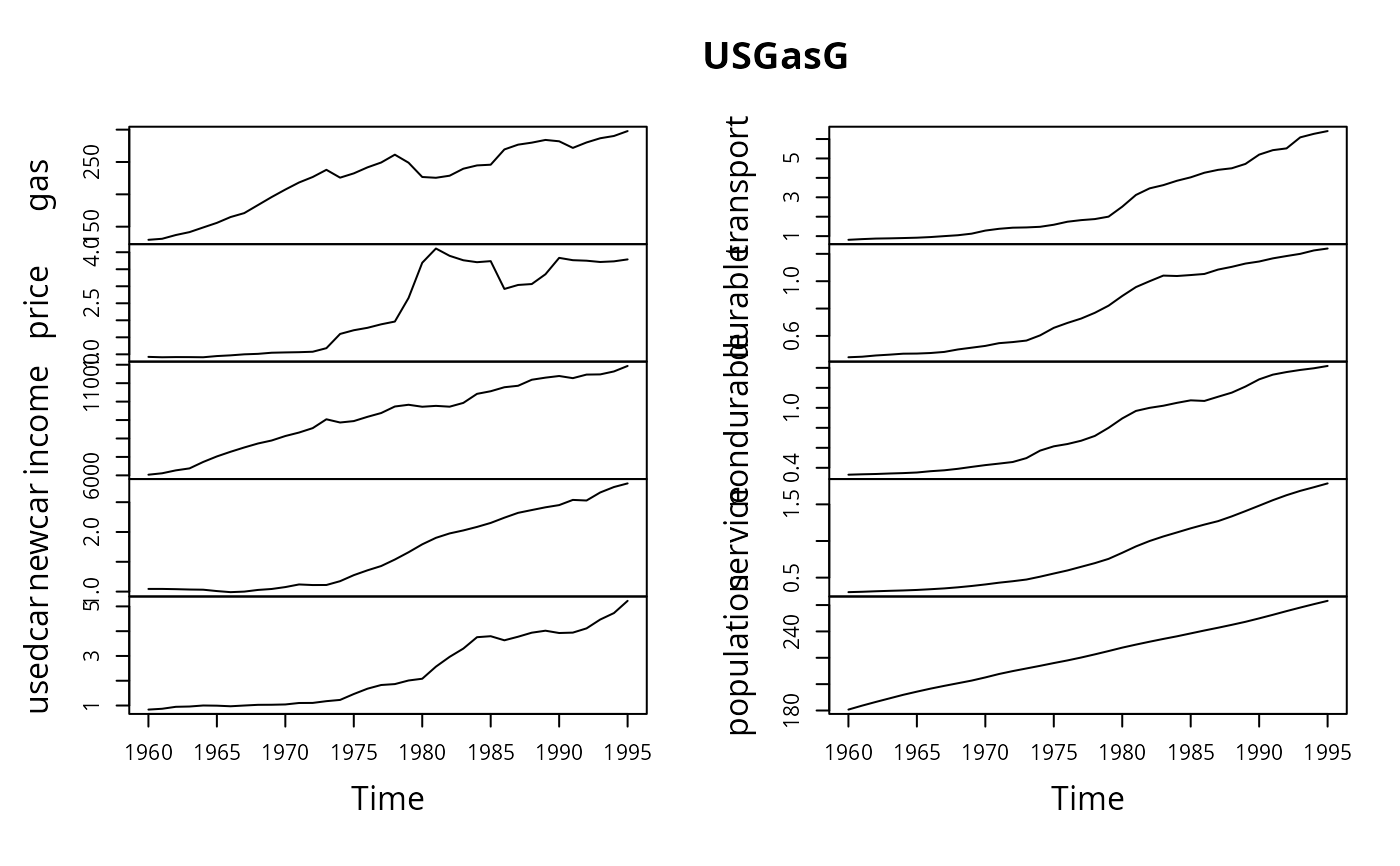

US Gasoline Market Data (1960–1995, Greene)

USGasG.RdTime series data on the US gasoline market.

