=.01, clean="boudt",

main="... with Robust ModVaR Estimate")

# with 'cleaned' data for VaR estimates

chart.BarVaR(managers[,1,drop=FALSE],

methods=c("HistoricalVaR", "ModifiedVaR"),

lwd=2, ypad=.01, clean="boudt",

main="... with Robust ModVaR Estimate")

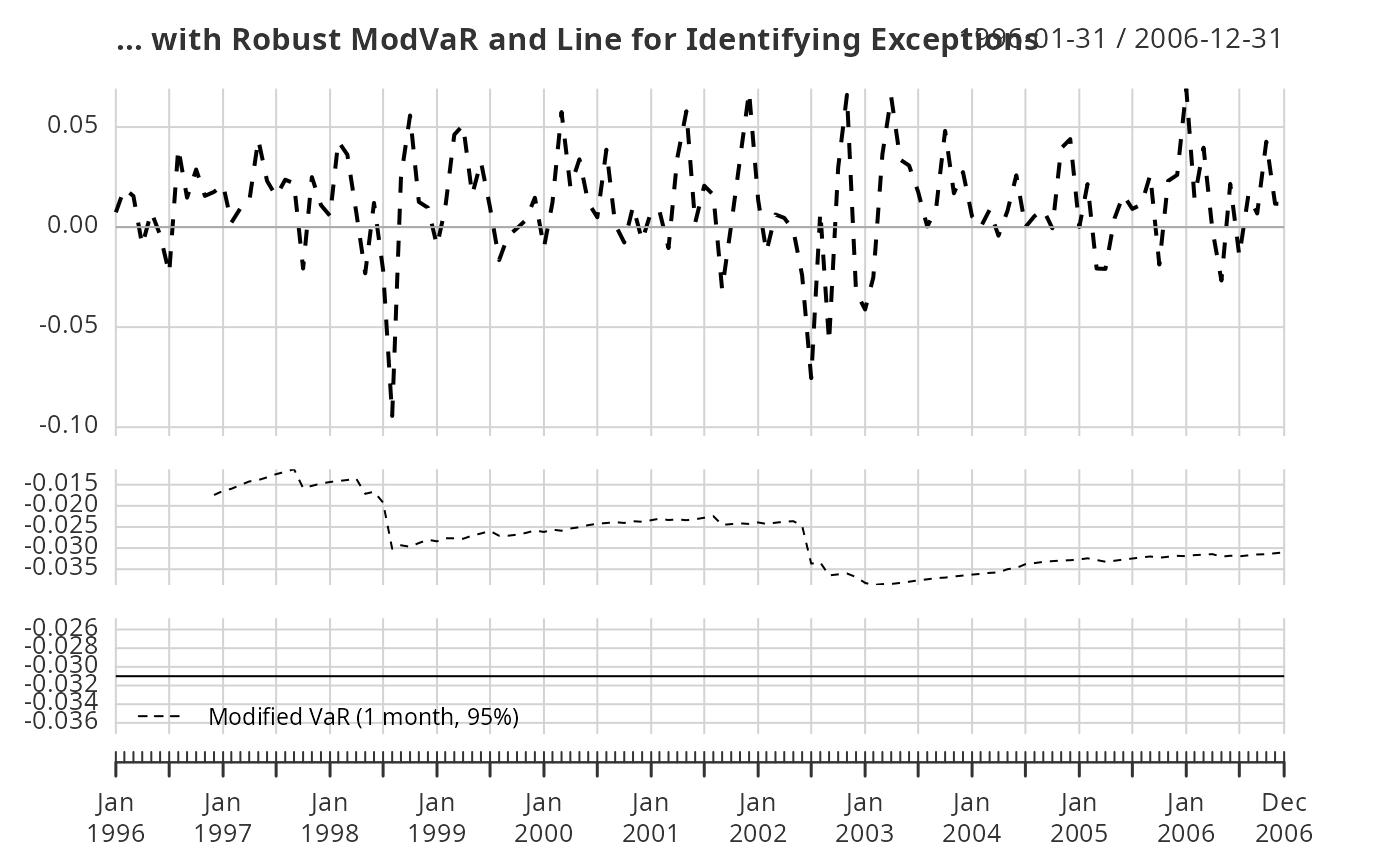

# Cornish Fisher VaR estimated with cleaned data,

# with horizontal line to show exceptions

chart.BarVaR(managers[,1,drop=FALSE],

methods="ModifiedVaR",

lwd=2, ypad=.01, clean="boudt",

show.horizontal=TRUE, lty=2,

main="... with Robust ModVaR and Line for Identifying Exceptions")

# Cornish Fisher VaR estimated with cleaned data,

# with horizontal line to show exceptions

chart.BarVaR(managers[,1,drop=FALSE],

methods="ModifiedVaR",

lwd=2, ypad=.01, clean="boudt",

show.horizontal=TRUE, lty=2,

main="... with Robust ModVaR and Line for Identifying Exceptions")

# \dontrun{}

# \dontrun{}