Variability Summary: Statistics and Stylized Facts

Source:R/table.Variability.R

table.Variability.RdTable of Mean absolute difference, period standard deviation and annualised standard deviation

table.Variability(R, scale = NA, geometric = TRUE, digits = 4)Arguments

- R

an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns

- scale

number of periods in a year (daily scale = 252, monthly scale = 12, quarterly scale = 4)

- geometric

utilize geometric chaining (TRUE) or simple/arithmetic chaining (FALSE) to aggregate returns, default TRUE

- digits

number of digits to round results to

References

Carl Bacon, Practical portfolio performance measurement and attribution, second edition 2008 p.65

See also

Examples

data(managers)

table.Variability(managers[,1:8])

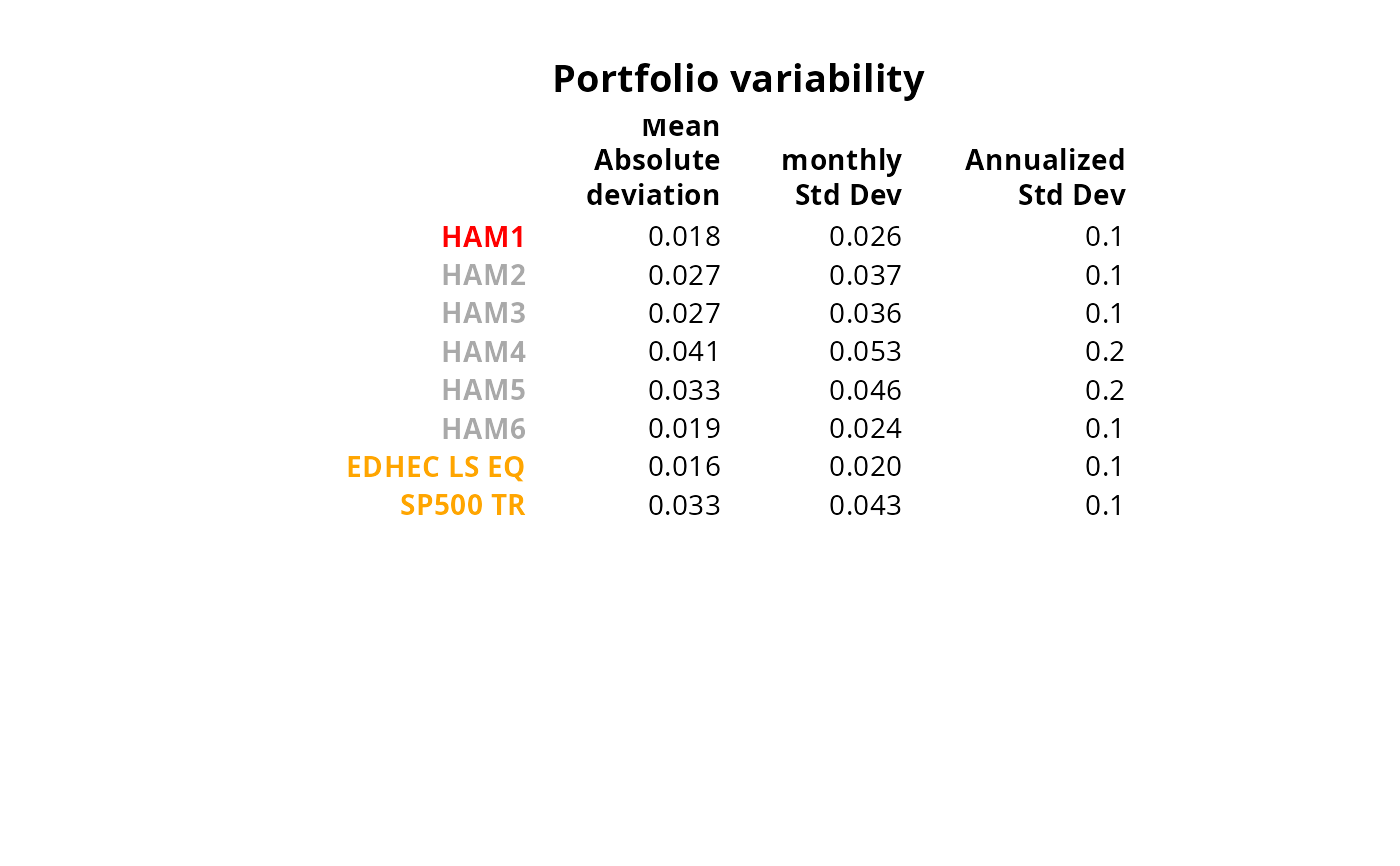

#> HAM1 HAM2 HAM3 HAM4 HAM5 HAM6 EDHEC LS EQ

#> Mean Absolute deviation 0.0182 0.0268 0.0268 0.0410 0.0329 0.0187 0.0159

#> monthly Std Dev 0.0256 0.0367 0.0365 0.0532 0.0457 0.0238 0.0205

#> Annualized Std Dev 0.0888 0.1272 0.1265 0.1843 0.1584 0.0825 0.0708

#> SP500 TR

#> Mean Absolute deviation 0.0333

#> monthly Std Dev 0.0433

#> Annualized Std Dev 0.1500

# don't test on CRAN, since it requires Suggested packages

require("Hmisc")

result = t(table.Variability(managers[,1:8]))

textplot(format.df(result, na.blank=TRUE, numeric.dollar=FALSE, cdec=c(3,3,1)),

rmar = 0.8, cmar = 2, max.cex=.9, halign = "center", valign = "top",

row.valign="center", wrap.rownames=20, wrap.colnames=10,

col.rownames=c("red", rep("darkgray",5), rep("orange",2)), mar = c(0,0,3,0)+0.1)

title(main="Portfolio variability")