MSCI Switzerland Index

MSCISwitzerland.RdTime series of the MSCI Switzerland index.

Usage

data("MSCISwitzerland")Format

A daily univariate time series from 1994-12-30 to 2012-12-31 (of class "zoo" with "Date" index).

References

Ding, Z., Granger, C. W. J. and Engle, R. F. (1993). A Long Memory Property of Stock Market Returns and a New Model. Journal of Empirical Finance, 1(1), 83–106.

Franses, P.H., van Dijk, D. and Opschoor, A. (2014). Time Series Models for Business and Economic Forecasting, 2nd ed. Cambridge, UK: Cambridge University Press.

Examples

#> Loading required namespace: fGarch

#> Loading required namespace: rugarch

data("MSCISwitzerland", package = "AER")

## p.190, Fig. 7.6

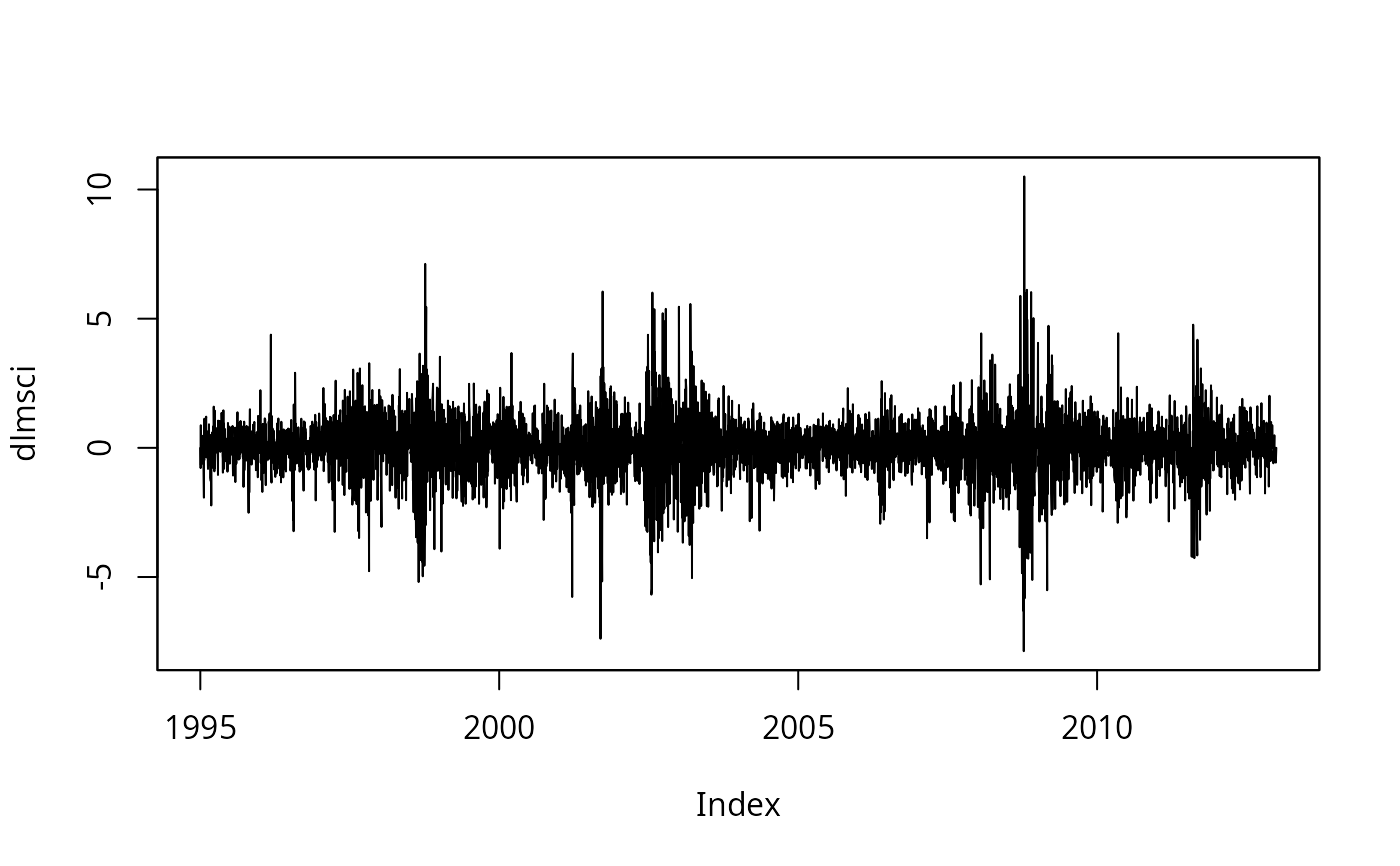

dlmsci <- 100 * diff(log(MSCISwitzerland))

plot(dlmsci)

