Fit GARCH Models to Time Series

garch.RdFit a Generalized Autoregressive Conditional Heteroscedastic GARCH(p, q) time series model to the data by computing the maximum-likelihood estimates of the conditionally normal model.

Usage

garch(x, order = c(1, 1), series = NULL, control = garch.control(...), ...)

garch.control(maxiter = 200, trace = TRUE, start = NULL,

grad = c("analytical","numerical"), abstol = max(1e-20, .Machine$double.eps^2),

reltol = max(1e-10, .Machine$double.eps^(2/3)), xtol = sqrt(.Machine$double.eps),

falsetol = 1e2 * .Machine$double.eps, ...)Arguments

- x

a numeric vector or time series.

- order

a two dimensional integer vector giving the orders of the model to fit.

order[2]corresponds to the ARCH part andorder[1]to the GARCH part.- series

name for the series. Defaults to

deparse(substitute(x)).- control

a list of control parameters as set up by

garch.control.- maxiter

gives the maximum number of log-likelihood function evaluations

maxiterand the maximum number of iterations2*maxiterthe optimizer is allowed to compute.- trace

logical. Trace optimizer output?

- start

If given this numeric vector is used as the initial estimate of the GARCH coefficients. Default initialization is to set the GARCH parameters to slightly positive values and to initialize the intercept such that the unconditional variance of the initial GARCH is equal to the variance of

x.- grad

character indicating whether analytical gradients or a numerical approximation is used for the optimization.

- abstol

absolute function convergence tolerance.

- reltol

relative function convergence tolerance.

- xtol

coefficient-convergence tolerance.

- falsetol

false convergence tolerance.

- ...

additional arguments for

qrwhen computing the asymptotic covariance matrix.

Details

garch uses a Quasi-Newton optimizer to find the maximum

likelihood estimates of the conditionally normal model. The first

max(p, q) values are assumed to be fixed. The optimizer uses a hessian

approximation computed from the BFGS update. Only a Cholesky factor

of the Hessian approximation is stored. For more details see Dennis

et al. (1981), Dennis and Mei (1979), Dennis and More (1977), and

Goldfarb (1976). The gradient is either computed analytically or

using a numerical approximation.

Value

A list of class "garch" with the following elements:

- order

the order of the fitted model.

- coef

estimated GARCH coefficients for the fitted model.

- n.likeli

the negative log-likelihood function evaluated at the coefficient estimates (apart from some constant).

- n.used

the number of observations of

x.- residuals

the series of residuals.

- fitted.values

the bivariate series of conditional standard deviation predictions for

x.- series

the name of the series

x.- frequency

the frequency of the series

x.- call

the call of the

garchfunction.- vcov

outer product of gradient estimate of the asymptotic-theory covariance matrix for the coefficient estimates.

References

A. K. Bera and M. L. Higgins (1993): ARCH Models: Properties, Estimation and Testing. J. Economic Surveys 7 305–362. doi:10.1111/j.1467-6419.1993.tb00170.x .

T. Bollerslev (1986): Generalized Autoregressive Conditional Heteroscedasticity. Journal of Econometrics 31, 307–327. doi:10.1016/0304-4076(86)90063-1 .

R. F. Engle (1982): Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 50, 987–1008. doi:10.1093/oso/9780198774310.003.0001 .

J. E. Dennis, D. M. Gay, and R. E. Welsch (1981): Algorithm 573 — An Adaptive Nonlinear Least-Squares Algorithm. ACM Transactions on Mathematical Software 7, 369–383. doi:10.1145/355958.355966 .

J. E. Dennis and H. H. W. Mei (1979): Two New Unconstrained Optimization Algorithms which use Function and Gradient Values. J. Optim. Theory Applic. 28, 453–482. doi:10.1007/BF00932218 .

J. E. Dennis and J. J. More (1977): Quasi-Newton Methods, Motivation and Theory. SIAM Rev. 19, 46–89. doi:10.1137/1019005 .

D. Goldfarb (1976): Factorized Variable Metric Methods for Unconstrained Optimization. Math. Comput. 30, 796–811. doi:10.2307/2005399 .

See also

summary.garch for summarizing GARCH model fits;

garch-methods for further methods.

Examples

n <- 1100

a <- c(0.1, 0.5, 0.2) # ARCH(2) coefficients

e <- rnorm(n)

x <- double(n)

x[1:2] <- rnorm(2, sd = sqrt(a[1]/(1.0-a[2]-a[3])))

for(i in 3:n) # Generate ARCH(2) process

{

x[i] <- e[i]*sqrt(a[1]+a[2]*x[i-1]^2+a[3]*x[i-2]^2)

}

x <- ts(x[101:1100])

x.arch <- garch(x, order = c(0,2)) # Fit ARCH(2)

#>

#> ***** ESTIMATION WITH ANALYTICAL GRADIENT *****

#>

#>

#> I INITIAL X(I) D(I)

