William's % R.

Value

A object of the same class as HLC or a vector (if

try.xts fails) containing the William's %R values.

Details

If an High-Low-Close series is provided, the indicator is calculated using the high/low values. If a vector is provided, the calculation only uses that series.

Note

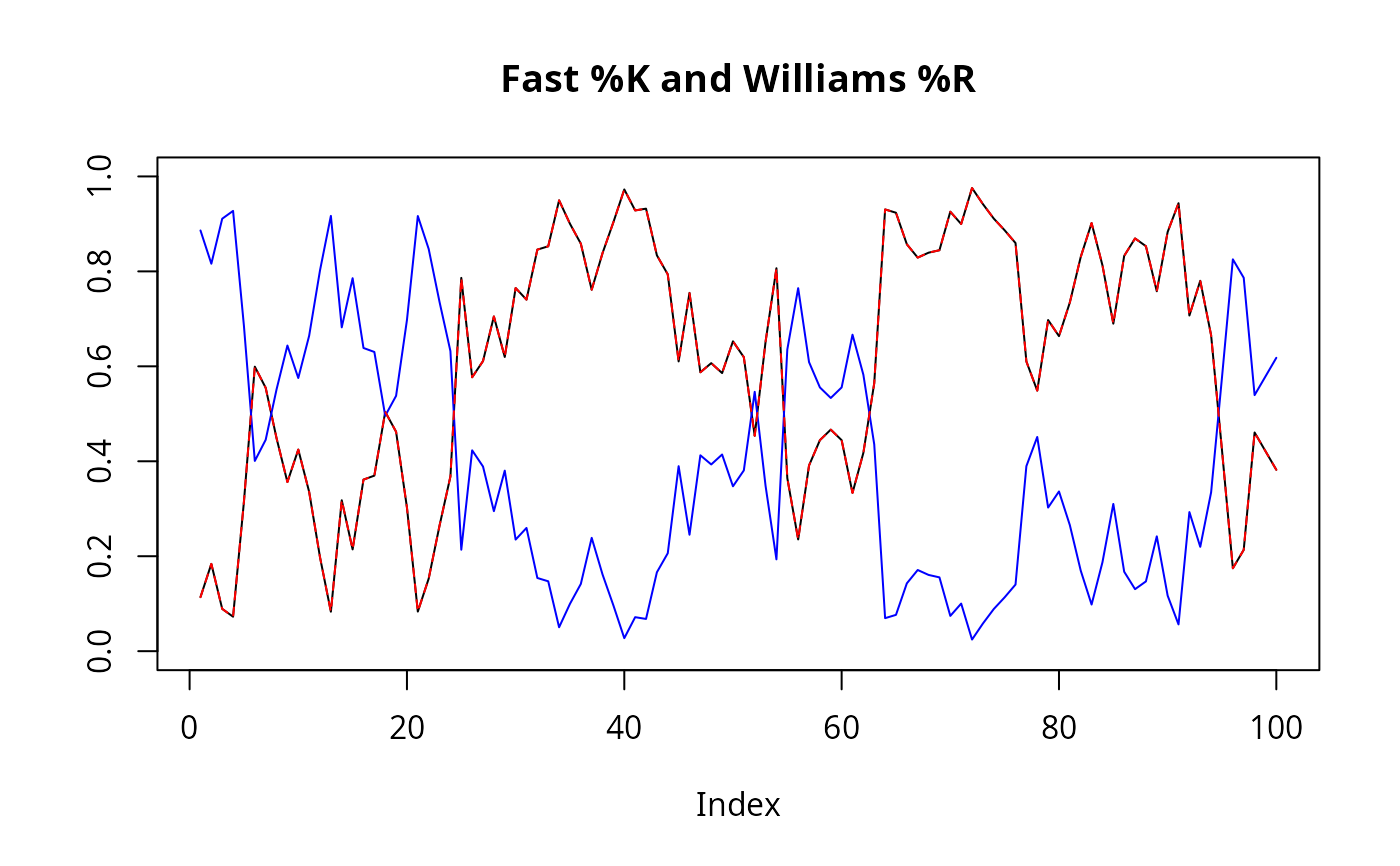

The William's %R calculation is similar to stochastics' fast %K.

The value for William's %R will be 0.5 whenever the highest high and

lowest low are the same over the last n periods.

References

The following site(s) were used to code/document this

indicator:

https://www.fmlabs.com/reference/WilliamsR.htm

https://www.metastock.com/Customer/Resources/TAAZ/?p=126

https://www.linnsoft.com/techind/williams-r-wpr

https://school.stockcharts.com/doku.php?id=technical_indicators:williams_r

See also

See stoch.

Examples

data(ttrc)

stochOsc <- stoch(ttrc[,c("High","Low","Close")])

stochWPR<- WPR(ttrc[,c("High","Low","Close")])

plot(tail(stochOsc[,"fastK"], 100), type="l",

main="Fast %K and Williams %R", ylab="",

ylim=range(cbind(stochOsc, stochWPR), na.rm=TRUE) )

lines(tail(stochWPR, 100), col="blue")

lines(tail(1-stochWPR, 100), col="red", lty="dashed")