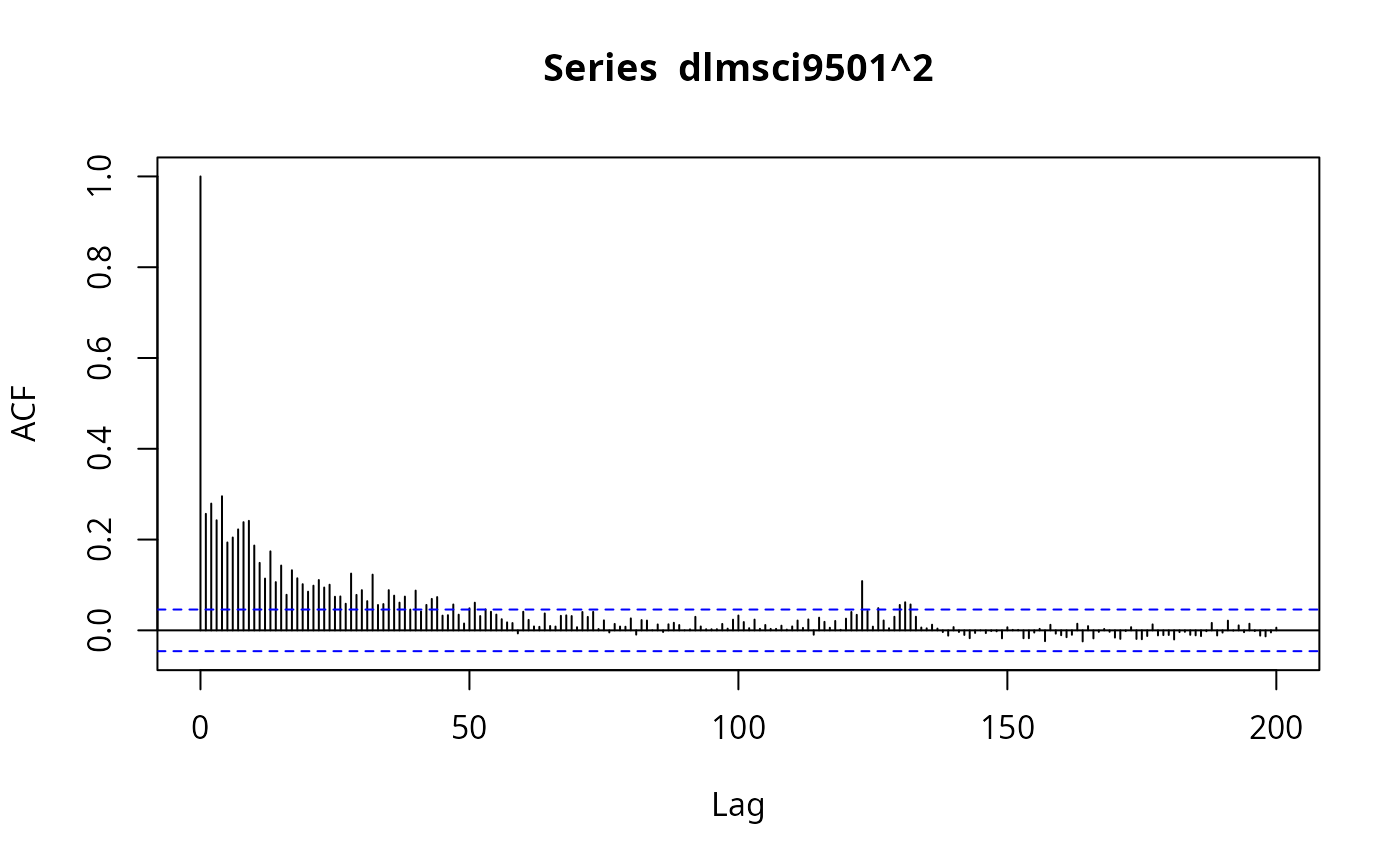

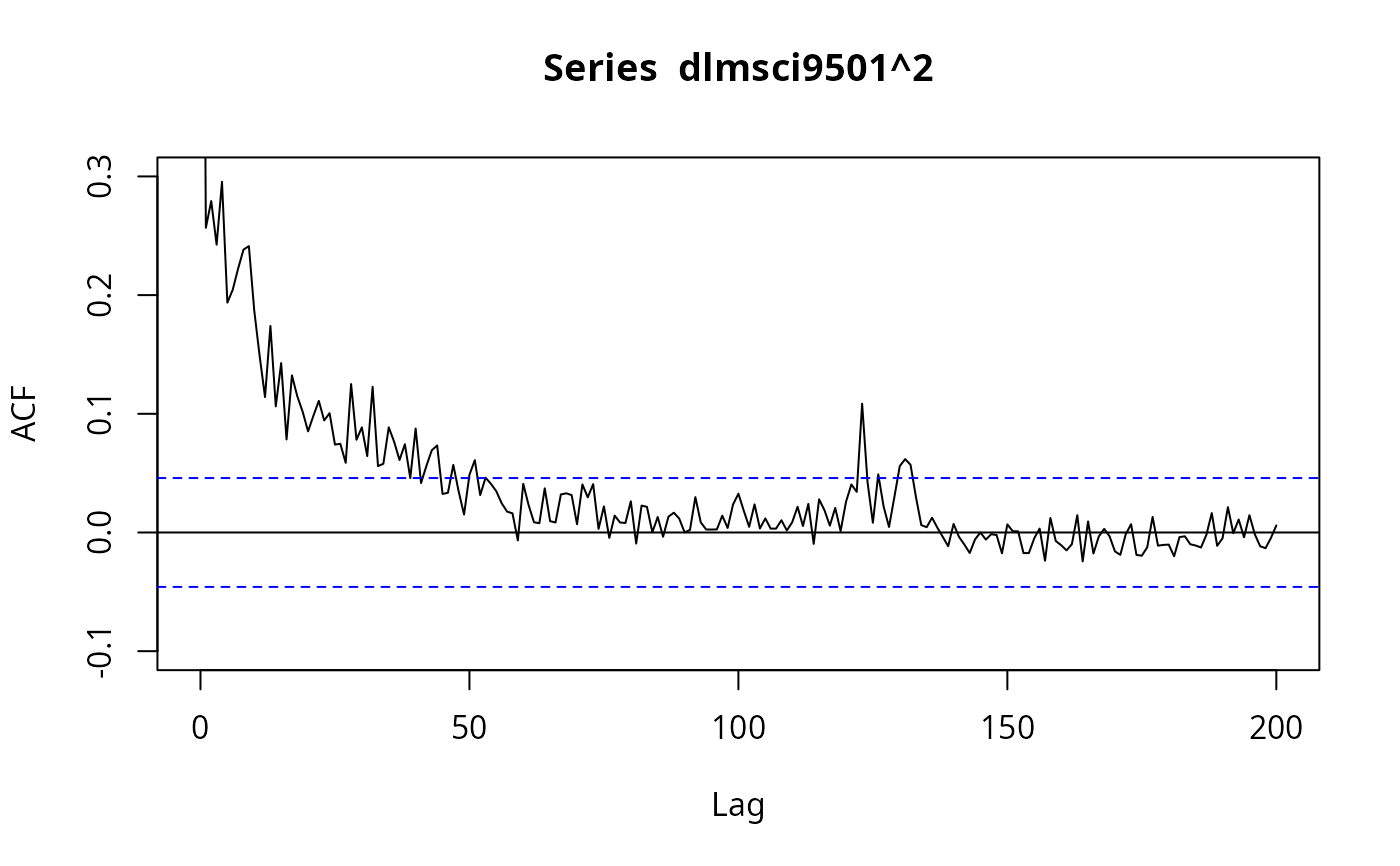

dlmsci9501 <- window(dlmsci, end = as.Date("2001-12-31"))

## Figure 7.7

plot(acf(dlmsci9501^2, lag.max = 200, na.action = na.exclude),

ylim = c(-0.1, 0.3), type = "l")

dlmsci9501 <- window(dlmsci, end = as.Date("2001-12-31"))

## Figure 7.7

plot(acf(dlmsci9501^2, lag.max = 200, na.action = na.exclude),

ylim = c(-0.1, 0.3), type = "l")

## GARCH(1,1) model, p.190, eq. (7.60)

## standard errors using first derivatives (as apparently used by Franses et al.)

library("tseries")

msci9501_g11 <- garch(zooreg(dlmsci9501), trace = FALSE)

summary(msci9501_g11)

#>

#> Call:

#> garch(x = zooreg(dlmsci9501), trace = FALSE)

#>

#> Model:

#> GARCH(1,1)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -5.30570 -0.50860 0.05433 0.68275 5.71286

#>

#> Coefficient(s):

#> Estimate Std. Error t value Pr(>|t|)

#> a0 0.039017 0.007657 5.096 3.48e-07 ***

#> a1 0.115525 0.011968 9.653 < 2e-16 ***

#> b1 0.853031 0.016621 51.323 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Diagnostic Tests:

#> Jarque Bera Test

#>

#> data: Residuals

#> X-squared = 322.29, df = 2, p-value < 2.2e-16

#>

#>

#> Box-Ljung test

#>

#> data: Squared.Residuals

#> X-squared = 0.74665, df = 1, p-value = 0.3875

#>

## standard errors using second derivatives

library("fGarch")

#> NOTE: Packages 'fBasics', 'timeDate', and 'timeSeries' are no longer

#> attached to the search() path when 'fGarch' is attached.

#>

#> If needed attach them yourself in your R script by e.g.,

#> require("timeSeries")

msci9501_g11a <- garchFit( ~ garch(1,1), include.mean = FALSE,

