Gold and Silver Prices

GoldSilver.RdTime series of gold and silver prices.

Usage

data("GoldSilver")Format

A daily multiple time series from 1977-12-30 to 2012-12-31 (of class "zoo" with "Date" index).

- gold

spot price for gold,

- silver

spot price for silver.

References

Franses, P.H., van Dijk, D. and Opschoor, A. (2014). Time Series Models for Business and Economic Forecasting, 2nd ed. Cambridge, UK: Cambridge University Press.

Examples

#> Loading required namespace: longmemo

#> Loading required namespace: forecast

#> Loading required namespace: vars

data("GoldSilver", package = "AER")

## p.31, daily returns

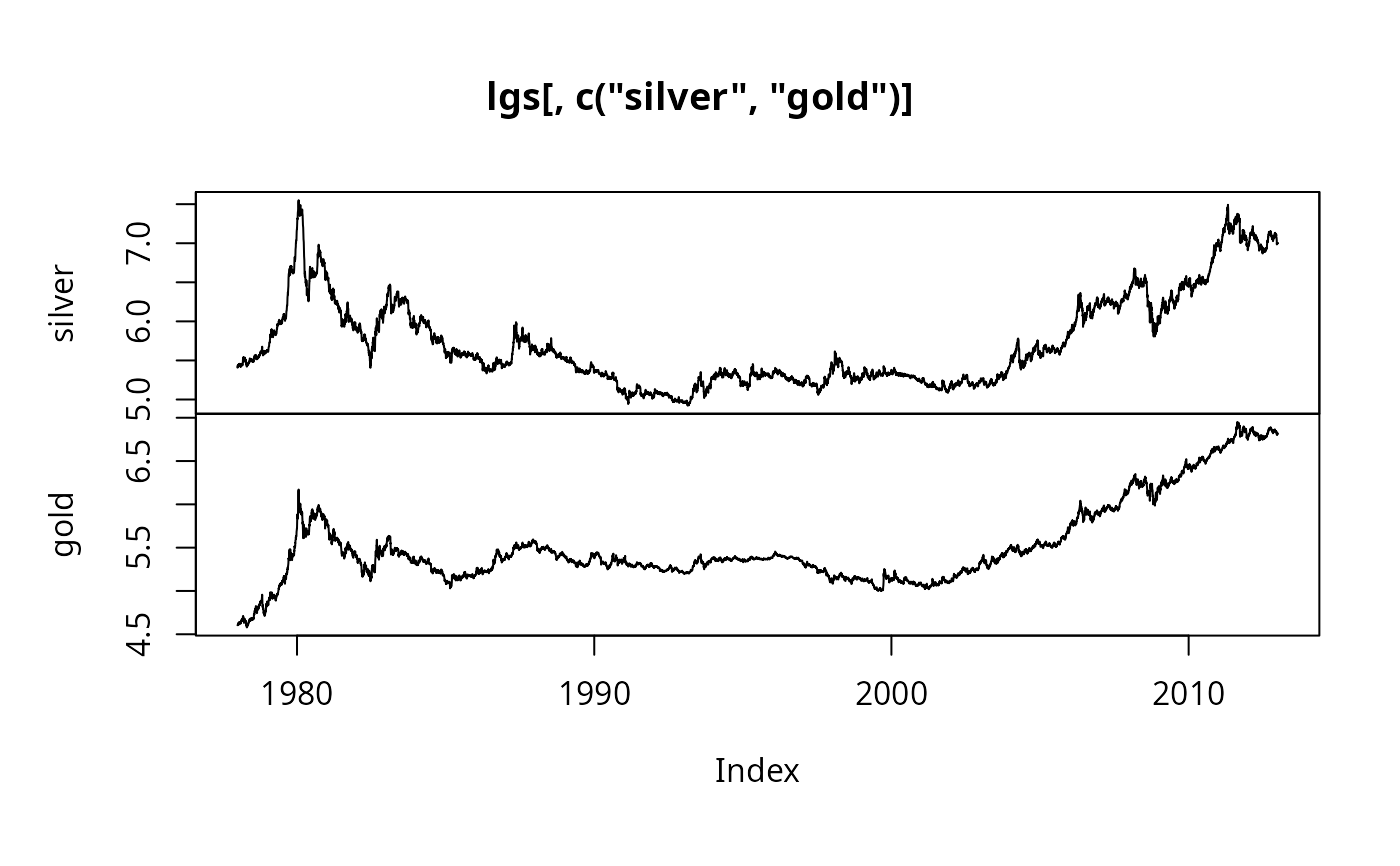

lgs <- log(GoldSilver)

plot(lgs[, c("silver", "gold")])