#>

#> 1 2.363190e-01 1.000e+00

#> 2 5.000000e-02 1.000e+00

#> 3 5.000000e-02 1.000e+00

#>

#> IT NF F RELDF PRELDF RELDX STPPAR D*STEP NPRELDF

#> 0 1 -2.325e+02

#> 1 3 -2.767e+02 1.60e-01 1.95e-01 1.7e-01 5.4e+03 1.0e-01 5.25e+02

#> 2 4 -2.960e+02 6.50e-02 8.53e-02 2.3e-01 2.8e+00 1.0e-01 2.47e+00

#> 3 5 -2.987e+02 8.98e-03 1.04e-01 1.7e-01 2.0e+00 1.0e-01 3.66e+02

#> 4 6 -3.149e+02 5.15e-02 4.21e-02 8.5e-02 2.0e+00 5.0e-02 6.29e+01

#> 5 8 -3.161e+02 3.78e-03 5.49e-03 2.6e-02 3.4e+00 1.9e-02 2.03e+01

#> 6 9 -3.175e+02 4.50e-03 5.92e-03 2.6e-02 2.0e+00 1.9e-02 1.43e+01

#> 7 10 -3.199e+02 7.52e-03 9.82e-03 5.3e-02 2.0e+00 3.9e-02 7.96e+00

#> 8 11 -3.222e+02 7.07e-03 1.54e-02 9.6e-02 2.0e+00 7.8e-02 2.03e+00

#> 9 13 -3.229e+02 2.14e-03 6.49e-03 2.7e-02 2.0e+00 3.6e-02 2.13e-01

#> 10 14 -3.237e+02 2.36e-03 3.49e-03 4.0e-02 2.0e+00 3.6e-02 1.75e-01

#> 11 15 -3.239e+02 7.96e-04 1.20e-03 3.0e-02 1.9e+00 3.6e-02 3.78e-02

#> 12 17 -3.240e+02 2.36e-04 4.66e-04 8.1e-03 7.1e+00 1.0e-02 4.45e-02

#> 13 18 -3.241e+02 2.92e-04 6.62e-04 7.8e-03 2.0e+00 1.0e-02 1.02e-01

#> 14 19 -3.242e+02 2.59e-04 4.09e-04 8.6e-03 2.0e+00 1.0e-02 1.73e-02

#> 15 20 -3.242e+02 2.77e-05 1.40e-04 8.7e-03 1.8e+00 1.0e-02 1.57e-03

#> 16 21 -3.242e+02 1.08e-04 1.23e-04 7.6e-03 8.3e-01 1.0e-02 1.67e-04

#> 17 23 -3.242e+02 6.68e-06 2.42e-05 2.8e-03 1.5e+00 3.0e-03 3.36e-05

#> 18 24 -3.242e+02 1.02e-05 1.27e-05 2.9e-03 5.7e-01 3.0e-03 1.40e-05

#> 19 25 -3.242e+02 8.70e-07 1.36e-06 1.1e-03 0.0e+00 1.2e-03 1.36e-06

#> 20 26 -3.242e+02 1.33e-07 1.34e-07 3.3e-04 0.0e+00 3.5e-04 1.34e-07

#> 21 27 -3.242e+02 1.50e-12 1.51e-12 9.0e-07 0.0e+00 1.0e-06 1.51e-12

#>

#> ***** RELATIVE FUNCTION CONVERGENCE *****

#>

#> FUNCTION -3.242267e+02 RELDX 8.952e-07

#> FUNC. EVALS 27 GRAD. EVALS 22

#> PRELDF 1.509e-12 NPRELDF 1.509e-12

#>

#> I FINAL X(I) D(I) G(I)

#>

#> 1 9.157780e-02 1.000e+00 1.712e-05

#> 2 5.183412e-01 1.000e+00 1.519e-06

#> 3 1.342126e-01 1.000e+00 9.057e-06

#>

summary(x.arch) # Diagnostic tests

#>

#> Call:

#> garch(x = x, order = c(0, 2))

#>

#> Model:

#> GARCH(0,2)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -3.0820433 -0.6446973 -0.0002197 0.7076624 3.1693239

#>

#> Coefficient(s):

#> Estimate Std. Error t value Pr(>|t|)

#> a0 0.091578 0.008291 11.045 < 2e-16 ***

#> a1 0.518341 0.069238 7.486 7.08e-14 ***

#> a2 0.134213 0.045741 2.934 0.00334 **

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Diagnostic Tests:

#> Jarque Bera Test

#>

#> data: Residuals

#> X-squared = 1.1825, df = 2, p-value = 0.5536

#>

#>

#> Box-Ljung test

#>

#> data: Squared.Residuals

#> X-squared = 0.3441, df = 1, p-value = 0.5575

#>

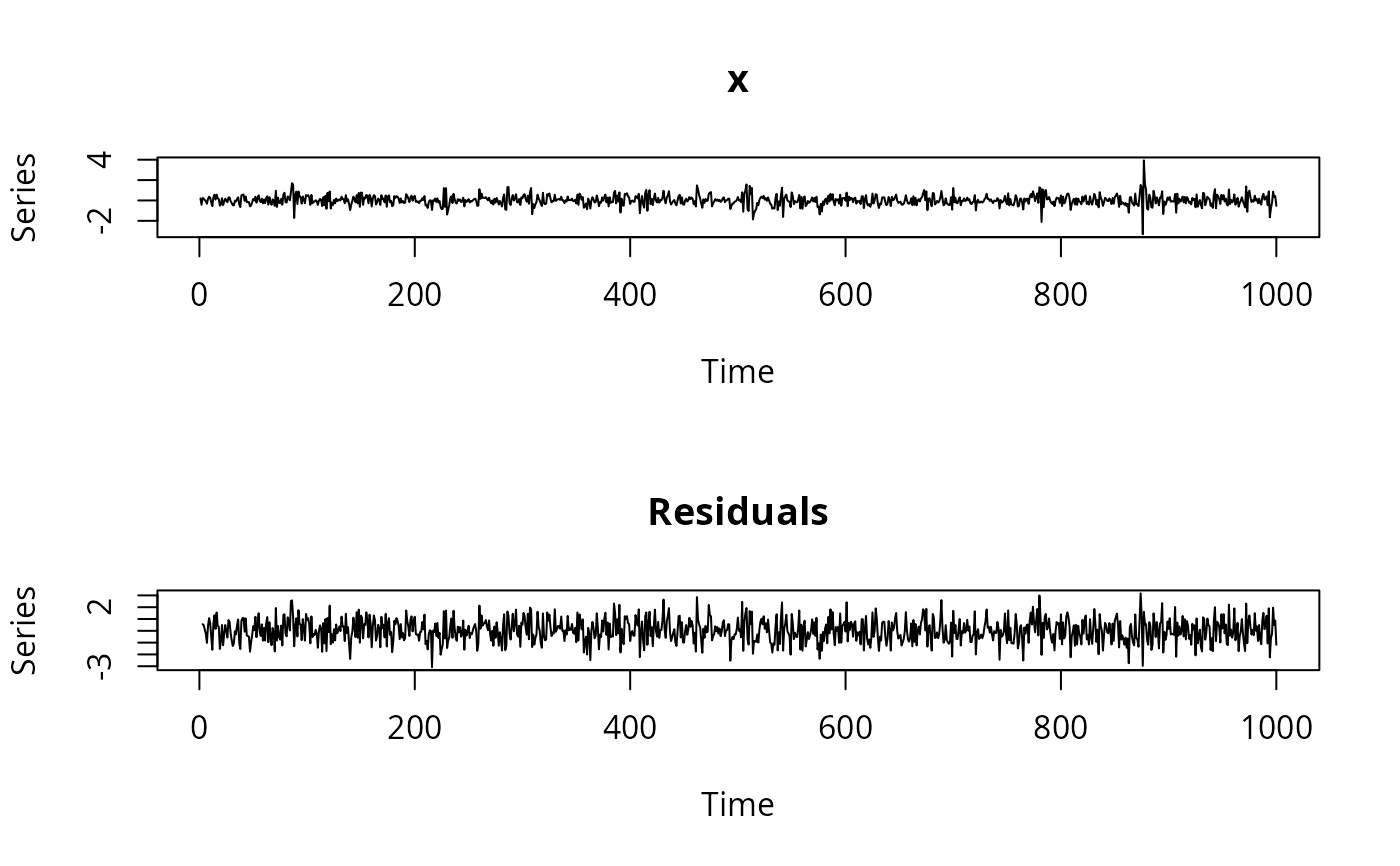

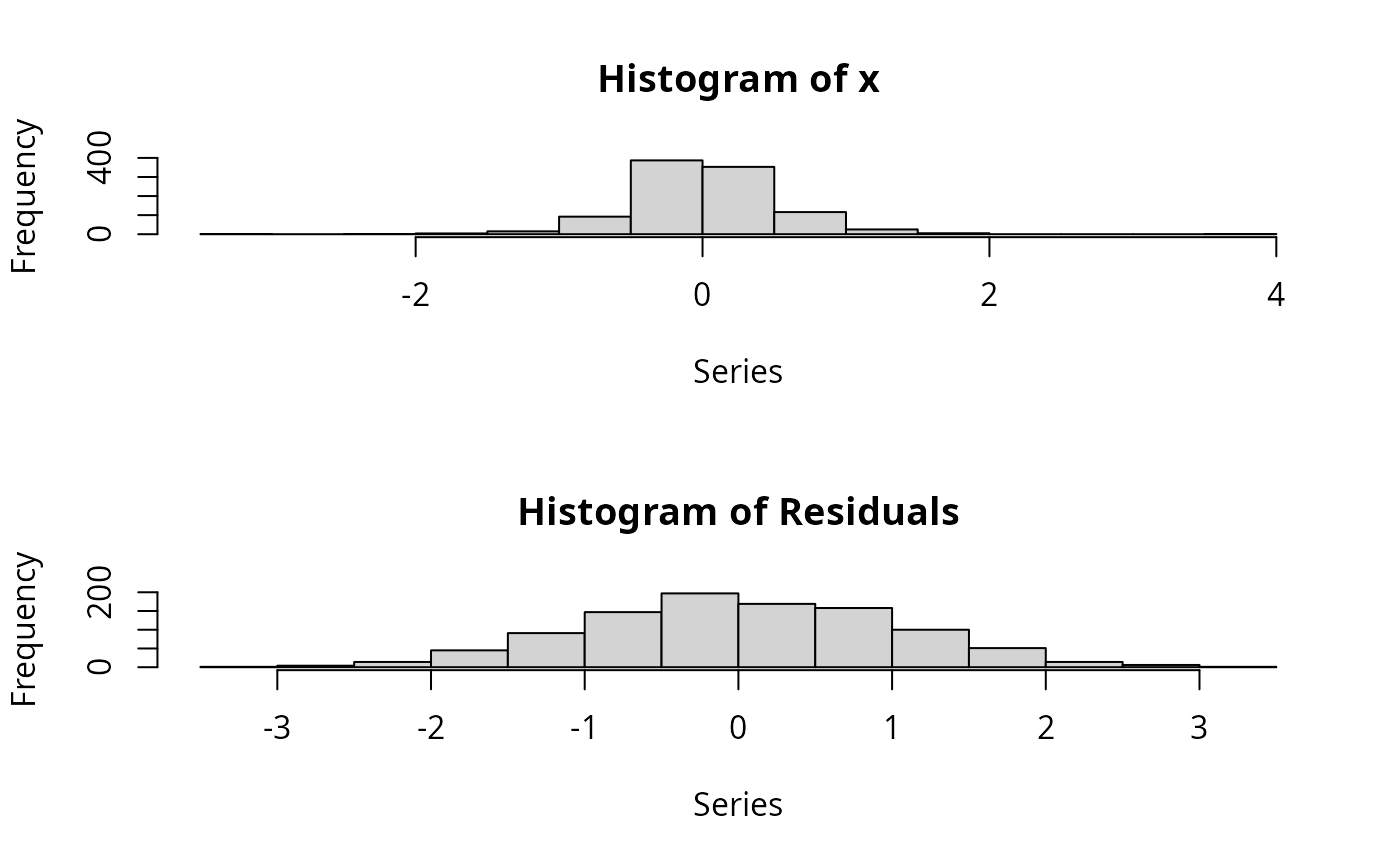

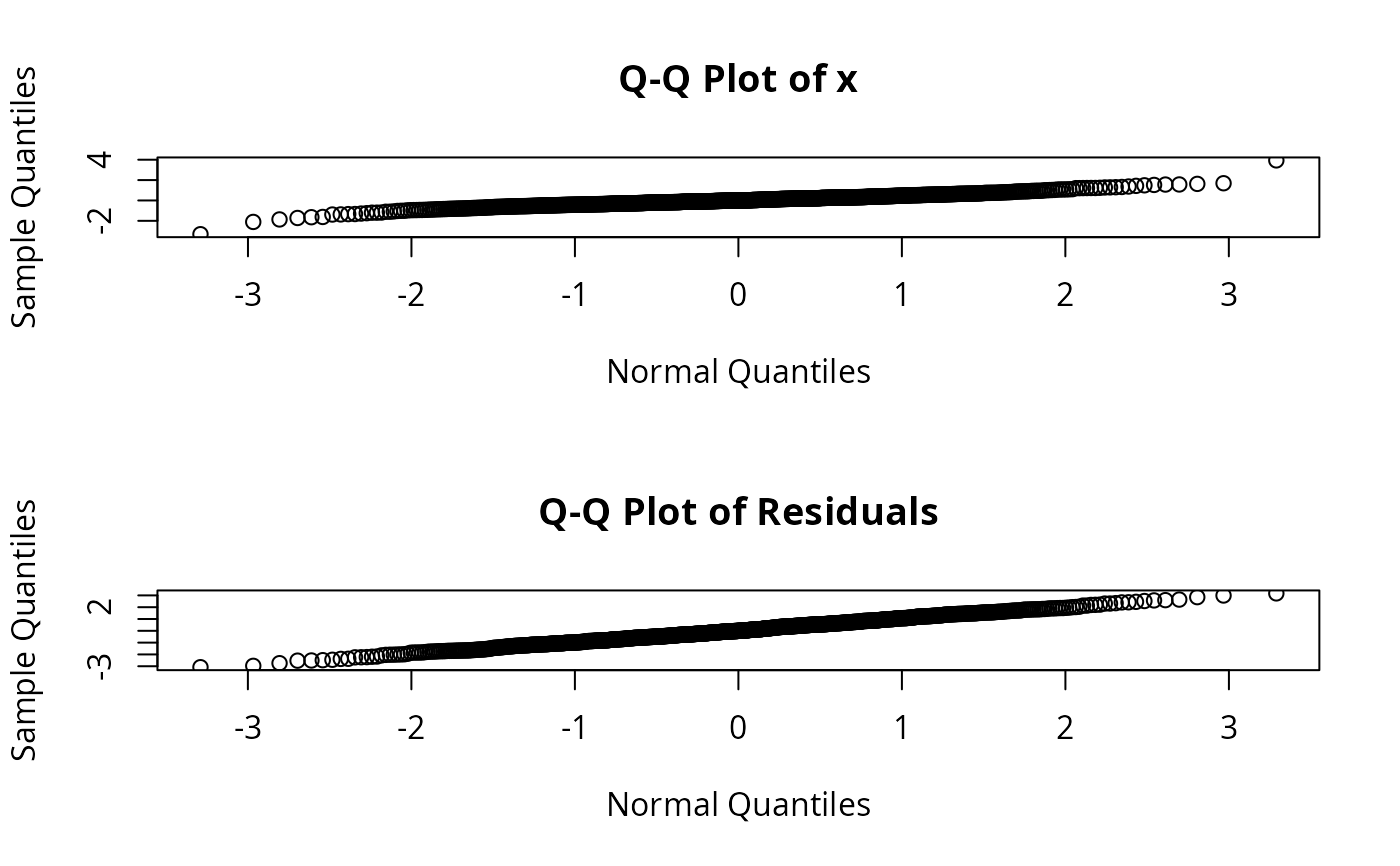

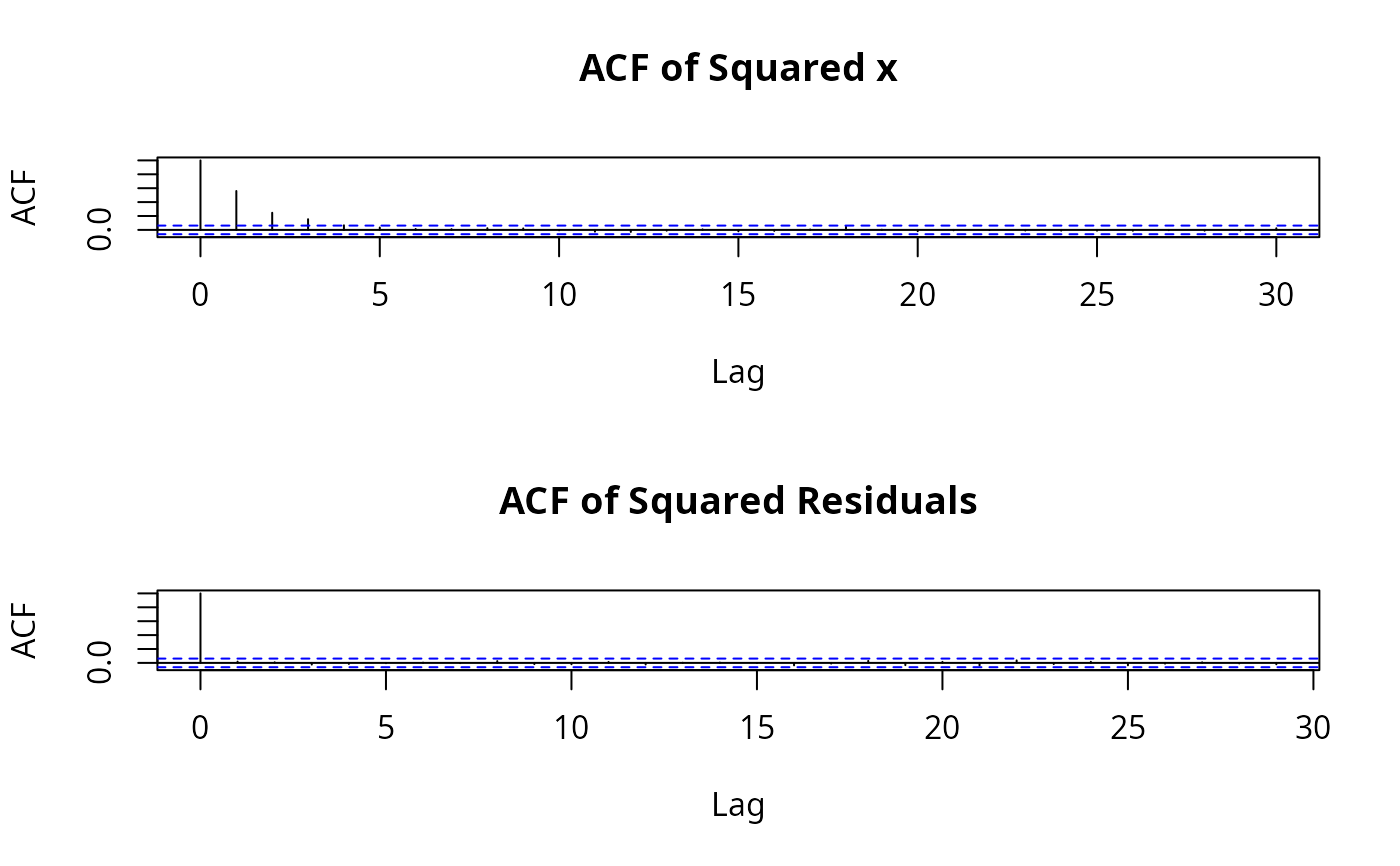

plot(x.arch)