Usage

data("USGasG")Format

An annual multiple time series from 1960 to 1995 with 10 variables.

- gas

Total US gasoline consumption (computed as total expenditure divided by price index).

- price

Price index for gasoline.

- income

Per capita disposable income.

- newcar

Price index for new cars.

- usedcar

Price index for used cars.

- transport

Price index for public transportation.

- durable

Aggregate price index for consumer durables.

- nondurable

Aggregate price index for consumer nondurables.

- service

Aggregate price index for consumer services.

- population

US total population in millions.

Source

Online complements to Greene (2003). Table F2.2.

https://pages.stern.nyu.edu/~wgreene/Text/tables/tablelist5.htm

References

Greene, W.H. (2003). Econometric Analysis, 5th edition. Upper Saddle River, NJ: Prentice Hall.

Examples

data("USGasG", package = "AER")

plot(USGasG)

## Greene (2003)

## Example 2.3

fm <- lm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar),

data = as.data.frame(USGasG))

summary(fm)

#>

#> Call:

#> lm(formula = log(gas/population) ~ log(price) + log(income) +

#> log(newcar) + log(usedcar), data = as.data.frame(USGasG))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.065042 -0.018842 0.001528 0.020786 0.058084

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -12.34184 0.67489 -18.287 <2e-16 ***

#> log(price) -0.05910 0.03248 -1.819 0.0786 .

#> log(income) 1.37340 0.07563 18.160 <2e-16 ***

#> log(newcar) -0.12680 0.12699 -0.998 0.3258

#> log(usedcar) -0.11871 0.08134 -1.459 0.1545

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.03304 on 31 degrees of freedom

#> Multiple R-squared: 0.958, Adjusted R-squared: 0.9526

#> F-statistic: 176.7 on 4 and 31 DF, p-value: < 2.2e-16

#>

## Example 4.4

## estimates and standard errors (note different offset for intercept)

coef(fm)

#> (Intercept) log(price) log(income) log(newcar) log(usedcar)

#> -12.34184054 -0.05909513 1.37339912 -0.12679667 -0.11870847

sqrt(diag(vcov(fm)))

#> (Intercept) log(price) log(income) log(newcar) log(usedcar)

#> 0.67489471 0.03248496 0.07562767 0.12699351 0.08133710

## confidence interval

confint(fm, parm = "log(income)")

#> 2.5 % 97.5 %

#> log(income) 1.219155 1.527643

## test linear hypothesis

linearHypothesis(fm, "log(income) = 1")

#>

#> Linear hypothesis test:

#> log(income) = 1

#>

#> Model 1: restricted model

#> Model 2: log(gas/population) ~ log(price) + log(income) + log(newcar) +

#> log(usedcar)

#>

#> Res.Df RSS Df Sum of Sq F Pr(>F)

#> 1 32 0.060445

#> 2 31 0.033837 1 0.026608 24.377 2.57e-05 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

## Example 7.6

## re-used in Example 8.3

trend <- 1:nrow(USGasG)

shock <- factor(time(USGasG) > 1973, levels = c(FALSE, TRUE),

labels = c("before", "after"))

## 1960-1995

fm1 <- lm(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = as.data.frame(USGasG))

summary(fm1)

#>

#> Call:

#> lm(formula = log(gas/population) ~ log(income) + log(price) +

#> log(newcar) + log(usedcar) + trend, data = as.data.frame(USGasG))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.055238 -0.017715 0.003659 0.016481 0.053522

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -17.385790 1.679289 -10.353 2.03e-11 ***

#> log(income) 1.954626 0.192854 10.135 3.34e-11 ***

#> log(price) -0.115530 0.033479 -3.451 0.00168 **

#> log(newcar) 0.205282 0.152019 1.350 0.18700

#> log(usedcar) -0.129274 0.071412 -1.810 0.08028 .

