Functions for calculating the nearest comoment estimator for financial time series

Source:R/MM.NCE.R

NCE.Rdcalculates NCE covariance, coskewness and cokurtosis matrices

MM.NCE(R, as.mat = TRUE, ...)Arguments

Details

The coskewness and cokurtosis matrices are defined as the matrices of dimension p x p^2 and p x p^3 containing the third and fourth order central moments. They are useful for measuring nonlinear dependence between different assets of the portfolio and computing modified VaR and modified ES of a portfolio.

The nearest comoment estimator is a way to estimate the covariance, coskewness and cokurtosis matrix by means of a latent multi-factor model. The method is proposed in Boudt, Cornilly and Verdonck (2018).

The optional arguments include the number of factors, given by `k` and the weight matrix `W`, see the examples.

References

Boudt, Kris, Dries Cornilly and Tim Verdonck. 2020. Nearest comoment estimation with unobserved factors. Journal of Econometrics, 217(2), 381-397.

Examples

if (FALSE) # CRAN doesn't like how long this takes (>5 secs)

data(edhec)

# default estimator

est_nc <- MM.NCE(edhec[, 1:3] * 100)

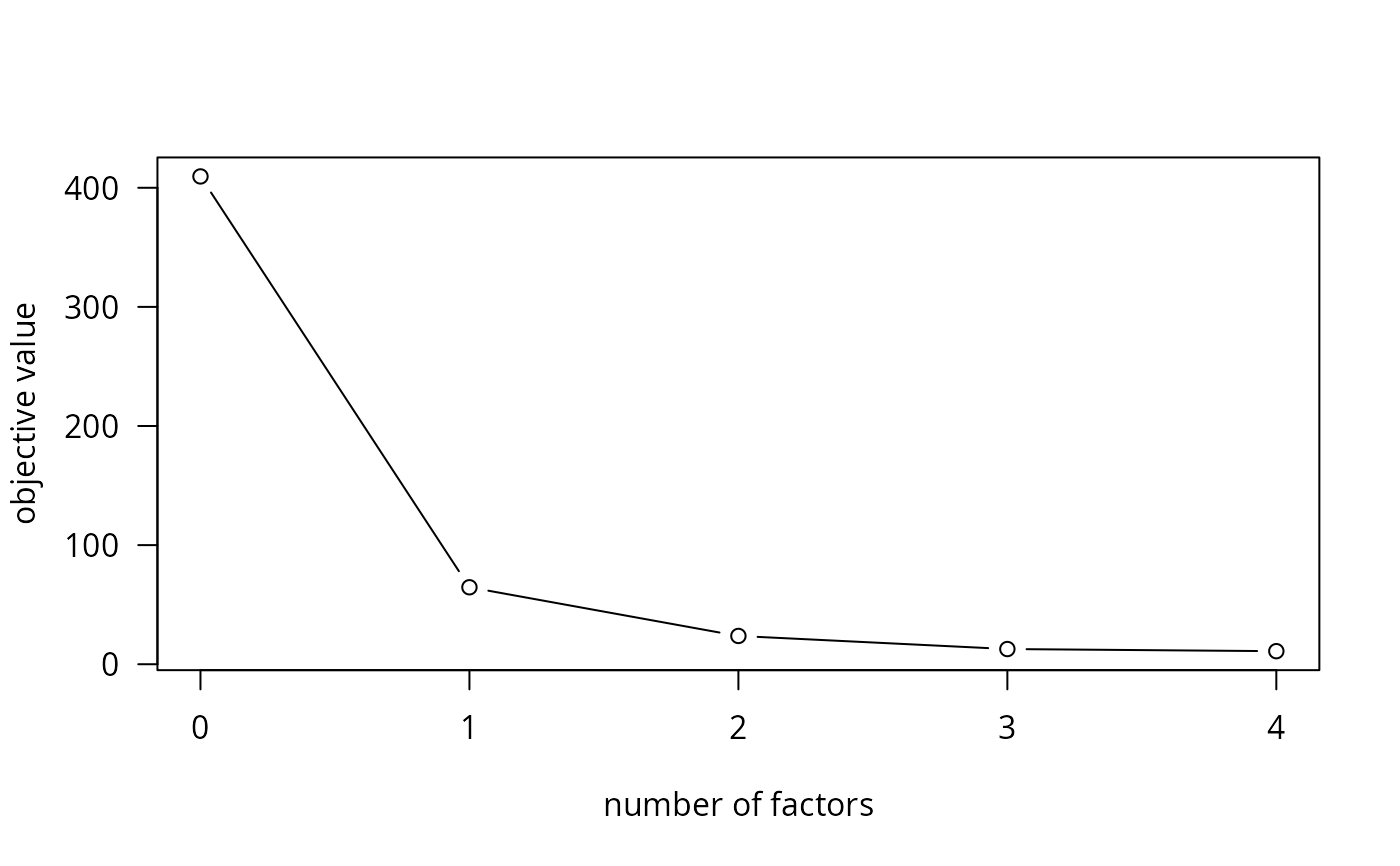

# scree plot to determine number of factors

obj <- rep(NA, 5)

for (ii in 1:5) {

est_nc <- MM.NCE(edhec[, 1:5] * 100, k = ii - 1)

obj[ii] <- est_nc$optim.sol$objective * nrow(edhec[, 1:5])

}

plot(0:4, obj, type = 'b', xlab = "number of factors",

ylab = "objective value", las = 1)

# bootstrapped estimator

est_nc <- MM.NCE(edhec[, 1:2] * 100, W = list("Wid" = "RidgeD",

"alpha" = NULL, "nb" = 250, "alphavec" = seq(0.2, 1, by = 0.2)))

# ridge weight matrix with alpha = 0.5

est_nc <- MM.NCE(edhec[, 1:2] * 100, W = list("Wid" = "RidgeD", "alpha" = 0.5))

# \dontrun{} # end \dontrun

# bootstrapped estimator

est_nc <- MM.NCE(edhec[, 1:2] * 100, W = list("Wid" = "RidgeD",

"alpha" = NULL, "nb" = 250, "alphavec" = seq(0.2, 1, by = 0.2)))

# ridge weight matrix with alpha = 0.5

est_nc <- MM.NCE(edhec[, 1:2] * 100, W = list("Wid" = "RidgeD", "alpha" = 0.5))

# \dontrun{} # end \dontrun