data = dlmsci9501, trace = FALSE)

summary(msci9501_g11a)

#>

#> Title:

#> GARCH Modelling

#>

#> Call:

#> garchFit(formula = ~garch(1, 1), data = dlmsci9501, include.mean = FALSE,

#> trace = FALSE)

#>

#> Mean and Variance Equation:

#> data ~ garch(1, 1)

#> <environment: 0x5bb5ed622368>

#> [data = dlmsci9501]

#>

#> Conditional Distribution:

#> norm

#>

#> Coefficient(s):

#> omega alpha1 beta1

#> 0.039178 0.115480 0.852834

#>

#> Std. Errors:

#> based on Hessian

#>

#> Error Analysis:

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.039178 0.009849 3.978 6.96e-05 ***

#> alpha1 0.115480 0.016283 7.092 1.32e-12 ***

#> beta1 0.852834 0.020529 41.543 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Log Likelihood:

#> -2566.521 normalized: -1.405543

#>

#> Description:

#> Wed Feb 18 21:33:14 2026 by user: andrew

#>

#>

#>

#> Standardised Residuals Tests:

#> Statistic p-Value

#> Jarque-Bera Test R Chi^2 322.9213582 0.000000e+00

#> Shapiro-Wilk Test R W 0.9811351 8.649613e-15

#> Ljung-Box Test R Q(10) 18.7534129 4.350883e-02

#> Ljung-Box Test R Q(15) 20.5383235 1.522397e-01

#> Ljung-Box Test R Q(20) 24.3476524 2.275358e-01

#> Ljung-Box Test R^2 Q(10) 3.4624434 9.683582e-01

#> Ljung-Box Test R^2 Q(15) 5.9656935 9.803183e-01

#> Ljung-Box Test R^2 Q(20) 9.6069360 9.747523e-01

#> LM Arch Test R TR^2 5.3071118 9.469268e-01

#>

#> Information Criterion Statistics:

#> AIC BIC SIC HQIC

#> 2.814372 2.823424 2.814366 2.817711

#>

round(msci9501_g11a@fit$coef, 3)

#> omega alpha1 beta1

#> 0.039 0.115 0.853

round(msci9501_g11a@fit$se.coef, 3)