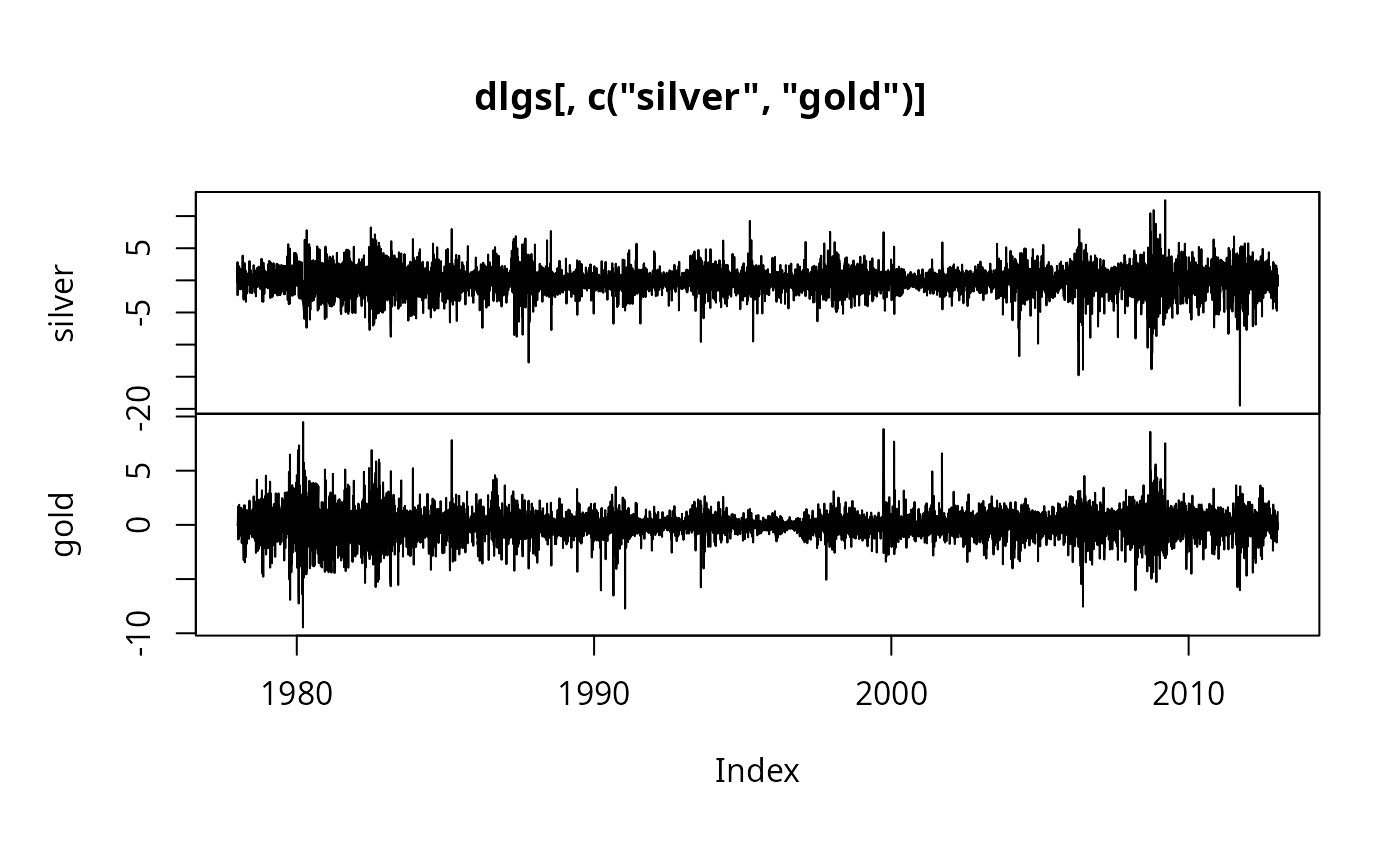

dlgs <- 100 * diff(lgs)

plot(dlgs[, c("silver", "gold")])

dlgs <- 100 * diff(lgs)

plot(dlgs[, c("silver", "gold")])

