Returns Summary: Statistics and Stylized Facts

Source:R/table.MonthlyReturns.R

table.MonthlyReturns.RdReturns a basic set of statistics that match the period of the data passed in (e.g., monthly returns will get monthly statistics, daily will be daily stats, and so on)

table.Stats(R, ci = 0.95, digits = 4)Arguments

Details

This was created as a way to display a set of related statistics together for comparison across a set of instruments or funds. Careful consideration to missing data or unequal time series should be given when intepreting the results.

Examples

data(edhec)

table.Stats(edhec[,1:3])

#> Convertible Arbitrage CTA Global Distressed Securities

#> Observations 293.0000 293.0000 293.0000

#> NAs 0.0000 0.0000 0.0000

#> Minimum -0.1237 -0.0568 -0.1061

#> Quartile 1 0.0002 -0.0114 -0.0021

#> Median 0.0065 0.0020 0.0088

#> Arithmetic Mean 0.0058 0.0043 0.0068

#> Geometric Mean 0.0056 0.0041 0.0067

#> Quartile 3 0.0137 0.0199 0.0179

#> Maximum 0.0611 0.0691 0.0504

#> SE Mean 0.0010 0.0013 0.0011

#> LCL Mean (0.95) 0.0039 0.0017 0.0047

#> UCL Mean (0.95) 0.0077 0.0069 0.0089

#> Variance 0.0003 0.0005 0.0003

#> Stdev 0.0168 0.0228 0.0181

#> Skewness -2.5970 0.1628 -1.7283

#> Kurtosis 18.6011 -0.0076 7.7946

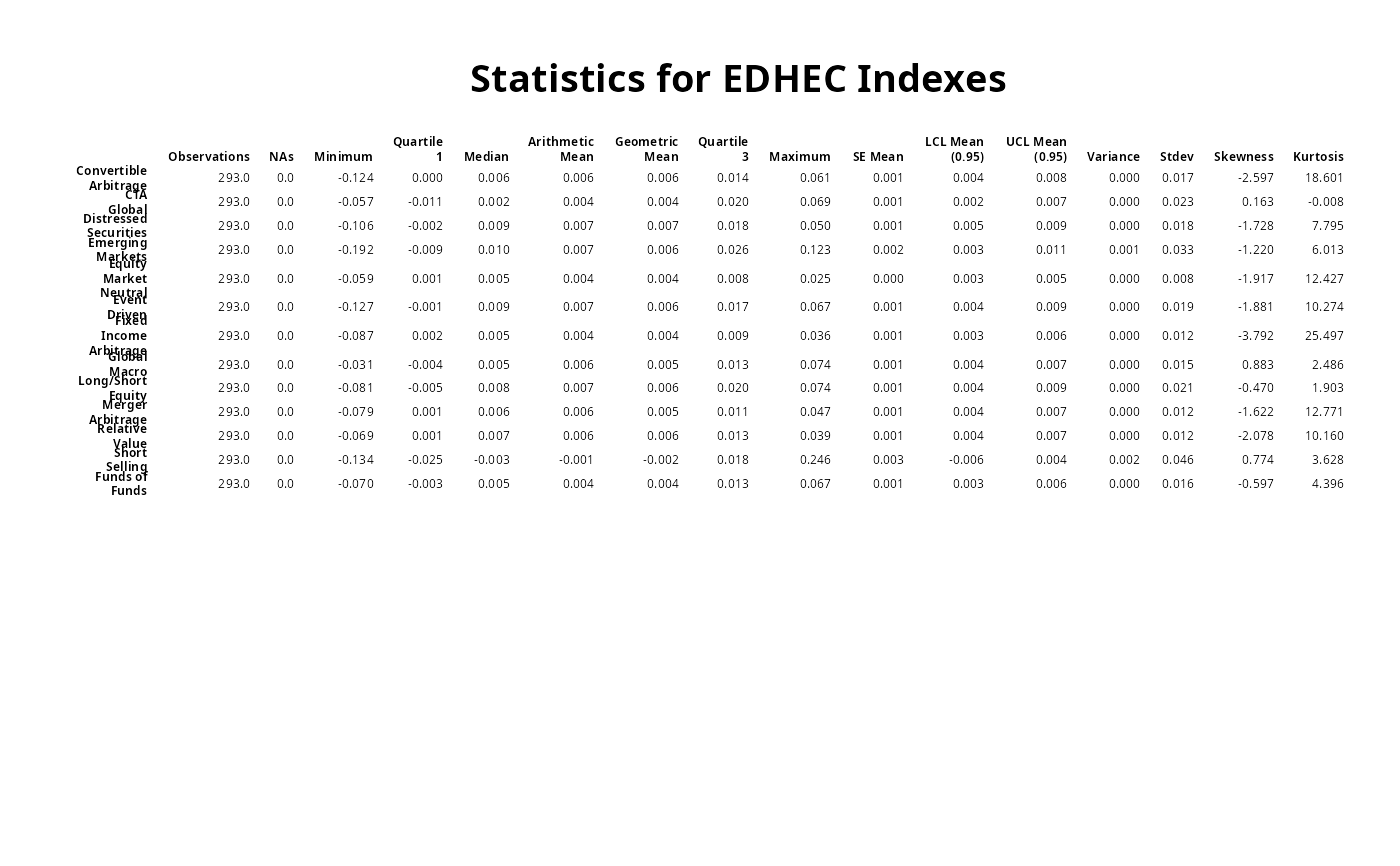

t(table.Stats(edhec))