#> omega alpha1 beta1

#> 0.010 0.016 0.021

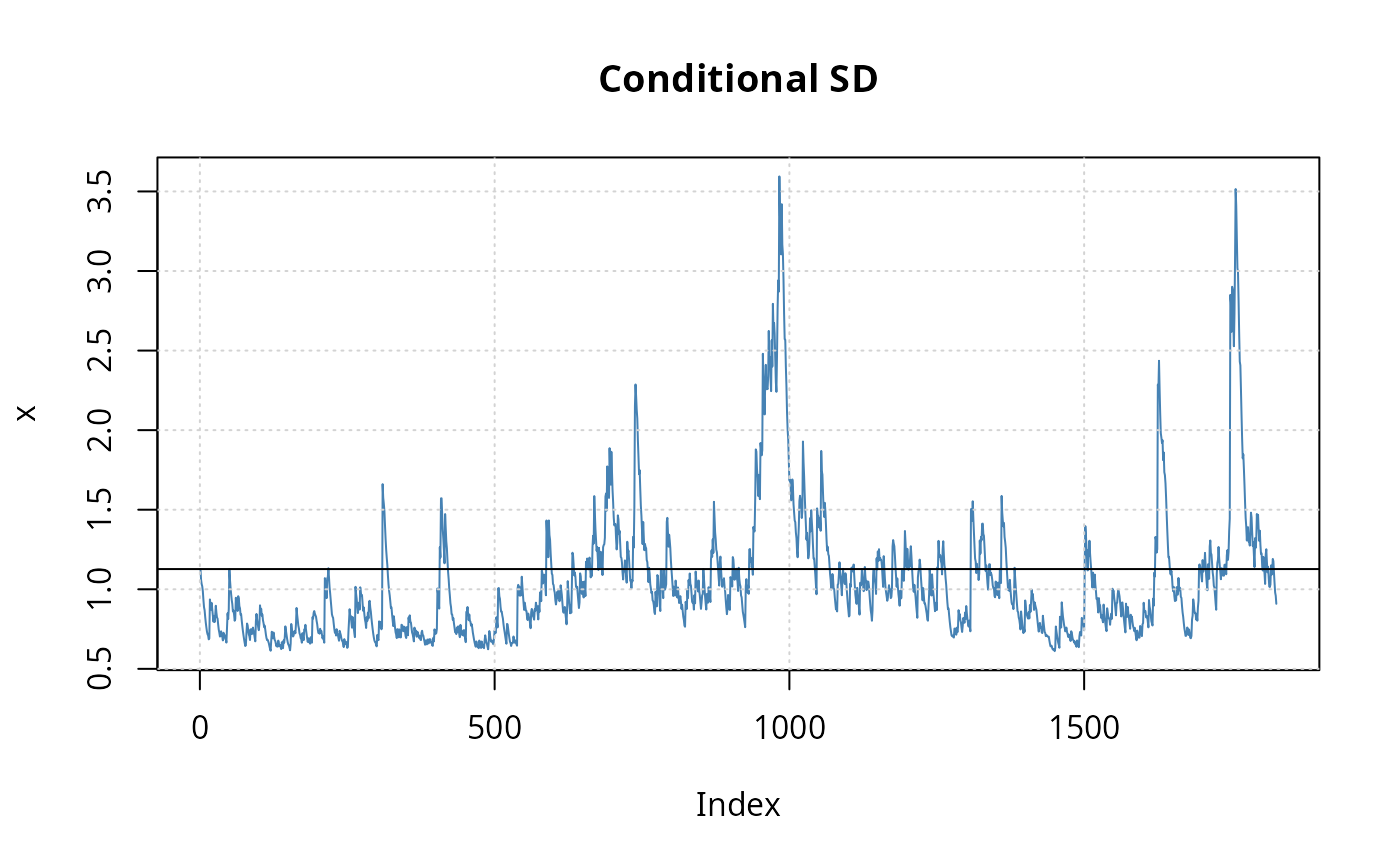

## Fig. 7.8, p.192

plot(msci9501_g11a, which = 2)

abline(h = sd(dlmsci9501))

## GARCH(1,1) model, p.190, eq. (7.60)

## standard errors using first derivatives (as apparently used by Franses et al.)

library("tseries")

msci9501_g11 <- garch(zooreg(dlmsci9501), trace = FALSE)

summary(msci9501_g11)

#>

#> Call:

#> garch(x = zooreg(dlmsci9501), trace = FALSE)

#>

#> Model:

#> GARCH(1,1)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -5.30570 -0.50860 0.05433 0.68275 5.71286

#>

#> Coefficient(s):

#> Estimate Std. Error t value Pr(>|t|)

#> a0 0.039017 0.007657 5.096 3.48e-07 ***

#> a1 0.115525 0.011968 9.653 < 2e-16 ***

#> b1 0.853031 0.016621 51.323 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Diagnostic Tests:

#> Jarque Bera Test

#>

#> data: Residuals

#> X-squared = 322.29, df = 2, p-value < 2.2e-16

#>

#>

#> Box-Ljung test

#>

#> data: Squared.Residuals

#> X-squared = 0.74665, df = 1, p-value = 0.3875

#>

## standard errors using second derivatives

library("fGarch")

#> NOTE: Packages 'fBasics', 'timeDate', and 'timeSeries' are no longer

#> attached to the search() path when 'fGarch' is attached.