#> trend -0.019118 0.005957 -3.210 0.00316 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.02898 on 30 degrees of freedom

#> Multiple R-squared: 0.9687, Adjusted R-squared: 0.9635

#> F-statistic: 185.8 on 5 and 30 DF, p-value: < 2.2e-16

#>

## pooled

fm2 <- lm(log(gas/population) ~ shock + log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = as.data.frame(USGasG))

summary(fm2)

#>

#> Call:

#> lm(formula = log(gas/population) ~ shock + log(income) + log(price) +

#> log(newcar) + log(usedcar) + trend, data = as.data.frame(USGasG))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.045360 -0.019697 0.003931 0.015112 0.047550

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -16.374402 1.456263 -11.244 4.33e-12 ***

#> shockafter 0.077311 0.021872 3.535 0.00139 **

#> log(income) 1.838167 0.167258 10.990 7.43e-12 ***

#> log(price) -0.178005 0.033508 -5.312 1.06e-05 ***

#> log(newcar) 0.209842 0.129267 1.623 0.11534

#> log(usedcar) -0.128132 0.060721 -2.110 0.04359 *

#> trend -0.016862 0.005105 -3.303 0.00255 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.02464 on 29 degrees of freedom

#> Multiple R-squared: 0.9781, Adjusted R-squared: 0.9736

#> F-statistic: 216.3 on 6 and 29 DF, p-value: < 2.2e-16

#>

## segmented

fm3 <- lm(log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) +

log(usedcar) + trend), data = as.data.frame(USGasG))

summary(fm3)

#>

#> Call:

#> lm(formula = log(gas/population) ~ shock/(log(income) + log(price) +

#> log(newcar) + log(usedcar) + trend), data = as.data.frame(USGasG))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.027349 -0.006332 0.001295 0.007159 0.022016

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -4.13439 5.03963 -0.820 0.420075

#> shockafter -4.74111 5.51576 -0.860 0.398538

#> shockbefore:log(income) 0.42400 0.57973 0.731 0.471633

#> shockafter:log(income) 1.01408 0.24904 4.072 0.000439 ***

#> shockbefore:log(price) 0.09455 0.24804 0.381 0.706427

#> shockafter:log(price) -0.24237 0.03490 -6.946 3.5e-07 ***

#> shockbefore:log(newcar) 0.58390 0.21670 2.695 0.012665 *

#> shockafter:log(newcar) 0.33017 0.15789 2.091 0.047277 *

#> shockbefore:log(usedcar) -0.33462 0.15215 -2.199 0.037738 *

#> shockafter:log(usedcar) -0.05537 0.04426 -1.251 0.222972

#> shockbefore:trend 0.02637 0.01762 1.497 0.147533

#> shockafter:trend -0.01262 0.00329 -3.835 0.000798 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.01488 on 24 degrees of freedom

#> Multiple R-squared: 0.9934, Adjusted R-squared: 0.9904

#> F-statistic: 328.5 on 11 and 24 DF, p-value: < 2.2e-16

#>

## Chow test

anova(fm3, fm1)

#> Analysis of Variance Table

#>

#> Model 1: log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) +

#> log(usedcar) + trend)

#> Model 2: log(gas/population) ~ log(income) + log(price) + log(newcar) +

#> log(usedcar) + trend

#> Res.Df RSS Df Sum of Sq F Pr(>F)

#> 1 24 0.0053144

#> 2 30 0.0251878 -6 -0.019873 14.958 4.595e-07 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

library("strucchange")

sctest(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = USGasG, point = c(1973, 1), type = "Chow")

