Consumer Price Index in Argentina

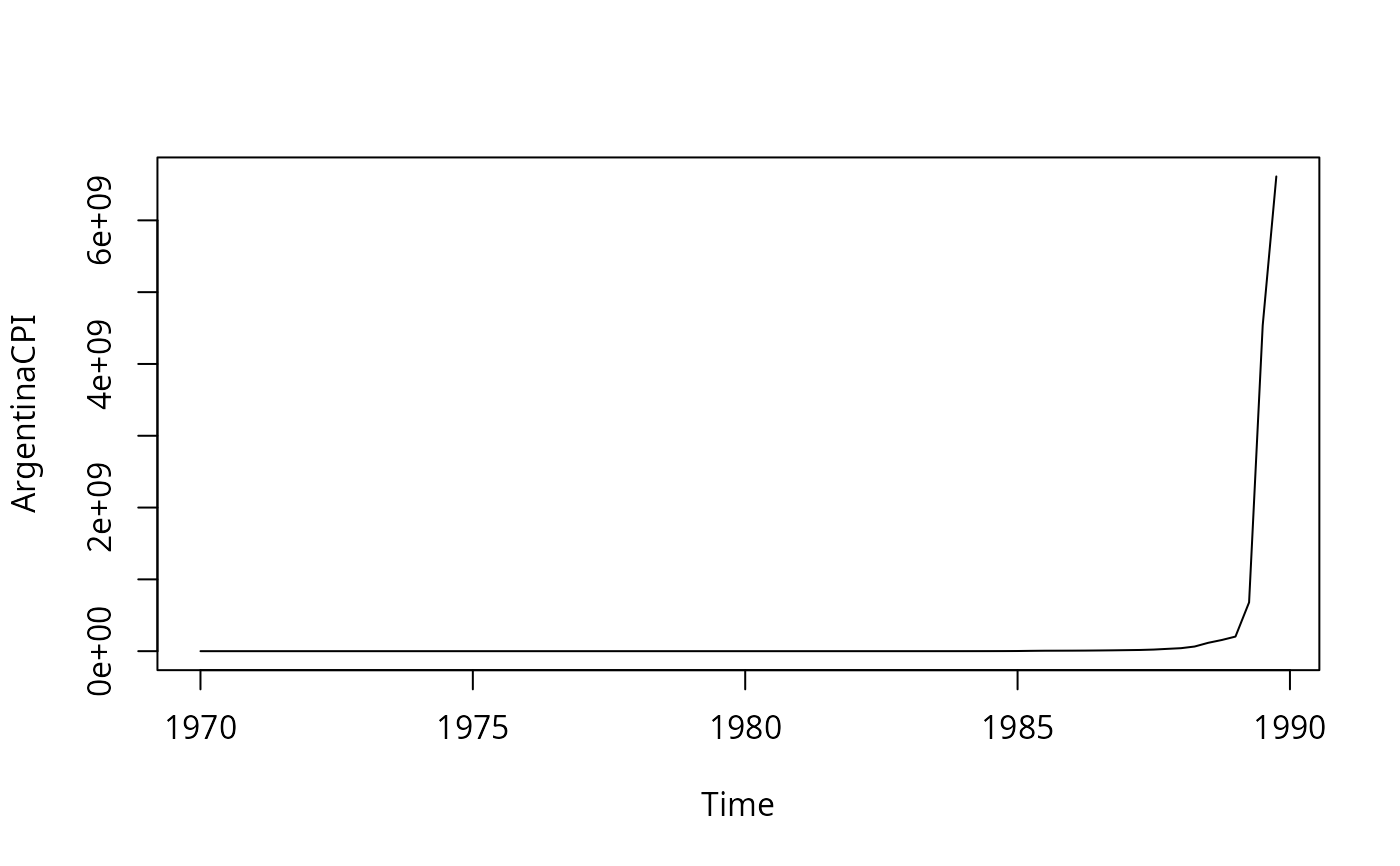

ArgentinaCPI.RdTime series of consumer price index (CPI) in Argentina (index with 1969(4) = 1).

Usage

data("ArgentinaCPI")References

De Ruyter van Steveninck, M.A. (1996). The Impact of Capital Imports; Argentina 1970–1989. Amsterdam: Thesis Publishers.

Franses, P.H. (1998). Time Series Models for Business and Economic Forecasting. Cambridge, UK: Cambridge University Press.

Examples

#> Loading required namespace: dynlm

data("ArgentinaCPI")

plot(ArgentinaCPI)

