Consumption of Non-Durables in the UK

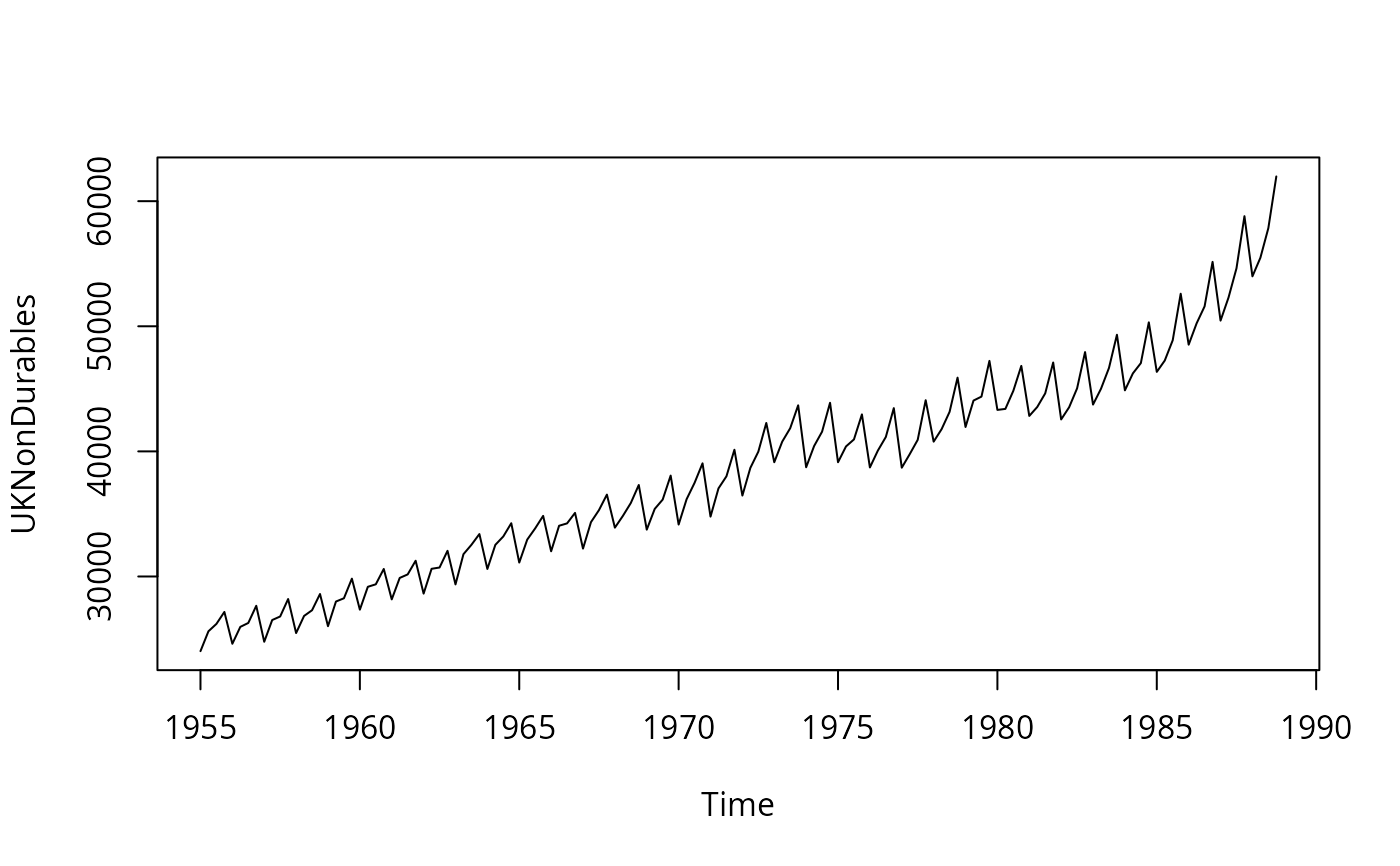

UKNonDurables.RdTime series of consumption of non-durables in the UK (in 1985 prices).

Usage

data("UKNonDurables")References

Osborn, D.R. (1988). A Survey of Seasonality in UK Macroeconomic Variables. International Journal of Forecasting, 6, 327–336.

Franses, P.H. (1998). Time Series Models for Business and Economic Forecasting. Cambridge, UK: Cambridge University Press.

