Information ratio Summary: Statistics and Stylized Facts

Source:R/table.InformationRatio.R

table.InformationRatio.RdTable of Tracking error, Annualised tracking error and Information ratio

table.InformationRatio(R, Rb, scale = NA, digits = 4)Arguments

References

Carl Bacon, Practical portfolio performance measurement and attribution, second edition 2008 p.81

See also

Examples

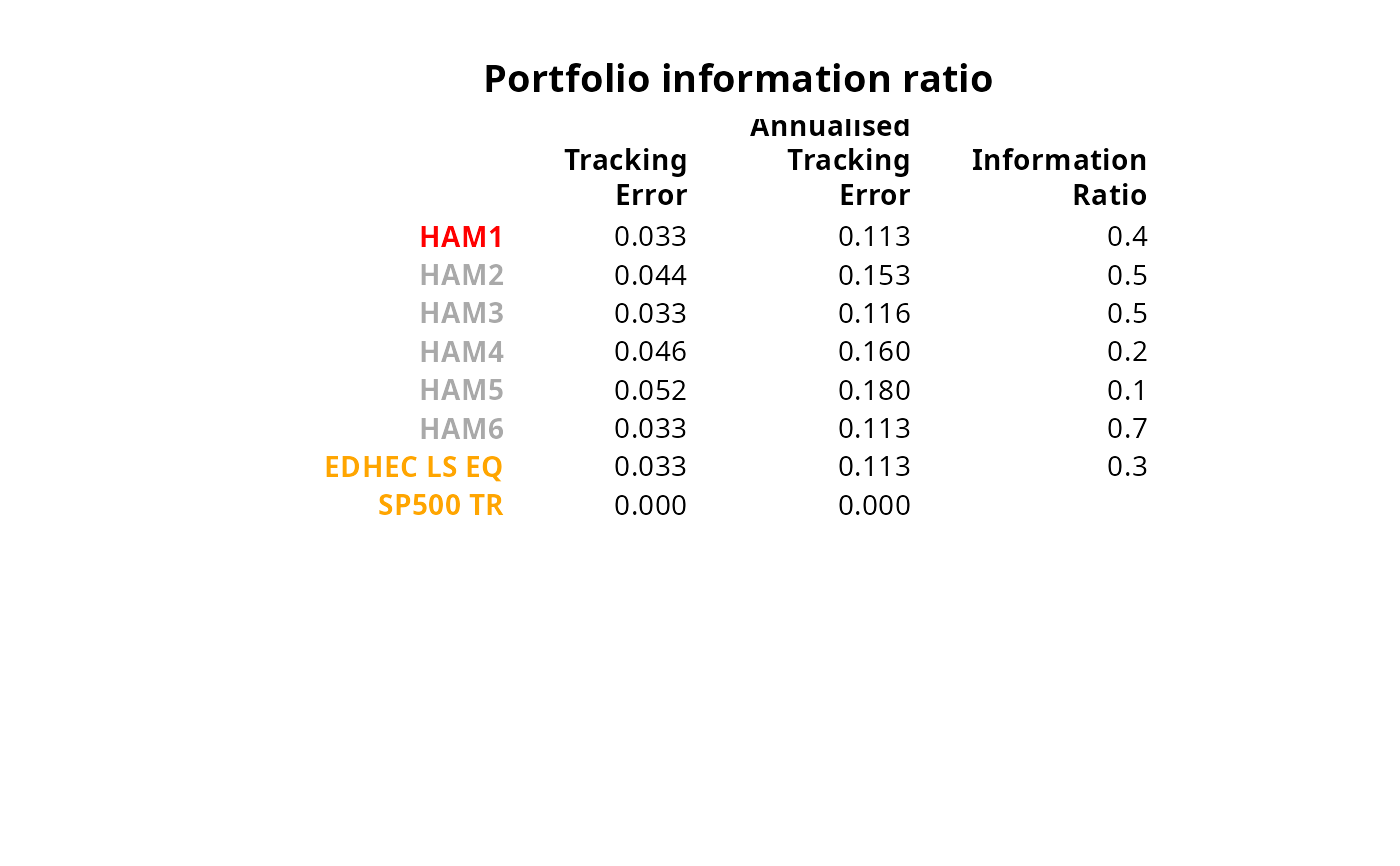

data(managers)

table.InformationRatio(managers[,1:8], managers[,8])

#> HAM1 HAM2 HAM3 HAM4 HAM5 HAM6 EDHEC LS EQ

#> Tracking Error 0.0327 0.0443 0.0334 0.0461 0.0520 0.0326 0.0326

#> Annualised Tracking Error 0.1132 0.1534 0.1159 0.1597 0.1800 0.1128 0.1130

#> Information Ratio 0.3604 0.5060 0.4701 0.1549 0.1212 0.6723 0.2985

#> SP500 TR

#> Tracking Error 0

#> Annualised Tracking Error 0

#> Information Ratio NaN

# don't test on CRAN, since it requires Suggested packages

require("Hmisc")

result = t(table.InformationRatio(managers[,1:8], managers[,8]))

textplot(format.df(result, na.blank=TRUE, numeric.dollar=FALSE, cdec=c(3,3,1)),

rmar = 0.8, cmar = 2, max.cex=.9, halign = "center", valign = "top",

row.valign="center", wrap.rownames=20, wrap.colnames=10,

col.rownames=c("red", rep("darkgray",5), rep("orange",2)), mar = c(0,0,3,0)+0.1)

title(main="Portfolio information ratio")