## p.31, monthly log prices

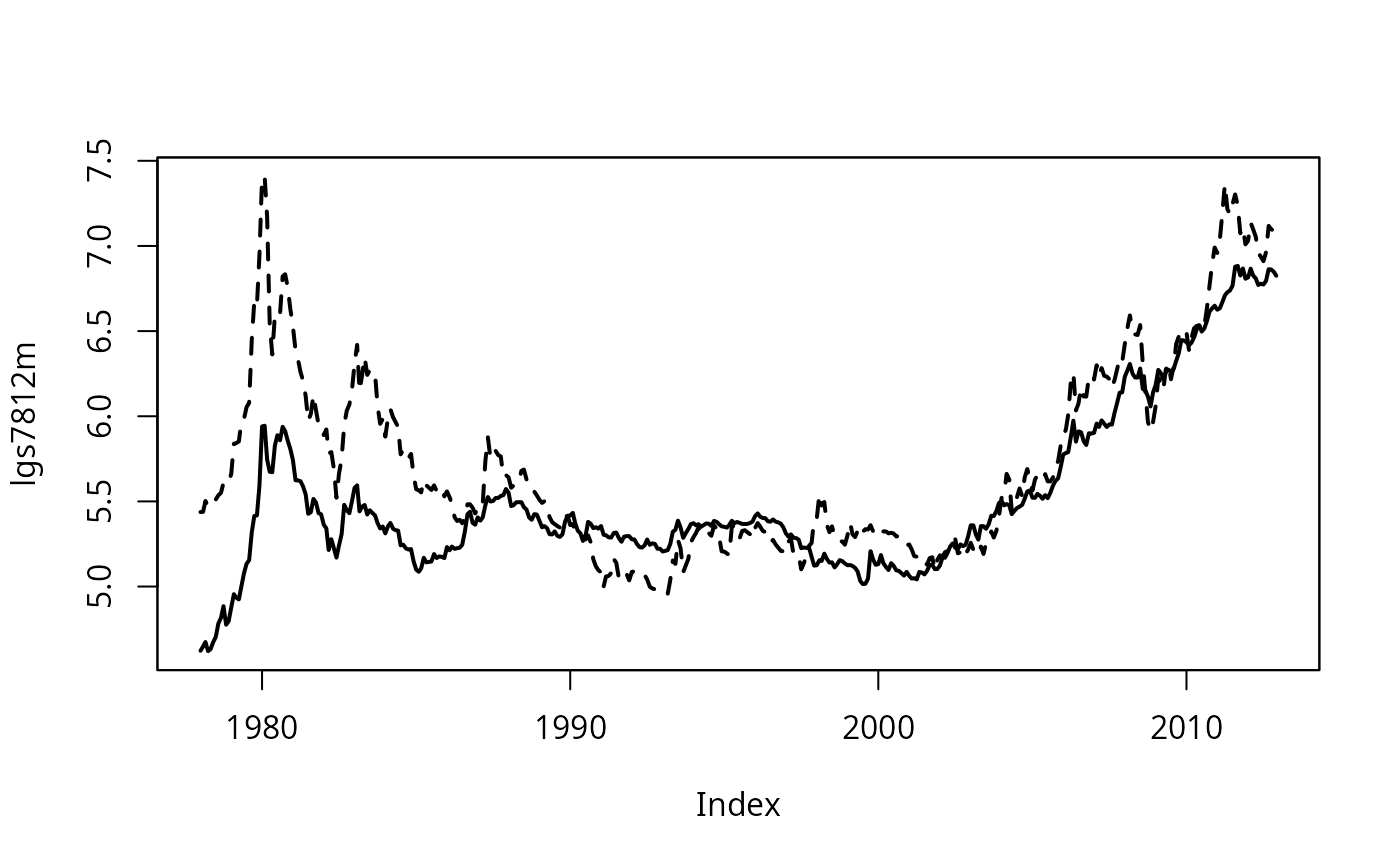

lgs7812 <- window(lgs, start = as.Date("1978-01-01"))