#>

#> Chow test

#>

#> data: log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + trend

#> F = 14.958, p-value = 4.595e-07

#>

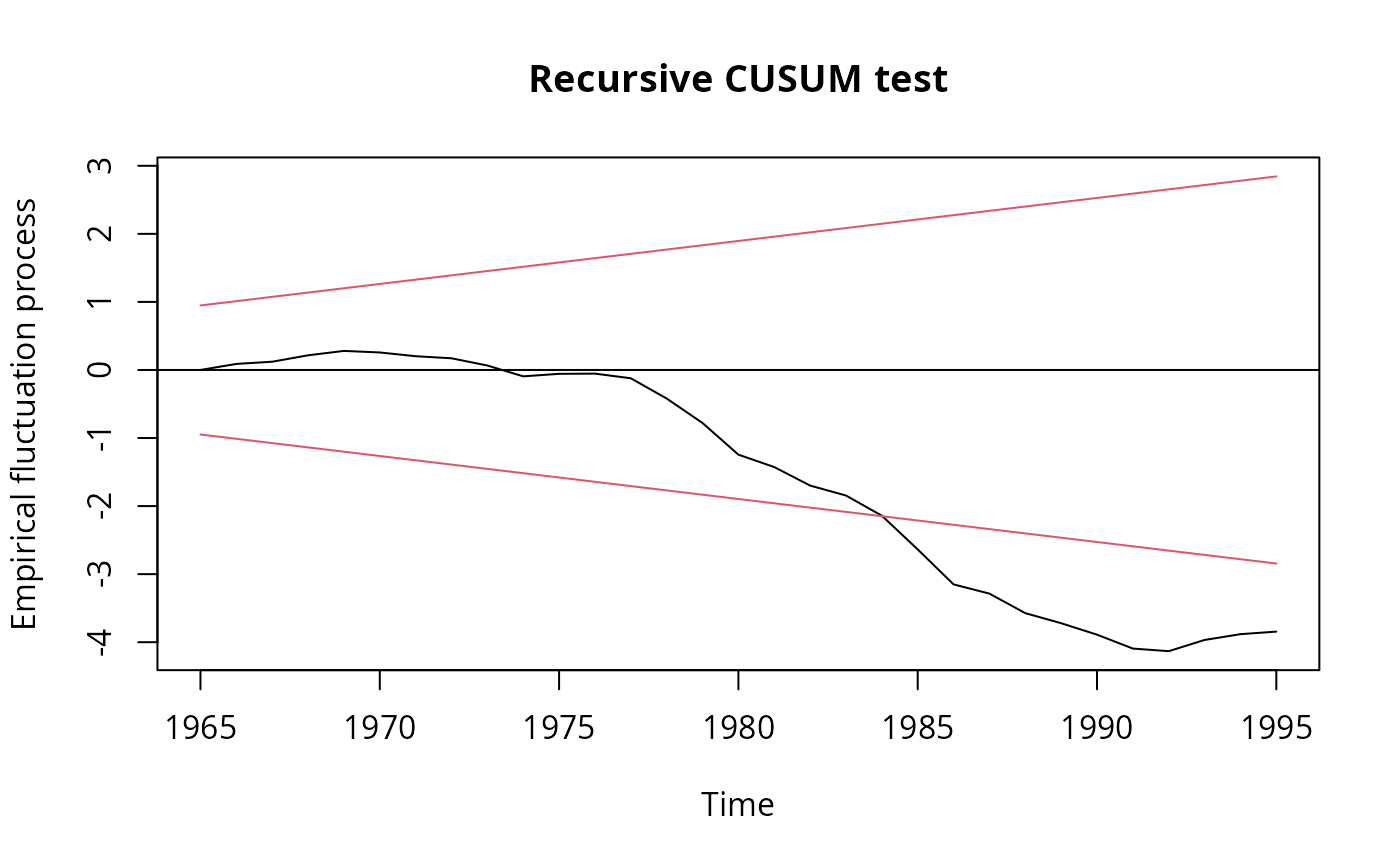

## Recursive CUSUM test

rcus <- efp(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = USGasG, type = "Rec-CUSUM")

plot(rcus)