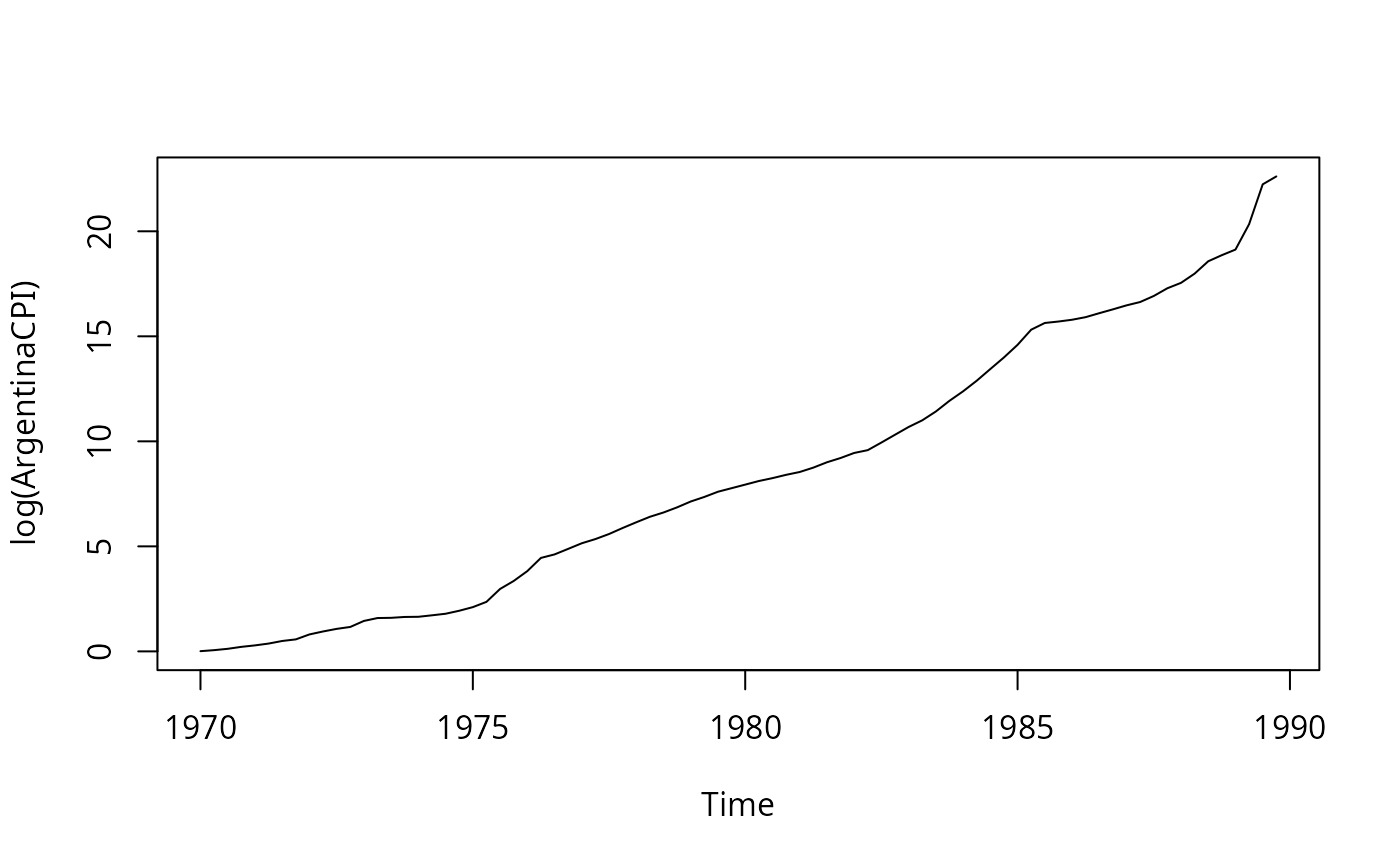

plot(log(ArgentinaCPI))

plot(log(ArgentinaCPI))

library("dynlm")

## estimation sample 1970.3-1988.4 means

acpi <- window(ArgentinaCPI, start = c(1970,1), end = c(1988,4))

## eq. (3.90), p.54

acpi_ols <- dynlm(d(log(acpi)) ~ L(d(log(acpi))))

summary(acpi_ols)

#>

#> Time series regression with "ts" data:

#> Start = 1970(3), End = 1988(4)

#>

#> Call:

#> dynlm(formula = d(log(acpi)) ~ L(d(log(acpi))))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.35308 -0.05569 -0.01312 0.04952 0.35938

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.07764 0.02458 3.158 0.00232 **

#> L(d(log(acpi))) 0.70359 0.08205 8.575 1.29e-12 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.1156 on 72 degrees of freedom

#> Multiple R-squared: 0.5053, Adjusted R-squared: 0.4984

#> F-statistic: 73.53 on 1 and 72 DF, p-value: 1.293e-12

#>

## alternatively

ar(diff(log(acpi)), order.max = 1, method = "ols")

#>

#> Call:

#> ar(x = diff(log(acpi)), order.max = 1, method = "ols")

#>

#> Coefficients:

#> 1

#> 0.7036

#>

#> Intercept: 0.003122 (0.01326)

#>

#> Order selected 1 sigma^2 estimated as 0.013

library("dynlm")

## estimation sample 1970.3-1988.4 means

acpi <- window(ArgentinaCPI, start = c(1970,1), end = c(1988,4))

## eq. (3.90), p.54

acpi_ols <- dynlm(d(log(acpi)) ~ L(d(log(acpi))))

summary(acpi_ols)

#>

#> Time series regression with "ts" data:

#> Start = 1970(3), End = 1988(4)

#>

#> Call:

#> dynlm(formula = d(log(acpi)) ~ L(d(log(acpi))))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.35308 -0.05569 -0.01312 0.04952 0.35938

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.07764 0.02458 3.158 0.00232 **

#> L(d(log(acpi))) 0.70359 0.08205 8.575 1.29e-12 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.1156 on 72 degrees of freedom

#> Multiple R-squared: 0.5053, Adjusted R-squared: 0.4984

#> F-statistic: 73.53 on 1 and 72 DF, p-value: 1.293e-12

#>

## alternatively

ar(diff(log(acpi)), order.max = 1, method = "ols")

#>

#> Call:

#> ar(x = diff(log(acpi)), order.max = 1, method = "ols")

#>

#> Coefficients:

#> 1

#> 0.7036

#>

#> Intercept: 0.003122 (0.01326)

#>

#> Order selected 1 sigma^2 estimated as 0.013