lgs7812m <- aggregate(lgs7812, as.Date(as.yearmon(time(lgs7812))), mean)

plot(lgs7812m, plot.type = "single", lty = 1:2, lwd = 2)

## p.31, monthly log prices

lgs7812 <- window(lgs, start = as.Date("1978-01-01"))

lgs7812m <- aggregate(lgs7812, as.Date(as.yearmon(time(lgs7812))), mean)

plot(lgs7812m, plot.type = "single", lty = 1:2, lwd = 2)

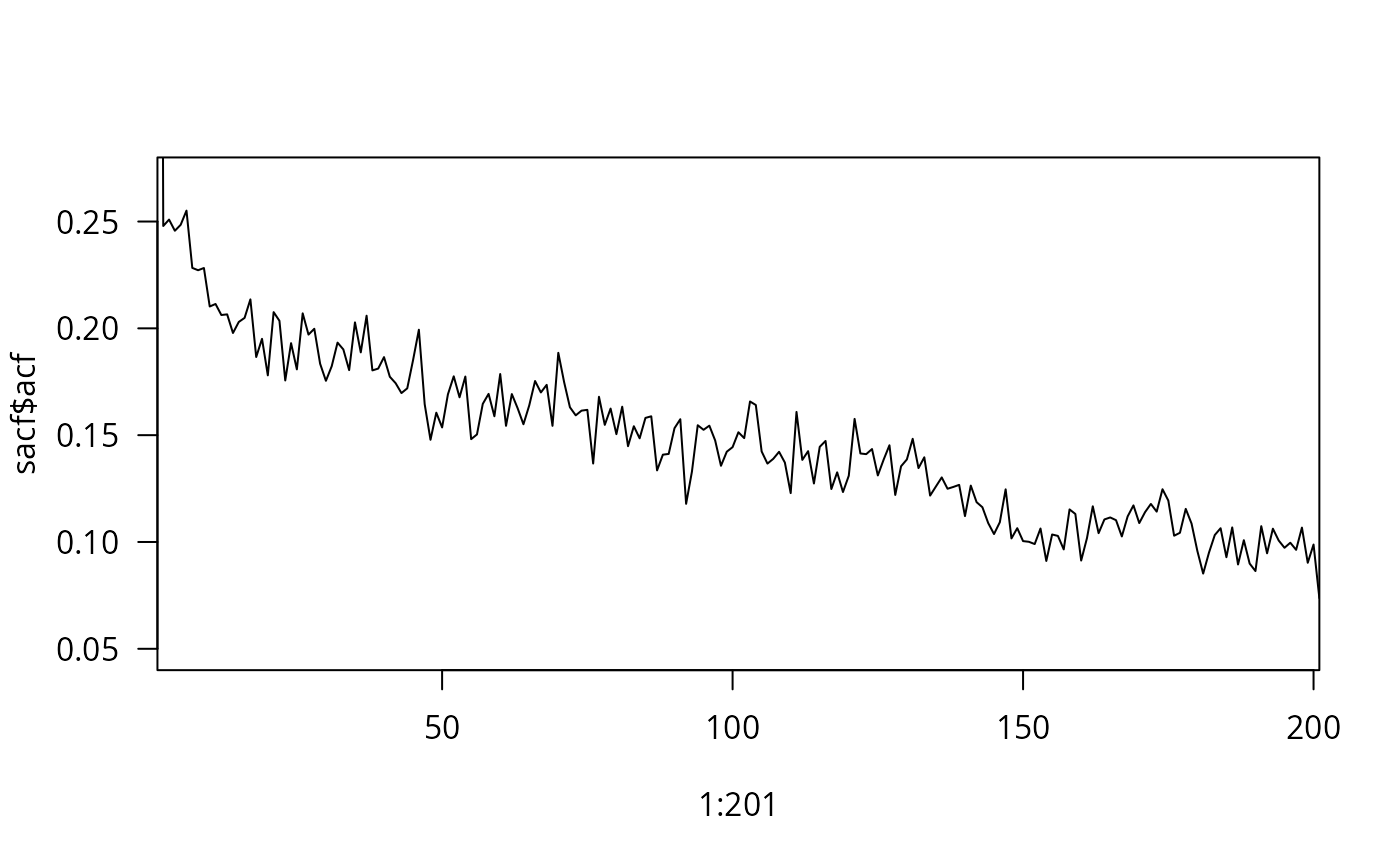

## p.93, empirical ACF of absolute daily gold returns, 1978-01-01 - 2012-12-31

absgret <- abs(100 * diff(lgs7812[, "gold"]))

sacf <- acf(absgret, lag.max = 200, na.action = na.exclude, plot = FALSE)

plot(1:201, sacf$acf, ylim = c(0.04, 0.28), type = "l", xaxs = "i", yaxs = "i", las = 1)

## p.93, empirical ACF of absolute daily gold returns, 1978-01-01 - 2012-12-31

absgret <- abs(100 * diff(lgs7812[, "gold"]))

sacf <- acf(absgret, lag.max = 200, na.action = na.exclude, plot = FALSE)

plot(1:201, sacf$acf, ylim = c(0.04, 0.28), type = "l", xaxs = "i", yaxs = "i", las = 1)

# \donttest{

## ARFIMA(0,1,1) model, eq. (4.44)

library("longmemo")

WhittleEst(absgret, model = "fARIMA", p = 0, q = 1, start = list(H = 0.3, MA = .25))

#> 'WhittleEst' Whittle estimator for fractional ARIMA ('fARIMA'); call:

#> WhittleEst(x = absgret, model = "fARIMA", p = 0, q = 1, start = list(H = 0.3,

#> MA = 0.25))

#> ARMA order (p=0, q=1); time series of length n = 9130.