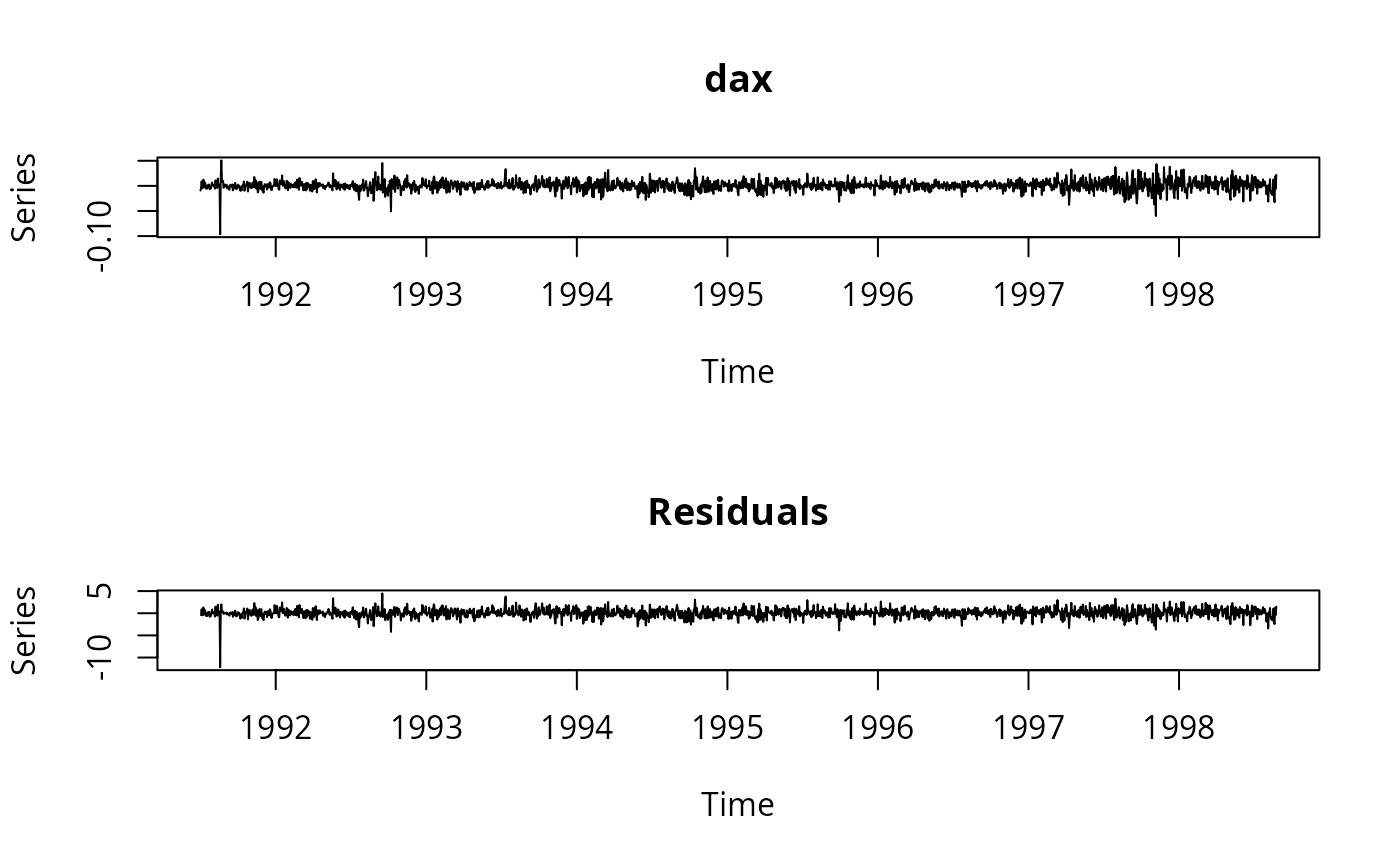

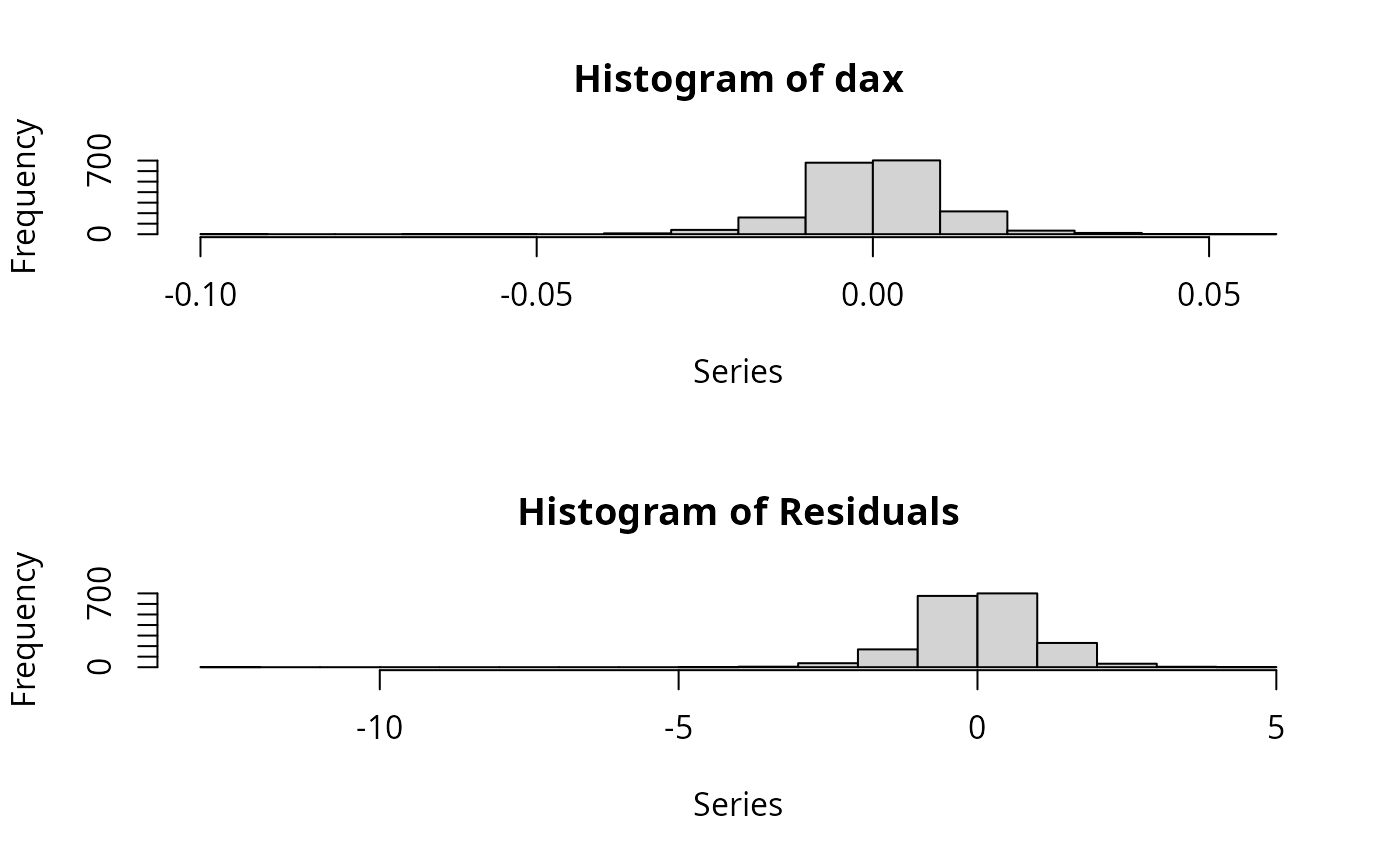

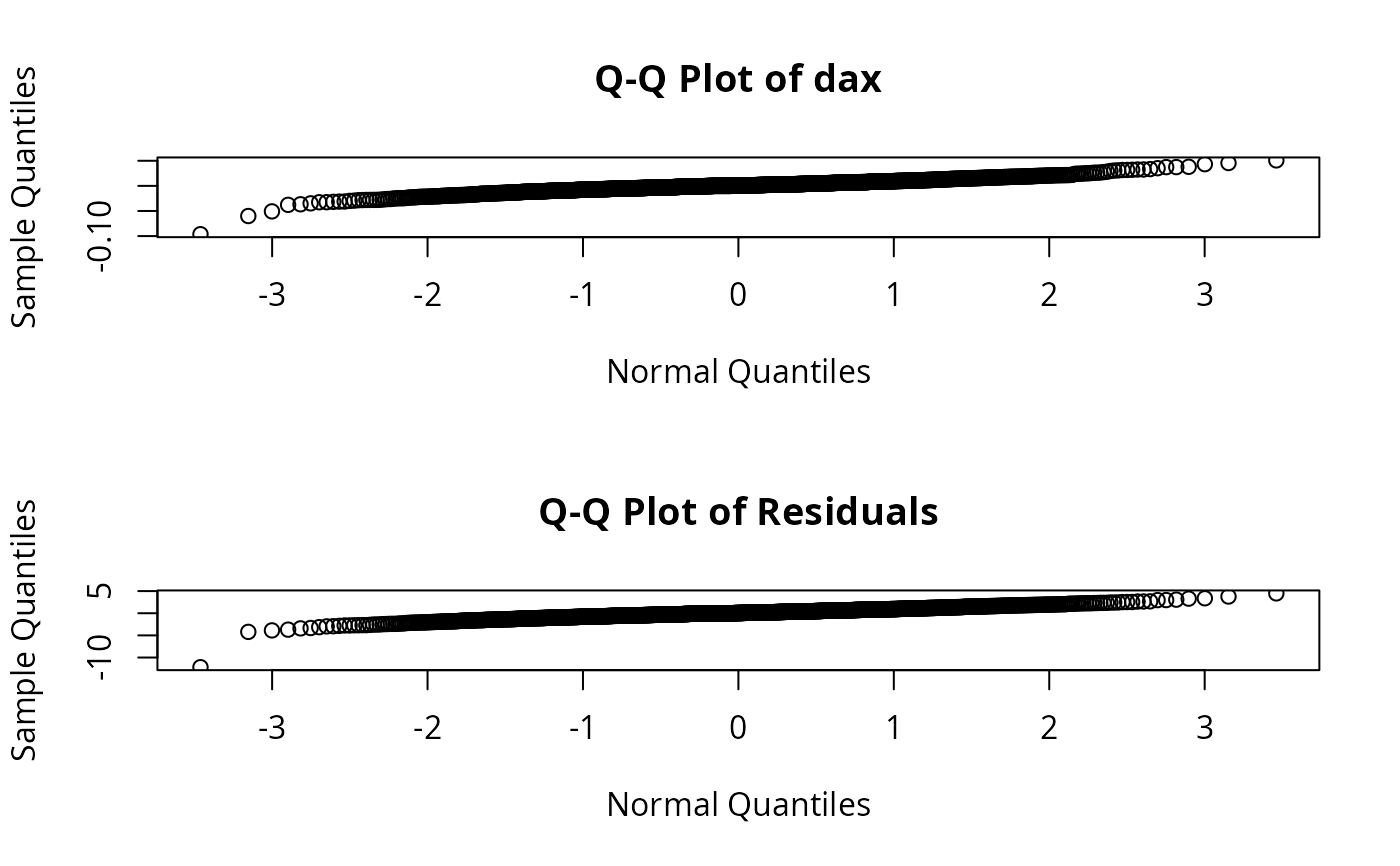

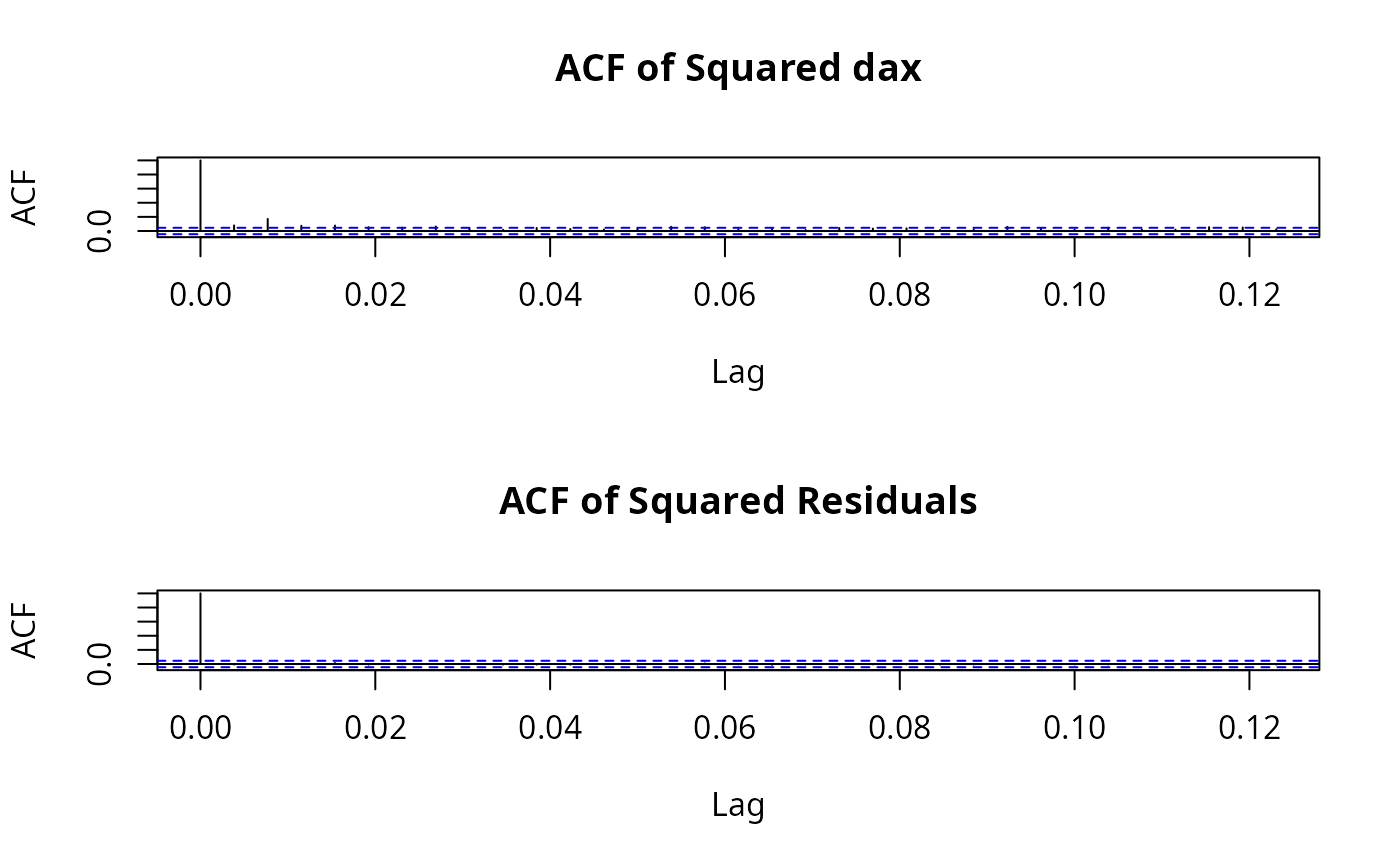

data(EuStockMarkets)

dax <- diff(log(EuStockMarkets))[,"DAX"]

dax.garch <- garch(dax) # Fit a GARCH(1,1) to DAX returns

#>

#> ***** ESTIMATION WITH ANALYTICAL GRADIENT *****

#>

#>

#> I INITIAL X(I) D(I)

#>

#> 1 9.549651e-05 1.000e+00

#> 2 5.000000e-02 1.000e+00

#> 3 5.000000e-02 1.000e+00

#>

#> IT NF F RELDF PRELDF RELDX STPPAR D*STEP NPRELDF

#> 0 1 -7.584e+03

#> 1 8 -7.585e+03 1.45e-05 2.60e-05 1.4e-05 1.0e+11 1.4e-06 1.35e+06

#> 2 9 -7.585e+03 1.88e-07 1.97e-07 1.3e-05 2.0e+00 1.4e-06 1.50e+00

#> 3 18 -7.589e+03 6.22e-04 1.10e-03 3.5e-01 2.0e+00 5.5e-02 1.50e+00

#> 4 21 -7.601e+03 1.58e-03 1.81e-03 6.2e-01 1.9e+00 2.2e-01 3.07e-01

#> 5 23 -7.634e+03 4.22e-03 3.55e-03 4.3e-01 9.6e-01 4.4e-01 3.06e-02