Examples

data("UKNonDurables")

plot(UKNonDurables)

## EACF tables (Franses 1998, p. 99)

ctrafo <- function(x) residuals(lm(x ~ factor(cycle(x))))

ddiff <- function(x) diff(diff(x, frequency(x)), 1)

eacf <- function(y, lag = 12) {

stopifnot(all(lag > 0))

if(length(lag) < 2) lag <- 1:lag

rval <- sapply(

list(y = y, dy = diff(y), cdy = ctrafo(diff(y)),

Dy = diff(y, frequency(y)), dDy = ddiff(y)),

function(x) acf(x, plot = FALSE, lag.max = max(lag))$acf[lag + 1])

rownames(rval) <- lag

return(rval)

}

## Franses (1998), Table 5.2

round(eacf(log(UKNonDurables)), digits = 3)

#> y dy cdy Dy dDy

#> 1 0.928 -0.463 -0.074 0.779 -0.164

#> 2 0.900 -0.014 -0.359 0.625 0.050

#> 3 0.876 -0.481 -0.034 0.449 0.048

#> 4 0.891 0.947 0.554 0.248 -0.444

#> 5 0.823 -0.438 0.023 0.238 0.236

#> 6 0.795 -0.014 -0.390 0.130 -0.118

#> 7 0.771 -0.471 -0.045 0.082 0.115

#> 8 0.788 0.910 0.491 -0.014 0.023

#> 9 0.723 -0.421 -0.081 -0.125 -0.251

#> 10 0.697 -0.014 -0.328 -0.133 0.122

#> 11 0.674 -0.464 -0.148 -0.196 -0.131

#> 12 0.691 0.877 0.414 -0.196 -0.001

## Franses (1998), Equation 5.51

## (Franses: sma1 = -0.632 (0.069))

arima(log(UKNonDurables), c(0, 1, 0), c(0, 1, 1))

#>

#> Call:

#> arima(x = log(UKNonDurables), order = c(0, 1, 0), seasonal = c(0, 1, 1))

#>

#> Coefficients:

#> sma1

#> -0.6095

#> s.e. 0.0711

#>

#> sigma^2 estimated as 0.0001234: log likelihood = 402.71, aic = -801.42

## EACF tables (Franses 1998, p. 99)

ctrafo <- function(x) residuals(lm(x ~ factor(cycle(x))))

ddiff <- function(x) diff(diff(x, frequency(x)), 1)

eacf <- function(y, lag = 12) {

stopifnot(all(lag > 0))

if(length(lag) < 2) lag <- 1:lag

rval <- sapply(

list(y = y, dy = diff(y), cdy = ctrafo(diff(y)),

Dy = diff(y, frequency(y)), dDy = ddiff(y)),

function(x) acf(x, plot = FALSE, lag.max = max(lag))$acf[lag + 1])

rownames(rval) <- lag

return(rval)

}

## Franses (1998), Table 5.2

round(eacf(log(UKNonDurables)), digits = 3)

#> y dy cdy Dy dDy

#> 1 0.928 -0.463 -0.074 0.779 -0.164

#> 2 0.900 -0.014 -0.359 0.625 0.050

#> 3 0.876 -0.481 -0.034 0.449 0.048

#> 4 0.891 0.947 0.554 0.248 -0.444

#> 5 0.823 -0.438 0.023 0.238 0.236

#> 6 0.795 -0.014 -0.390 0.130 -0.118

#> 7 0.771 -0.471 -0.045 0.082 0.115

#> 8 0.788 0.910 0.491 -0.014 0.023

#> 9 0.723 -0.421 -0.081 -0.125 -0.251

#> 10 0.697 -0.014 -0.328 -0.133 0.122

#> 11 0.674 -0.464 -0.148 -0.196 -0.131

#> 12 0.691 0.877 0.414 -0.196 -0.001

## Franses (1998), Equation 5.51

## (Franses: sma1 = -0.632 (0.069))

arima(log(UKNonDurables), c(0, 1, 0), c(0, 1, 1))

#>

#> Call:

#> arima(x = log(UKNonDurables), order = c(0, 1, 0), seasonal = c(0, 1, 1))

#>

#> Coefficients:

#> sma1

#> -0.6095

#> s.e. 0.0711

#>

#> sigma^2 estimated as 0.0001234: log likelihood = 402.71, aic = -801.42