Higher Moments Summary: Statistics and Stylized Facts

Source:R/table.HigherMoments.R

table.HigherMoments.RdSummary of the higher moements and Co-Moments of the return distribution. Used to determine diversification potential. Also called "systematic" moments by several papers.

table.HigherMoments(Ra, Rb, scale = NA, Rf = 0, digits = 4, method = "moment")Arguments

- Ra

an xts, vector, matrix, data frame, timeSeries or zoo object of asset returns

- Rb

return vector of the benchmark asset

- scale

number of periods in a year (daily scale = 252, monthly scale = 12, quarterly scale = 4)

- Rf

risk free rate, in same period as your returns

- digits

number of digits to round results to

- method

method to use when computing

kurtosisone of:excess,moment,fisher

References

Martellini L., Vaissie M., Ziemann V. Investing in Hedge Funds: Adding Value through Active Style Allocation Decisions. October 2005. Edhec Risk and Asset Management Research Centre.

Examples

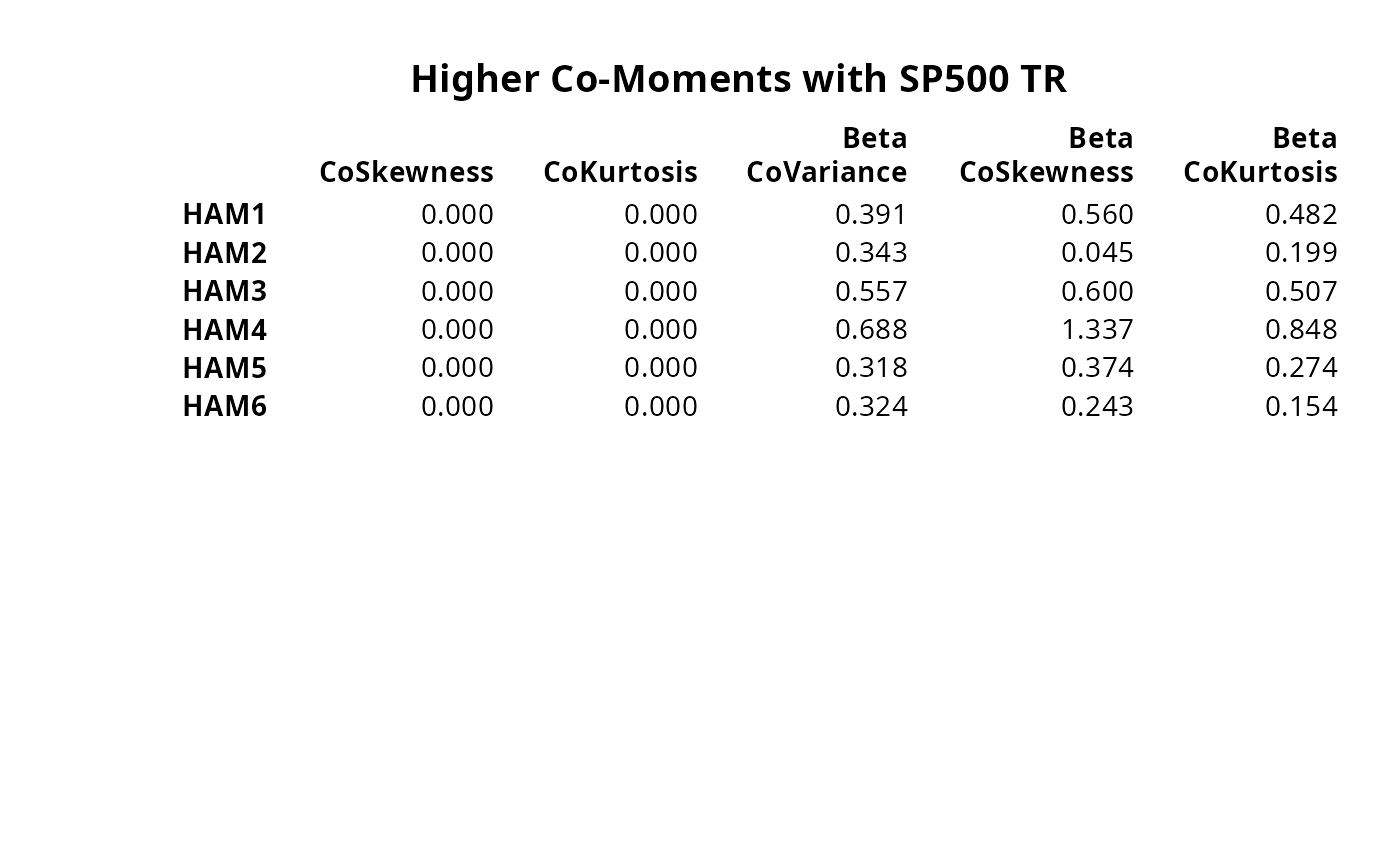

data(managers)

table.HigherMoments(managers[,1:3],managers[,8,drop=FALSE])

#> HAM1 to SP500 TR HAM2 to SP500 TR HAM3 to SP500 TR

#> CoSkewness 0.0000 0.0000 0.0000

#> CoKurtosis 0.0000 0.0000 0.0000

#> Beta CoVariance 0.3906 0.3432 0.5572

#> Beta CoSkewness 0.5602 0.0454 0.5999

#> Beta CoKurtosis 0.4815 0.1988 0.5068

result=t(table.HigherMoments(managers[,1:6],managers[,8,drop=FALSE]))

rownames(result)=colnames(managers[,1:6])

# don't test on CRAN, since it requires Suggested packages

require("Hmisc")

textplot(format.df(result, na.blank=TRUE, numeric.dollar=FALSE,

cdec=rep(3,dim(result)[2])), rmar = 0.8, cmar = 1.5,

max.cex=.9, halign = "center", valign = "top", row.valign="center",

wrap.rownames=5, wrap.colnames=10, mar = c(0,0,3,0)+0.1)

title(main="Higher Co-Moments with SP500 TR")