#>

#> If needed attach them yourself in your R script by e.g.,

#> require("timeSeries")

msci9501_g11a <- garchFit( ~ garch(1,1), include.mean = FALSE,

data = dlmsci9501, trace = FALSE)

summary(msci9501_g11a)

#>

#> Title:

#> GARCH Modelling

#>

#> Call:

#> garchFit(formula = ~garch(1, 1), data = dlmsci9501, include.mean = FALSE,

#> trace = FALSE)

#>

#> Mean and Variance Equation:

#> data ~ garch(1, 1)

#> <environment: 0x5bb5ed622368>

#> [data = dlmsci9501]

#>

#> Conditional Distribution:

#> norm

#>

#> Coefficient(s):

#> omega alpha1 beta1

#> 0.039178 0.115480 0.852834

#>

#> Std. Errors:

#> based on Hessian

#>

#> Error Analysis:

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.039178 0.009849 3.978 6.96e-05 ***

#> alpha1 0.115480 0.016283 7.092 1.32e-12 ***

#> beta1 0.852834 0.020529 41.543 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Log Likelihood:

#> -2566.521 normalized: -1.405543

#>

#> Description:

#> Wed Feb 18 21:33:14 2026 by user: andrew

#>

#>

#>

#> Standardised Residuals Tests:

#> Statistic p-Value

#> Jarque-Bera Test R Chi^2 322.9213582 0.000000e+00

#> Shapiro-Wilk Test R W 0.9811351 8.649613e-15

#> Ljung-Box Test R Q(10) 18.7534129 4.350883e-02

#> Ljung-Box Test R Q(15) 20.5383235 1.522397e-01

#> Ljung-Box Test R Q(20) 24.3476524 2.275358e-01

#> Ljung-Box Test R^2 Q(10) 3.4624434 9.683582e-01

#> Ljung-Box Test R^2 Q(15) 5.9656935 9.803183e-01

#> Ljung-Box Test R^2 Q(20) 9.6069360 9.747523e-01

#> LM Arch Test R TR^2 5.3071118 9.469268e-01

#>

#> Information Criterion Statistics:

#> AIC BIC SIC HQIC

#> 2.814372 2.823424 2.814366 2.817711

#>

round(msci9501_g11a@fit$coef, 3)

#> omega alpha1 beta1

#> 0.039 0.115 0.853

round(msci9501_g11a@fit$se.coef, 3)

#> omega alpha1 beta1

#> 0.010 0.016 0.021

## Fig. 7.8, p.192

plot(msci9501_g11a, which = 2)

abline(h = sd(dlmsci9501))

## TGARCH model (also known as GJR-GARCH model), p. 191, eq. (7.61)

msci9501_tg11 <- garchFit( ~ aparch(1,1), include.mean = FALSE,

include.delta = FALSE, delta = 2, data = dlmsci9501, trace = FALSE)

summary(msci9501_tg11)

#>

#> Title:

#> GARCH Modelling

#>

#> Call:

#> garchFit(formula = ~aparch(1, 1), data = dlmsci9501, delta = 2,

#> include.mean = FALSE, include.delta = FALSE, trace = FALSE)

#>

#> Mean and Variance Equation:

#> data ~ aparch(1, 1)

#> <environment: 0x5bb5eb71b198>

#> [data = dlmsci9501]

#>

#> Conditional Distribution:

#> norm

#>

#> Coefficient(s):

#> omega alpha1 gamma1 beta1

#> 0.050659 0.085286 0.427898 0.856101

#>

#> Std. Errors:

#> based on Hessian

#>

#> Error Analysis:

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.05066 0.01180 4.293 1.76e-05 ***

#> alpha1 0.08529 0.01767 4.825 1.40e-06 ***

#> gamma1 0.42790 0.09671 4.425 9.66e-06 ***

#> beta1 0.85610 0.02348 36.463 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Log Likelihood:

#> -2544.281 normalized: -1.393363

#>

#> Description:

#> Wed Feb 18 21:33:14 2026 by user: andrew

#>

#>

#>

#> Standardised Residuals Tests:

#> Statistic p-Value

#> Jarque-Bera Test R Chi^2 301.5135428 0.000000e+00

#> Shapiro-Wilk Test R W 0.9829266 6.022347e-14

#> Ljung-Box Test R Q(10) 21.5068487 1.782377e-02

#> Ljung-Box Test R Q(15) 23.6240653 7.175874e-02

#> Ljung-Box Test R Q(20) 27.8841646 1.121699e-01

#> Ljung-Box Test R^2 Q(10) 3.9434228 9.498632e-01

#> Ljung-Box Test R^2 Q(15) 5.8177948 9.826484e-01

#> Ljung-Box Test R^2 Q(20) 8.4910980 9.880874e-01

#> LM Arch Test R TR^2 5.4457693 9.414114e-01

#>

#> Information Criterion Statistics:

#> AIC BIC SIC HQIC

#> 2.791107 2.803177 2.791098 2.795560

#>

## GJR form using reparameterization as given by Ding et al. (1993, pp. 100-101)

coef(msci9501_tg11)["alpha1"] * (1 - coef(msci9501_tg11)["gamma1"])^2 ## alpha*

#> alpha1

#> 0.02791431

4 * coef(msci9501_tg11)["alpha1"] * coef(msci9501_tg11)["gamma1"] ## gamma*

#> alpha1

#> 0.1459754

## GARCH and GJR-GARCH with rugarch

# \donttest{

library("rugarch")

#> Loading required package: parallel

spec_g11 <- ugarchspec(variance.model = list(model = "sGARCH"),

mean.model = list(armaOrder = c(0,0), include.mean = FALSE))

msci9501_g11b <- ugarchfit(spec_g11, data = dlmsci9501)

msci9501_g11b

#>

#> *---------------------------------*

#> * GARCH Model Fit *

#> *---------------------------------*

#>

#> Conditional Variance Dynamics

#> -----------------------------------

#> GARCH Model : sGARCH(1,1)

#> Mean Model : ARFIMA(0,0,0)

#> Distribution : norm

#>

#> Optimal Parameters

#> ------------------------------------

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.039146 0.009900 3.9541 7.7e-05

