table for calculating the first six autocorrelation coefficients and significance

Source:R/table.Autocorrelation.R

table.Autocorrelation.RdProduces data table of autocorrelation coefficients \(\rho\) and corresponding Q(6)-statistic for each column in R.

table.Autocorrelation(R, digits = 4, max.lag = 6)Arguments

Note

To test returns for autocorrelation, Lo (2001) suggests the use of the

Ljung-Box test, a significance test for the auto-correlation coefficients.

Ljung and Box (1978) provide a refinement of the Q-statistic proposed by Box

and Pierce (1970) that offers a better fit for the \(\chi^2\) test

for small sample sizes. Box.test provides both.

References

Lo, Andrew W. 2001. Risk Management for Hedge Funds: Introduction and Overview. SSRN eLibrary.

Examples

# CRAN does not allow examples to load suggested packages in one of its tests

data(managers)

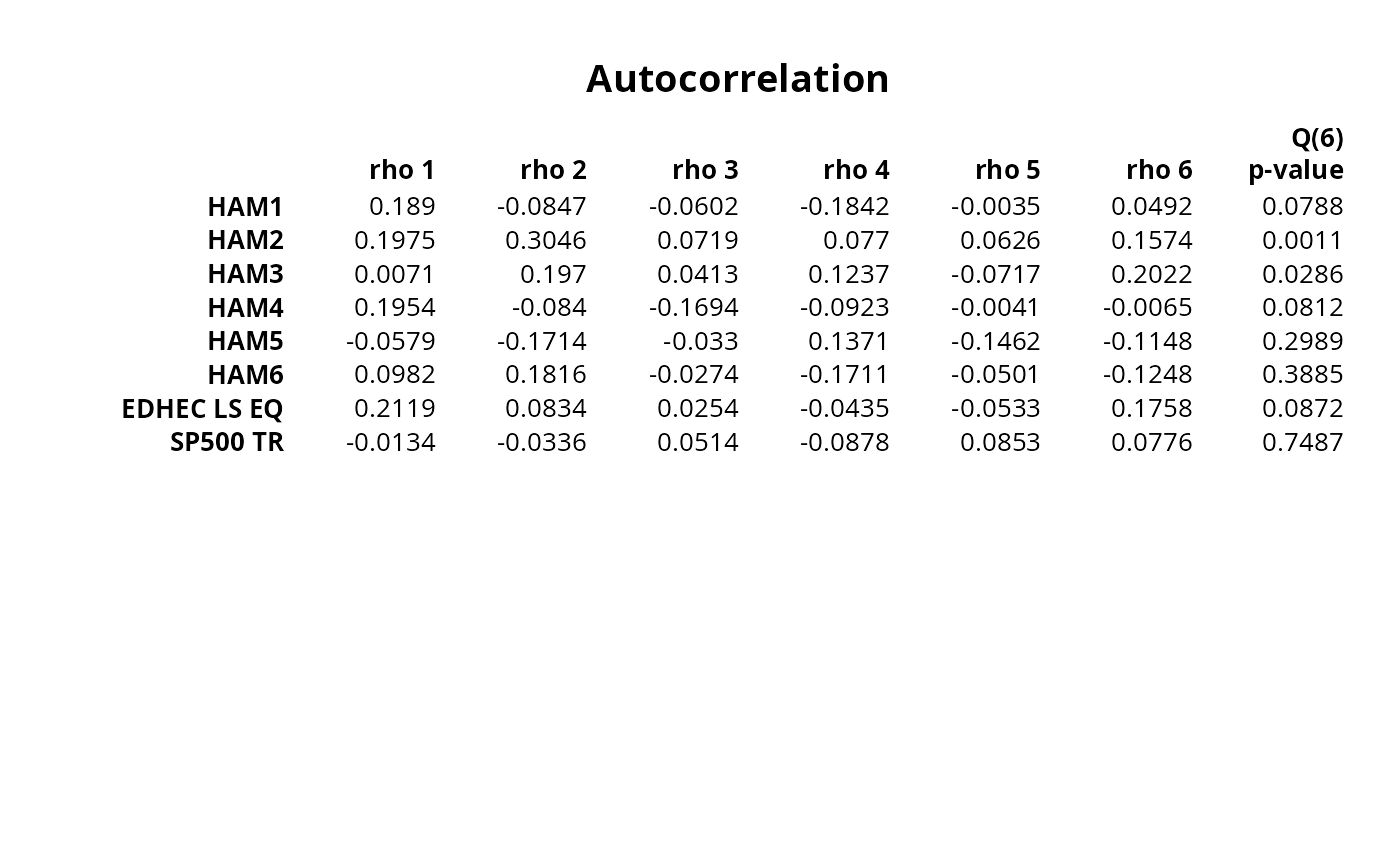

t(table.Autocorrelation(managers))

#> rho 1 rho 2 rho 3 rho 4 rho 5 rho 6 Q(6) p-value

#> HAM1 0.1890 -0.0847 -0.0602 -0.1842 -0.0035 0.0492 0.0788

#> HAM2 0.1975 0.3046 0.0719 0.0770 0.0626 0.1574 0.0011

#> HAM3 0.0071 0.1970 0.0413 0.1237 -0.0717 0.2022 0.0286

#> HAM4 0.1954 -0.0840 -0.1694 -0.0923 -0.0041 -0.0065 0.0812

#> HAM5 -0.0579 -0.1714 -0.0330 0.1371 -0.1462 -0.1148 0.2989

#> HAM6 0.0982 0.1816 -0.0274 -0.1711 -0.0501 -0.1248 0.3885

#> EDHEC LS EQ 0.2119 0.0834 0.0254 -0.0435 -0.0533 0.1758 0.0872

#> SP500 TR -0.0134 -0.0336 0.0514 -0.0878 0.0853 0.0776 0.7487

#> US 10Y TR 0.0398 -0.1739 0.1049 -0.0355 -0.1116 -0.0602 0.2199

#> US 3m TR 0.9224 0.9081 0.8968 0.8746 0.8363 0.8127 0.0000

result = t(table.Autocorrelation(managers[,1:8]))

textplot(result, rmar = 0.8, cmar = 2, max.cex=.9, halign = "center",

valign = "top", row.valign="center", wrap.rownames=15,

wrap.colnames=10, mar = c(0,0,3,0)+0.1)

title(main="Autocorrelation")