#> 6 25 -7.646e+03 1.61e-03 1.85e-03 2.9e-02 2.0e+00 4.4e-02 5.43e-02

#> 7 27 -7.646e+03 3.82e-05 5.23e-04 1.3e-02 2.0e+00 2.0e-02 1.46e-02

#> 8 28 -7.648e+03 1.86e-04 1.46e-04 6.5e-03 2.0e+00 9.9e-03 1.54e-03

#> 9 29 -7.648e+03 3.12e-05 4.83e-05 6.4e-03 2.0e+00 9.9e-03 3.34e-03

#> 10 30 -7.648e+03 1.39e-05 6.31e-05 6.2e-03 1.9e+00 9.9e-03 1.86e-03

#> 11 31 -7.650e+03 2.70e-04 3.24e-04 6.0e-03 1.9e+00 9.9e-03 4.99e-03

#> 12 34 -7.656e+03 8.42e-04 8.57e-04 2.2e-02 1.7e-01 3.9e-02 2.22e-03

#> 13 36 -7.661e+03 6.12e-04 6.40e-04 1.9e-02 4.2e-01 3.9e-02 2.09e-03

#> 14 38 -7.665e+03 4.87e-04 8.63e-04 4.9e-02 4.1e-01 9.6e-02 9.69e-04

#> 15 48 -7.666e+03 1.02e-04 1.86e-04 1.9e-07 4.5e+00 3.5e-07 3.94e-04

#> 16 49 -7.666e+03 1.12e-07 1.01e-07 1.9e-07 2.0e+00 3.5e-07 6.22e-05

#> 17 57 -7.666e+03 1.60e-05 2.70e-05 2.0e-03 9.3e-01 3.7e-03 6.10e-05