#> alpha1 0.115593 0.016357 7.0667 0.0e+00

#> beta1 0.852837 0.020635 41.3304 0.0e+00

#>

#> Robust Standard Errors:

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.039146 0.014155 2.7655 0.005683

#> alpha1 0.115593 0.023507 4.9173 0.000001

#> beta1 0.852837 0.027962 30.5004 0.000000

#>

#> LogLikelihood : -2566.524

#>

#> Information Criteria

#> ------------------------------------

#>

#> Akaike 2.8144

#> Bayes 2.8234

#> Shibata 2.8144

#> Hannan-Quinn 2.8177

#>

#> Weighted Ljung-Box Test on Standardized Residuals

#> ------------------------------------

#> statistic p-value

#> Lag[1] 3.130 0.07685

#> Lag[2*(p+q)+(p+q)-1][2] 3.425 0.10769

#> Lag[4*(p+q)+(p+q)-1][5] 4.939 0.15804

#> d.o.f=0

#> H0 : No serial correlation

#>

#> Weighted Ljung-Box Test on Standardized Squared Residuals

#> ------------------------------------

#> statistic p-value

#> Lag[1] 0.7428 0.3888

#> Lag[2*(p+q)+(p+q)-1][5] 1.3179 0.7845

#> Lag[4*(p+q)+(p+q)-1][9] 1.9604 0.9097

#> d.o.f=2

#>

#> Weighted ARCH LM Tests

#> ------------------------------------

#> Statistic Shape Scale P-Value

#> ARCH Lag[3] 0.3748 0.500 2.000 0.5404

#> ARCH Lag[5] 0.7871 1.440 1.667 0.7970

#> ARCH Lag[7] 1.1653 2.315 1.543 0.8853

#>

#> Nyblom stability test

#> ------------------------------------

#> Joint Statistic: 0.7441

#> Individual Statistics:

#> omega 0.3792

#> alpha1 0.3782

#> beta1 0.4055

#>

#> Asymptotic Critical Values (10% 5% 1%)

#> Joint Statistic: 0.846 1.01 1.35

#> Individual Statistic: 0.35 0.47 0.75

#>

#> Sign Bias Test

#> ------------------------------------

#> t-value prob sig

#> Sign Bias 1.208 0.2271695

#> Negative Sign Bias 2.213 0.0270343 **

#> Positive Sign Bias 3.177 0.0015143 ***

#> Joint Effect 19.166 0.0002526 ***

#>

#>

#> Adjusted Pearson Goodness-of-Fit Test:

#> ------------------------------------

#> group statistic p-value(g-1)

#> 1 20 125.5 1.011e-17

#> 2 30 146.6 1.168e-17

#> 3 40 179.5 6.391e-20

#> 4 50 206.7 2.904e-21

#>

#>

#> Elapsed time : 0.1491868

#>

spec_gjrg11 <- ugarchspec(variance.model = list(model = "gjrGARCH", garchOrder = c(1,1)),

mean.model = list(armaOrder = c(0, 0), include.mean = FALSE))

msci9501_gjrg11 <- ugarchfit(spec_gjrg11, data = dlmsci9501)

msci9501_gjrg11

#>

#> *---------------------------------*

#> * GARCH Model Fit *

#> *---------------------------------*

#>

#> Conditional Variance Dynamics

#> -----------------------------------

#> GARCH Model : gjrGARCH(1,1)

#> Mean Model : ARFIMA(0,0,0)

#> Distribution : norm

#>

#> Optimal Parameters

#> ------------------------------------

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.050626 0.011895 4.2561 0.000021

#> alpha1 0.028150 0.013916 2.0229 0.043084

#> beta1 0.856027 0.023672 36.1618 0.000000

#> gamma1 0.145862 0.026995 5.4032 0.000000

#>

#> Robust Standard Errors:

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.050626 0.020469 2.4733 0.013387

#> alpha1 0.028150 0.014244 1.9763 0.048116

#> beta1 0.856027 0.035439 24.1551 0.000000

#> gamma1 0.145862 0.042111 3.4638 0.000533

#>

#> LogLikelihood : -2544.334

#>

#> Information Criteria

#> ------------------------------------

#>

#> Akaike 2.7912

#> Bayes 2.8032

#> Shibata 2.7912

#> Hannan-Quinn 2.7956

#>

#> Weighted Ljung-Box Test on Standardized Residuals

#> ------------------------------------

#> statistic p-value

#> Lag[1] 4.450 0.03490

#> Lag[2*(p+q)+(p+q)-1][2] 4.878 0.04385

#> Lag[4*(p+q)+(p+q)-1][5] 6.638 0.06343

#> d.o.f=0

#> H0 : No serial correlation

#>

#> Weighted Ljung-Box Test on Standardized Squared Residuals

#> ------------------------------------

#> statistic p-value

#> Lag[1] 1.198 0.2737

#> Lag[2*(p+q)+(p+q)-1][5] 1.693 0.6926

#> Lag[4*(p+q)+(p+q)-1][9] 2.252 0.8729

#> d.o.f=2

#>

#> Weighted ARCH LM Tests

#> ------------------------------------

#> Statistic Shape Scale P-Value

#> ARCH Lag[3] 0.4704 0.500 2.000 0.4928

#> ARCH Lag[5] 0.4729 1.440 1.667 0.8916

#> ARCH Lag[7] 0.9819 2.315 1.543 0.9165

#>

#> Nyblom stability test

#> ------------------------------------

#> Joint Statistic: 1.2257

#> Individual Statistics:

#> omega 0.3108

#> alpha1 0.3758

#> beta1 0.4500

#> gamma1 0.4197

#>

#> Asymptotic Critical Values (10% 5% 1%)