## Greene (2003)

## Example 2.3

fm <- lm(log(gas/population) ~ log(price) + log(income) + log(newcar) + log(usedcar),

data = as.data.frame(USGasG))

summary(fm)

#>

#> Call:

#> lm(formula = log(gas/population) ~ log(price) + log(income) +

#> log(newcar) + log(usedcar), data = as.data.frame(USGasG))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.065042 -0.018842 0.001528 0.020786 0.058084

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -12.34184 0.67489 -18.287 <2e-16 ***

#> log(price) -0.05910 0.03248 -1.819 0.0786 .

#> log(income) 1.37340 0.07563 18.160 <2e-16 ***

#> log(newcar) -0.12680 0.12699 -0.998 0.3258

#> log(usedcar) -0.11871 0.08134 -1.459 0.1545

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.03304 on 31 degrees of freedom

#> Multiple R-squared: 0.958, Adjusted R-squared: 0.9526

#> F-statistic: 176.7 on 4 and 31 DF, p-value: < 2.2e-16

#>

## Example 4.4

## estimates and standard errors (note different offset for intercept)

coef(fm)

#> (Intercept) log(price) log(income) log(newcar) log(usedcar)

#> -12.34184054 -0.05909513 1.37339912 -0.12679667 -0.11870847

sqrt(diag(vcov(fm)))

#> (Intercept) log(price) log(income) log(newcar) log(usedcar)

#> 0.67489471 0.03248496 0.07562767 0.12699351 0.08133710

## confidence interval

confint(fm, parm = "log(income)")

#> 2.5 % 97.5 %

#> log(income) 1.219155 1.527643

## test linear hypothesis

linearHypothesis(fm, "log(income) = 1")

#>

#> Linear hypothesis test:

#> log(income) = 1

#>

#> Model 1: restricted model

#> Model 2: log(gas/population) ~ log(price) + log(income) + log(newcar) +

#> log(usedcar)

#>

#> Res.Df RSS Df Sum of Sq F Pr(>F)

#> 1 32 0.060445

#> 2 31 0.033837 1 0.026608 24.377 2.57e-05 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

## Example 7.6

## re-used in Example 8.3

trend <- 1:nrow(USGasG)

shock <- factor(time(USGasG) > 1973, levels = c(FALSE, TRUE),

labels = c("before", "after"))

## 1960-1995

fm1 <- lm(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = as.data.frame(USGasG))

summary(fm1)

#>

#> Call:

#> lm(formula = log(gas/population) ~ log(income) + log(price) +

#> log(newcar) + log(usedcar) + trend, data = as.data.frame(USGasG))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.055238 -0.017715 0.003659 0.016481 0.053522

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -17.385790 1.679289 -10.353 2.03e-11 ***

#> log(income) 1.954626 0.192854 10.135 3.34e-11 ***

#> log(price) -0.115530 0.033479 -3.451 0.00168 **

#> log(newcar) 0.205282 0.152019 1.350 0.18700

#> log(usedcar) -0.129274 0.071412 -1.810 0.08028 .

#> trend -0.019118 0.005957 -3.210 0.00316 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.02898 on 30 degrees of freedom

#> Multiple R-squared: 0.9687, Adjusted R-squared: 0.9635

#> F-statistic: 185.8 on 5 and 30 DF, p-value: < 2.2e-16

#>

## pooled

fm2 <- lm(log(gas/population) ~ shock + log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = as.data.frame(USGasG))

summary(fm2)

#>

#> Call:

#> lm(formula = log(gas/population) ~ shock + log(income) + log(price) +

#> log(newcar) + log(usedcar) + trend, data = as.data.frame(USGasG))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.045360 -0.019697 0.003931 0.015112 0.047550

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -16.374402 1.456263 -11.244 4.33e-12 ***