#> Observations NAs Minimum Quartile 1 Median

#> Convertible Arbitrage 293 0 -0.1237 0.0002 0.0065

#> CTA Global 293 0 -0.0568 -0.0114 0.0020

#> Distressed Securities 293 0 -0.1061 -0.0021 0.0088

#> Emerging Markets 293 0 -0.1922 -0.0092 0.0100

#> Equity Market Neutral 293 0 -0.0587 0.0009 0.0047

#> Event Driven 293 0 -0.1269 -0.0012 0.0088

#> Fixed Income Arbitrage 293 0 -0.0867 0.0018 0.0055

#> Global Macro 293 0 -0.0313 -0.0039 0.0047

#> Long/Short Equity 293 0 -0.0813 -0.0047 0.0082

#> Merger Arbitrage 293 0 -0.0790 0.0007 0.0059

#> Relative Value 293 0 -0.0692 0.0011 0.0067

#> Short Selling 293 0 -0.1340 -0.0251 -0.0032

#> Funds of Funds 293 0 -0.0705 -0.0033 0.0052

#> Arithmetic Mean Geometric Mean Quartile 3 Maximum

#> Convertible Arbitrage 0.0058 0.0056 0.0137 0.0611

#> CTA Global 0.0043 0.0041 0.0199 0.0691

#> Distressed Securities 0.0068 0.0067 0.0179 0.0504

#> Emerging Markets 0.0067 0.0062 0.0257 0.1230

#> Equity Market Neutral 0.0043 0.0043 0.0083 0.0253

#> Event Driven 0.0067 0.0065 0.0168 0.0666

#> Fixed Income Arbitrage 0.0044 0.0044 0.0093 0.0365

#> Global Macro 0.0056 0.0055 0.0128 0.0738

#> Long/Short Equity 0.0067 0.0065 0.0195 0.0745

#> Merger Arbitrage 0.0056 0.0055 0.0111 0.0472

#> Relative Value 0.0057 0.0057 0.0130 0.0392

#> Short Selling -0.0013 -0.0023 0.0181 0.2463

#> Funds of Funds 0.0045 0.0044 0.0127 0.0666

#> SE Mean LCL Mean (0.95) UCL Mean (0.95) Variance Stdev

#> Convertible Arbitrage 0.0010 0.0039 0.0077 0.0003 0.0168

#> CTA Global 0.0013 0.0017 0.0069 0.0005 0.0228

#> Distressed Securities 0.0011 0.0047 0.0089 0.0003 0.0181

#> Emerging Markets 0.0019 0.0030 0.0105 0.0011 0.0327

#> Equity Market Neutral 0.0005 0.0034 0.0053 0.0001 0.0082

#> Event Driven 0.0011 0.0045 0.0089 0.0004 0.0191

#> Fixed Income Arbitrage 0.0007 0.0031 0.0057 0.0001 0.0115

#> Global Macro 0.0009 0.0039 0.0073 0.0002 0.0146

#> Long/Short Equity 0.0012 0.0043 0.0091 0.0004 0.0209

#> Merger Arbitrage 0.0007 0.0043 0.0069 0.0001 0.0115

#> Relative Value 0.0007 0.0044 0.0071 0.0001 0.0119

#> Short Selling 0.0027 -0.0065 0.0040 0.0021 0.0455

#> Funds of Funds 0.0009 0.0027 0.0064 0.0003 0.0161

#> Skewness Kurtosis

#> Convertible Arbitrage -2.5970 18.6011

#> CTA Global 0.1628 -0.0076

#> Distressed Securities -1.7283 7.7946

#> Emerging Markets -1.2205 6.0126

#> Equity Market Neutral -1.9173 12.4266

#> Event Driven -1.8806 10.2736

#> Fixed Income Arbitrage -3.7918 25.4966

#> Global Macro 0.8826 2.4863

#> Long/Short Equity -0.4702 1.9028

#> Merger Arbitrage -1.6216 12.7706

#> Relative Value -2.0781 10.1597

#> Short Selling 0.7737 3.6282

#> Funds of Funds -0.5969 4.3957

result=t(table.Stats(edhec))

# don't test on CRAN, since it requires Suggested packages

require("Hmisc")

textplot(format.df(result, na.blank=TRUE, numeric.dollar=FALSE, cdec=c(rep(1,2),rep(3,14))),

rmar = 0.8, cmar = 1.5, max.cex=.9, halign = "center", valign = "top",

row.valign="center", wrap.rownames=10, wrap.colnames=10, mar = c(0,0,3,0)+0.1)

title(main="Statistics for EDHEC Indexes")