#> Joint Statistic: 1.07 1.24 1.6

#> Individual Statistic: 0.35 0.47 0.75

#>

#> Sign Bias Test

#> ------------------------------------

#> t-value prob sig

#> Sign Bias 1.0876 0.27690

#> Negative Sign Bias 0.8449 0.39829

#> Positive Sign Bias 2.4336 0.01504 **

#> Joint Effect 7.1624 0.06690 *

#>

#>

#> Adjusted Pearson Goodness-of-Fit Test:

#> ------------------------------------

#> group statistic p-value(g-1)

#> 1 20 120.6 8.429e-17

#> 2 30 150.1 2.758e-18

#> 3 40 168.8 4.371e-18

#> 4 50 181.9 3.651e-17

#>

#>

#> Elapsed time : 0.1416152

#>

round(coef(msci9501_gjrg11), 3)

#> omega alpha1 beta1 gamma1

#> 0.051 0.028 0.856 0.146

# }

## TGARCH model (also known as GJR-GARCH model), p. 191, eq. (7.61)

msci9501_tg11 <- garchFit( ~ aparch(1,1), include.mean = FALSE,

include.delta = FALSE, delta = 2, data = dlmsci9501, trace = FALSE)

summary(msci9501_tg11)

#>

#> Title:

#> GARCH Modelling

#>

#> Call:

#> garchFit(formula = ~aparch(1, 1), data = dlmsci9501, delta = 2,

#> include.mean = FALSE, include.delta = FALSE, trace = FALSE)

#>

#> Mean and Variance Equation:

#> data ~ aparch(1, 1)

#> <environment: 0x5bb5eb71b198>

#> [data = dlmsci9501]

#>

#> Conditional Distribution:

#> norm

#>

#> Coefficient(s):

#> omega alpha1 gamma1 beta1

#> 0.050659 0.085286 0.427898 0.856101

#>

#> Std. Errors:

#> based on Hessian

#>

#> Error Analysis:

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.05066 0.01180 4.293 1.76e-05 ***

#> alpha1 0.08529 0.01767 4.825 1.40e-06 ***

#> gamma1 0.42790 0.09671 4.425 9.66e-06 ***

#> beta1 0.85610 0.02348 36.463 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Log Likelihood:

#> -2544.281 normalized: -1.393363

#>

#> Description:

#> Wed Feb 18 21:33:14 2026 by user: andrew

#>

#>

#>

#> Standardised Residuals Tests:

#> Statistic p-Value

#> Jarque-Bera Test R Chi^2 301.5135428 0.000000e+00

#> Shapiro-Wilk Test R W 0.9829266 6.022347e-14

#> Ljung-Box Test R Q(10) 21.5068487 1.782377e-02

#> Ljung-Box Test R Q(15) 23.6240653 7.175874e-02

#> Ljung-Box Test R Q(20) 27.8841646 1.121699e-01

#> Ljung-Box Test R^2 Q(10) 3.9434228 9.498632e-01

#> Ljung-Box Test R^2 Q(15) 5.8177948 9.826484e-01

#> Ljung-Box Test R^2 Q(20) 8.4910980 9.880874e-01

#> LM Arch Test R TR^2 5.4457693 9.414114e-01

#>

#> Information Criterion Statistics:

#> AIC BIC SIC HQIC

#> 2.791107 2.803177 2.791098 2.795560

#>

## GJR form using reparameterization as given by Ding et al. (1993, pp. 100-101)

coef(msci9501_tg11)["alpha1"] * (1 - coef(msci9501_tg11)["gamma1"])^2 ## alpha*

#> alpha1

#> 0.02791431

4 * coef(msci9501_tg11)["alpha1"] * coef(msci9501_tg11)["gamma1"] ## gamma*

#> alpha1

#> 0.1459754

## GARCH and GJR-GARCH with rugarch

# \donttest{

library("rugarch")

#> Loading required package: parallel

spec_g11 <- ugarchspec(variance.model = list(model = "sGARCH"),

mean.model = list(armaOrder = c(0,0), include.mean = FALSE))

msci9501_g11b <- ugarchfit(spec_g11, data = dlmsci9501)

msci9501_g11b

#>

#> *---------------------------------*

#> * GARCH Model Fit *

#> *---------------------------------*

#>

#> Conditional Variance Dynamics

#> -----------------------------------

#> GARCH Model : sGARCH(1,1)

#> Mean Model : ARFIMA(0,0,0)

#> Distribution : norm

#>

#> Optimal Parameters

#> ------------------------------------

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.039146 0.009900 3.9541 7.7e-05

#> alpha1 0.115593 0.016357 7.0667 0.0e+00

#> beta1 0.852837 0.020635 41.3304 0.0e+00

#>

#> Robust Standard Errors:

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.039146 0.014155 2.7655 0.005683

#> alpha1 0.115593 0.023507 4.9173 0.000001

#> beta1 0.852837 0.027962 30.5004 0.000000

#>

#> LogLikelihood : -2566.524

#>

#> Information Criteria

#> ------------------------------------

#>

#> Akaike 2.8144

#> Bayes 2.8234

#> Shibata 2.8144

#> Hannan-Quinn 2.8177

#>

#> Weighted Ljung-Box Test on Standardized Residuals

#> ------------------------------------

#> statistic p-value

#> Lag[1] 3.130 0.07685

#> Lag[2*(p+q)+(p+q)-1][2] 3.425 0.10769

#> Lag[4*(p+q)+(p+q)-1][5] 4.939 0.15804

#> d.o.f=0

#> H0 : No serial correlation

#>

#> Weighted Ljung-Box Test on Standardized Squared Residuals

#> ------------------------------------

#> statistic p-value

#> Lag[1] 0.7428 0.3888

#> Lag[2*(p+q)+(p+q)-1][5] 1.3179 0.7845

#> Lag[4*(p+q)+(p+q)-1][9] 1.9604 0.9097

#> d.o.f=2

#>

#> Weighted ARCH LM Tests

#> ------------------------------------

#> Statistic Shape Scale P-Value

#> ARCH Lag[3] 0.3748 0.500 2.000 0.5404

#> ARCH Lag[5] 0.7871 1.440 1.667 0.7970

#> ARCH Lag[7] 1.1653 2.315 1.543 0.8853

#>

#> Nyblom stability test

#> ------------------------------------

#> Joint Statistic: 0.7441

#> Individual Statistics:

#> omega 0.3792

#> alpha1 0.3782

#> beta1 0.4055

#>

#> Asymptotic Critical Values (10% 5% 1%)

#> Joint Statistic: 0.846 1.01 1.35

#> Individual Statistic: 0.35 0.47 0.75

#>

#> Sign Bias Test

#> ------------------------------------

#> t-value prob sig

#> Sign Bias 1.208 0.2271695

#> Negative Sign Bias 2.213 0.0270343 **

#> Positive Sign Bias 3.177 0.0015143 ***

#> Joint Effect 19.166 0.0002526 ***

#>

#>

#> Adjusted Pearson Goodness-of-Fit Test:

#> ------------------------------------

#> group statistic p-value(g-1)

#> 1 20 125.5 1.011e-17

#> 2 30 146.6 1.168e-17

#> 3 40 179.5 6.391e-20

#> 4 50 206.7 2.904e-21

#>

#>

#> Elapsed time : 0.1491868

#>

spec_gjrg11 <- ugarchspec(variance.model = list(model = "gjrGARCH", garchOrder = c(1,1)),

mean.model = list(armaOrder = c(0, 0), include.mean = FALSE))

msci9501_gjrg11 <- ugarchfit(spec_gjrg11, data = dlmsci9501)

msci9501_gjrg11

#>

#> *---------------------------------*

#> * GARCH Model Fit *

#> *---------------------------------*

#>

#> Conditional Variance Dynamics

#> -----------------------------------

#> GARCH Model : gjrGARCH(1,1)

#> Mean Model : ARFIMA(0,0,0)

#> Distribution : norm

#>

#> Optimal Parameters

#> ------------------------------------

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.050626 0.011895 4.2561 0.000021

#> alpha1 0.028150 0.013916 2.0229 0.043084

#> beta1 0.856027 0.023672 36.1618 0.000000

#> gamma1 0.145862 0.026995 5.4032 0.000000

#>

#> Robust Standard Errors:

#> Estimate Std. Error t value Pr(>|t|)

#> omega 0.050626 0.020469 2.4733 0.013387

#> alpha1 0.028150 0.014244 1.9763 0.048116

#> beta1 0.856027 0.035439 24.1551 0.000000

#> gamma1 0.145862 0.042111 3.4638 0.000533

#>

#> LogLikelihood : -2544.334

#>

#> Information Criteria

#> ------------------------------------

#>

#> Akaike 2.7912

#> Bayes 2.8032

#> Shibata 2.7912

#> Hannan-Quinn 2.7956

#>

#> Weighted Ljung-Box Test on Standardized Residuals

#> ------------------------------------

#> statistic p-value

#> Lag[1] 4.450 0.03490

#> Lag[2*(p+q)+(p+q)-1][2] 4.878 0.04385

#> Lag[4*(p+q)+(p+q)-1][5] 6.638 0.06343

#> d.o.f=0

#> H0 : No serial correlation

#>

#> Weighted Ljung-Box Test on Standardized Squared Residuals

#> ------------------------------------

#> statistic p-value

#> Lag[1] 1.198 0.2737

#> Lag[2*(p+q)+(p+q)-1][5] 1.693 0.6926

#> Lag[4*(p+q)+(p+q)-1][9] 2.252 0.8729

#> d.o.f=2

#>

#> Weighted ARCH LM Tests

#> ------------------------------------

#> Statistic Shape Scale P-Value

#> ARCH Lag[3] 0.4704 0.500 2.000 0.4928

#> ARCH Lag[5] 0.4729 1.440 1.667 0.8916

#> ARCH Lag[7] 0.9819 2.315 1.543 0.9165

#>

#> Nyblom stability test

#> ------------------------------------

#> Joint Statistic: 1.2257

#> Individual Statistics:

#> omega 0.3108

#> alpha1 0.3758

#> beta1 0.4500

#> gamma1 0.4197

#>

#> Asymptotic Critical Values (10% 5% 1%)

#> Joint Statistic: 1.07 1.24 1.6

#> Individual Statistic: 0.35 0.47 0.75

#>

#> Sign Bias Test

#> ------------------------------------

#> t-value prob sig

#> Sign Bias 1.0876 0.27690

#> Negative Sign Bias 0.8449 0.39829

#> Positive Sign Bias 2.4336 0.01504 **

#> Joint Effect 7.1624 0.06690 *

#>

#>

#> Adjusted Pearson Goodness-of-Fit Test:

#> ------------------------------------

#> group statistic p-value(g-1)

#> 1 20 120.6 8.429e-17

#> 2 30 150.1 2.758e-18

#> 3 40 168.8 4.371e-18

#> 4 50 181.9 3.651e-17

#>

#>

#> Elapsed time : 0.1416152

#>

round(coef(msci9501_gjrg11), 3)

#> omega alpha1 beta1 gamma1

#> 0.051 0.028 0.856 0.146

# }