#> shockafter 0.077311 0.021872 3.535 0.00139 **

#> log(income) 1.838167 0.167258 10.990 7.43e-12 ***

#> log(price) -0.178005 0.033508 -5.312 1.06e-05 ***

#> log(newcar) 0.209842 0.129267 1.623 0.11534

#> log(usedcar) -0.128132 0.060721 -2.110 0.04359 *

#> trend -0.016862 0.005105 -3.303 0.00255 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.02464 on 29 degrees of freedom

#> Multiple R-squared: 0.9781, Adjusted R-squared: 0.9736

#> F-statistic: 216.3 on 6 and 29 DF, p-value: < 2.2e-16

#>

## segmented

fm3 <- lm(log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) +

log(usedcar) + trend), data = as.data.frame(USGasG))

summary(fm3)

#>

#> Call:

#> lm(formula = log(gas/population) ~ shock/(log(income) + log(price) +

#> log(newcar) + log(usedcar) + trend), data = as.data.frame(USGasG))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.027349 -0.006332 0.001295 0.007159 0.022016

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -4.13439 5.03963 -0.820 0.420075

#> shockafter -4.74111 5.51576 -0.860 0.398538

#> shockbefore:log(income) 0.42400 0.57973 0.731 0.471633

#> shockafter:log(income) 1.01408 0.24904 4.072 0.000439 ***

#> shockbefore:log(price) 0.09455 0.24804 0.381 0.706427

#> shockafter:log(price) -0.24237 0.03490 -6.946 3.5e-07 ***

#> shockbefore:log(newcar) 0.58390 0.21670 2.695 0.012665 *

#> shockafter:log(newcar) 0.33017 0.15789 2.091 0.047277 *

#> shockbefore:log(usedcar) -0.33462 0.15215 -2.199 0.037738 *

#> shockafter:log(usedcar) -0.05537 0.04426 -1.251 0.222972

#> shockbefore:trend 0.02637 0.01762 1.497 0.147533

#> shockafter:trend -0.01262 0.00329 -3.835 0.000798 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.01488 on 24 degrees of freedom

#> Multiple R-squared: 0.9934, Adjusted R-squared: 0.9904

#> F-statistic: 328.5 on 11 and 24 DF, p-value: < 2.2e-16

#>

## Chow test

anova(fm3, fm1)

#> Analysis of Variance Table

#>

#> Model 1: log(gas/population) ~ shock/(log(income) + log(price) + log(newcar) +

#> log(usedcar) + trend)

#> Model 2: log(gas/population) ~ log(income) + log(price) + log(newcar) +

#> log(usedcar) + trend

#> Res.Df RSS Df Sum of Sq F Pr(>F)

#> 1 24 0.0053144

#> 2 30 0.0251878 -6 -0.019873 14.958 4.595e-07 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

library("strucchange")

sctest(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = USGasG, point = c(1973, 1), type = "Chow")

#>

#> Chow test

#>

#> data: log(gas/population) ~ log(income) + log(price) + log(newcar) + log(usedcar) + trend

#> F = 14.958, p-value = 4.595e-07

#>

## Recursive CUSUM test

rcus <- efp(log(gas/population) ~ log(income) + log(price) + log(newcar) +

log(usedcar) + trend, data = USGasG, type = "Rec-CUSUM")

plot(rcus)

sctest(rcus)

#>

#> Recursive CUSUM test

#>

#> data: rcus

#> S = 1.4977, p-value = 0.0002437

#>

## Note: Greene's remark that the break is in 1984 (where the process crosses its

## boundary) is wrong. The break appears to be no later than 1976.

## More examples can be found in:

## help("Greene2003")

sctest(rcus)

#>

#> Recursive CUSUM test

#>

#> data: rcus

#> S = 1.4977, p-value = 0.0002437

#>

## Note: Greene's remark that the break is in 1984 (where the process crosses its

## boundary) is wrong. The break appears to be no later than 1976.

## More examples can be found in:

## help("Greene2003")