#> 18 59 -7.666e+03 5.23e-06 7.01e-06 3.7e-03 3.9e-01 8.0e-03 7.77e-06

#> 19 60 -7.666e+03 4.08e-08 3.74e-08 1.4e-04 0.0e+00 3.1e-04 3.74e-08

#> 20 61 -7.666e+03 2.31e-09 8.57e-10 8.6e-06 0.0e+00 2.0e-05 8.57e-10

#> 21 62 -7.666e+03 5.35e-11 2.25e-13 7.6e-07 0.0e+00 1.6e-06 2.25e-13

#> 22 63 -7.666e+03 1.81e-12 7.06e-16 1.7e-08 0.0e+00 3.4e-08 7.06e-16

#> 23 64 -7.666e+03 7.00e-14 1.69e-17 1.0e-09 0.0e+00 2.4e-09 1.69e-17

#> 24 65 -7.666e+03 -1.16e-14 1.76e-20 1.9e-10 0.0e+00 4.0e-10 1.76e-20

#>

#> ***** X- AND RELATIVE FUNCTION CONVERGENCE *****

#>

#> FUNCTION -7.665775e+03 RELDX 1.874e-10

#> FUNC. EVALS 65 GRAD. EVALS 24

#> PRELDF 1.760e-20 NPRELDF 1.760e-20

#>

#> I FINAL X(I) D(I) G(I)

#>

#> 1 4.639289e-06 1.000e+00 -2.337e-02

#> 2 6.832875e-02 1.000e+00 -8.294e-07

#> 3 8.890666e-01 1.000e+00 -2.230e-06

#>

summary(dax.garch) # ARCH effects are filtered. However,

#>

#> Call:

#> garch(x = dax)

#>

#> Model:

#> GARCH(1,1)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -12.18398 -0.47968 0.04949 0.65746 4.48048

#>

#> Coefficient(s):

#> Estimate Std. Error t value Pr(>|t|)

#> a0 4.639e-06 7.560e-07 6.137 8.42e-10 ***

#> a1 6.833e-02 1.125e-02 6.073 1.25e-09 ***

#> b1 8.891e-01 1.652e-02 53.817 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Diagnostic Tests:

#> Jarque Bera Test

#>

#> data: Residuals

#> X-squared = 12947, df = 2, p-value < 2.2e-16

#>

#>

#> Box-Ljung test

#>

#> data: Squared.Residuals

#> X-squared = 0.13566, df = 1, p-value = 0.7126

#>

plot(dax.garch) # conditional normality seems to be violated

data(EuStockMarkets)

dax <- diff(log(EuStockMarkets))[,"DAX"]

dax.garch <- garch(dax) # Fit a GARCH(1,1) to DAX returns

#>

#> ***** ESTIMATION WITH ANALYTICAL GRADIENT *****

#>

#>

#> I INITIAL X(I) D(I)

#>

#> 1 9.549651e-05 1.000e+00

#> 2 5.000000e-02 1.000e+00

#> 3 5.000000e-02 1.000e+00

#>

#> IT NF F RELDF PRELDF RELDX STPPAR D*STEP NPRELDF

#> 0 1 -7.584e+03

#> 1 8 -7.585e+03 1.45e-05 2.60e-05 1.4e-05 1.0e+11 1.4e-06 1.35e+06

#> 2 9 -7.585e+03 1.88e-07 1.97e-07 1.3e-05 2.0e+00 1.4e-06 1.50e+00

#> 3 18 -7.589e+03 6.22e-04 1.10e-03 3.5e-01 2.0e+00 5.5e-02 1.50e+00

#> 4 21 -7.601e+03 1.58e-03 1.81e-03 6.2e-01 1.9e+00 2.2e-01 3.07e-01

#> 5 23 -7.634e+03 4.22e-03 3.55e-03 4.3e-01 9.6e-01 4.4e-01 3.06e-02

#> 6 25 -7.646e+03 1.61e-03 1.85e-03 2.9e-02 2.0e+00 4.4e-02 5.43e-02

#> 7 27 -7.646e+03 3.82e-05 5.23e-04 1.3e-02 2.0e+00 2.0e-02 1.46e-02

#> 8 28 -7.648e+03 1.86e-04 1.46e-04 6.5e-03 2.0e+00 9.9e-03 1.54e-03

#> 9 29 -7.648e+03 3.12e-05 4.83e-05 6.4e-03 2.0e+00 9.9e-03 3.34e-03

#> 10 30 -7.648e+03 1.39e-05 6.31e-05 6.2e-03 1.9e+00 9.9e-03 1.86e-03

#> 11 31 -7.650e+03 2.70e-04 3.24e-04 6.0e-03 1.9e+00 9.9e-03 4.99e-03

#> 12 34 -7.656e+03 8.42e-04 8.57e-04 2.2e-02 1.7e-01 3.9e-02 2.22e-03

#> 13 36 -7.661e+03 6.12e-04 6.40e-04 1.9e-02 4.2e-01 3.9e-02 2.09e-03

#> 14 38 -7.665e+03 4.87e-04 8.63e-04 4.9e-02 4.1e-01 9.6e-02 9.69e-04

#> 15 48 -7.666e+03 1.02e-04 1.86e-04 1.9e-07 4.5e+00 3.5e-07 3.94e-04

#> 16 49 -7.666e+03 1.12e-07 1.01e-07 1.9e-07 2.0e+00 3.5e-07 6.22e-05

#> 17 57 -7.666e+03 1.60e-05 2.70e-05 2.0e-03 9.3e-01 3.7e-03 6.10e-05

#> 18 59 -7.666e+03 5.23e-06 7.01e-06 3.7e-03 3.9e-01 8.0e-03 7.77e-06

#> 19 60 -7.666e+03 4.08e-08 3.74e-08 1.4e-04 0.0e+00 3.1e-04 3.74e-08

#> 20 61 -7.666e+03 2.31e-09 8.57e-10 8.6e-06 0.0e+00 2.0e-05 8.57e-10

#> 21 62 -7.666e+03 5.35e-11 2.25e-13 7.6e-07 0.0e+00 1.6e-06 2.25e-13

#> 22 63 -7.666e+03 1.81e-12 7.06e-16 1.7e-08 0.0e+00 3.4e-08 7.06e-16

#> 23 64 -7.666e+03 7.00e-14 1.69e-17 1.0e-09 0.0e+00 2.4e-09 1.69e-17

#> 24 65 -7.666e+03 -1.16e-14 1.76e-20 1.9e-10 0.0e+00 4.0e-10 1.76e-20

#>

#> ***** X- AND RELATIVE FUNCTION CONVERGENCE *****

#>

#> FUNCTION -7.665775e+03 RELDX 1.874e-10

#> FUNC. EVALS 65 GRAD. EVALS 24

#> PRELDF 1.760e-20 NPRELDF 1.760e-20

#>

#> I FINAL X(I) D(I) G(I)

#>

#> 1 4.639289e-06 1.000e+00 -2.337e-02

#> 2 6.832875e-02 1.000e+00 -8.294e-07

#> 3 8.890666e-01 1.000e+00 -2.230e-06

#>

summary(dax.garch) # ARCH effects are filtered. However,

#>

#> Call:

#> garch(x = dax)

#>

#> Model:

#> GARCH(1,1)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -12.18398 -0.47968 0.04949 0.65746 4.48048

#>

#> Coefficient(s):

#> Estimate Std. Error t value Pr(>|t|)

#> a0 4.639e-06 7.560e-07 6.137 8.42e-10 ***

#> a1 6.833e-02 1.125e-02 6.073 1.25e-09 ***

#> b1 8.891e-01 1.652e-02 53.817 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Diagnostic Tests:

#> Jarque Bera Test

#>

#> data: Residuals

#> X-squared = 12947, df = 2, p-value < 2.2e-16

#>

#>

#> Box-Ljung test

#>

#> data: Squared.Residuals

#> X-squared = 0.13566, df = 1, p-value = 0.7126

#>

plot(dax.garch) # conditional normality seems to be violated