Rolling Periods Summary: Statistics and Stylized Facts

Source:R/table.RollingPeriods.R

table.RollingPeriods.RdA table of estimates of rolling period return measures

table.RollingPeriods(

R,

periods = subset(c(12, 36, 60), c(12, 36, 60) < length(as.matrix(R[, 1]))),

FUNCS = c("mean", "sd"),

funcs.names = c("Average", "Std Dev"),

digits = 4,

...

)

table.TrailingPeriodsRel(

R,

Rb,

periods = subset(c(12, 36, 60), c(12, 36, 60) < length(as.matrix(R[, 1]))),

FUNCS = c("cor", "CAPM.beta"),

funcs.names = c("Correlation", "Beta"),

digits = 4,

...

)Arguments

- R

an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns

- periods

number of periods to use as rolling window(s), subset of

c(3, 6, 9, 12, 18, 24, 36, 48)- FUNCS

list of functions to apply the rolling period to

- funcs.names

vector of function names used for labeling table rows

- digits

number of digits to round results to

- ...

any other passthru parameters for functions specified in FUNCS

- Rb

an xts, vector, matrix, data frame, timeSeries or zoo object of index, benchmark, portfolio, or secondary asset returns to compare against

See also

Examples

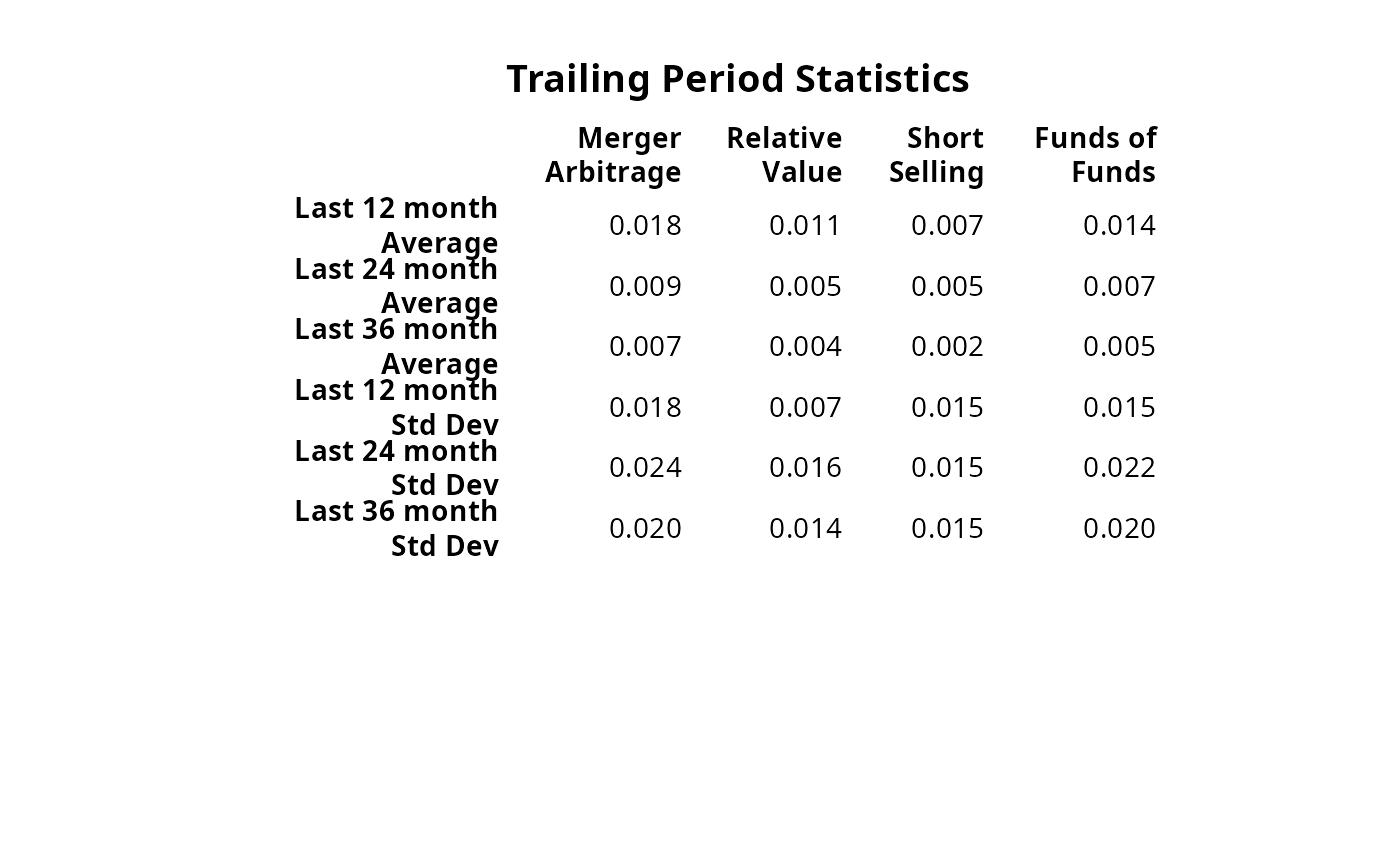

data(edhec)

table.TrailingPeriods(edhec[,10:13], periods=c(12,24,36))

#> Merger Arbitrage Relative Value Short Selling

#> Last 12 month Average 0.0175 0.0110 0.0074

#> Last 24 month Average 0.0085 0.0055 0.0055

#> Last 36 month Average 0.0069 0.0039 0.0016

#> Last 12 month Std Dev 0.0181 0.0066 0.0154

#> Last 24 month Std Dev 0.0245 0.0164 0.0147

#> Last 36 month Std Dev 0.0203 0.0141 0.0154

#> Funds of Funds

#> Last 12 month Average 0.0142

#> Last 24 month Average 0.0074

#> Last 36 month Average 0.0046

#> Last 12 month Std Dev 0.0150

#> Last 24 month Std Dev 0.0217

#> Last 36 month Std Dev 0.0195

result=table.TrailingPeriods(edhec[,10:13], periods=c(12,24,36))

# don't test on CRAN, since it requires Suggested packages

require("Hmisc")

textplot(format.df(result, na.blank=TRUE, numeric.dollar=FALSE,

cdec=rep(3,dim(result)[2])), rmar = 0.8, cmar = 1.5,

max.cex=.9, halign = "center", valign = "top", row.valign="center",

wrap.rownames=15, wrap.colnames=10, mar = c(0,0,3,0)+0.1)

title(main="Trailing Period Statistics")