#>

#> H = 0.8221219

#> coefficients 'eta' =

#> Estimate Std. Error z value Pr(>|z|)

#> H 0.82212189 0.01703983 48.24707 < 2.22e-16

#> MA -0.26559749 0.02096396 -12.66924 < 2.22e-16

#> <==> d := H - 1/2 = 0.322 (0.017)

#>

#> $ vcov : num [1:2, 1:2] 0.00029 -0.000313 -0.000313 0.000439

#> ..- attr(*, "dimnames")=List of 2

#> .. ..$ : chr [1:2] "H" "MA"

#> .. ..$ : chr [1:2] "H" "MA"

#> $ periodogr.x:‘zoo’ series from 1978-01-04 to 1995-07-03

#> Data: num [1:4564] 52.12 4.29 4.45 9.9 4.59 ...

#> Index: Date[1:4564], format: "1978-01-04" "1978-01-05" ...

#> $ spec : num [1:4564, 1] 6.3 4.03 3.1 2.58 2.23 ...

library("forecast")

arfima(as.vector(absgret), max.p = 0, max.q = 1)

#>

#> Call:

#> arfima(y = as.vector(absgret), max.p = 0, max.q = 1)

#>

#> Coefficients:

#> d ma.ma1

#> 0.3492222 0.2972577

#> sigma[eps] = 0.8218654

#> a list with components:

#> [1] "log.likelihood" "n" "msg" "d"

#> [5] "ar" "ma" "covariance.dpq" "fnormMin"

#> [9] "sigma" "stderror.dpq" "correlation.dpq" "h"

#> [13] "d.tol" "M" "hessian.dpq" "length.w"

#> [17] "residuals" "fitted" "call" "x"

#> [21] "series"

# }

## p.254: VAR(2), monthly data for 1986.1 - 2012.12

library("vars")

#> Loading required package: urca

lgs8612 <- window(lgs, start = as.Date("1986-01-01"))

dim(lgs8612)

#> [1] 7044 2

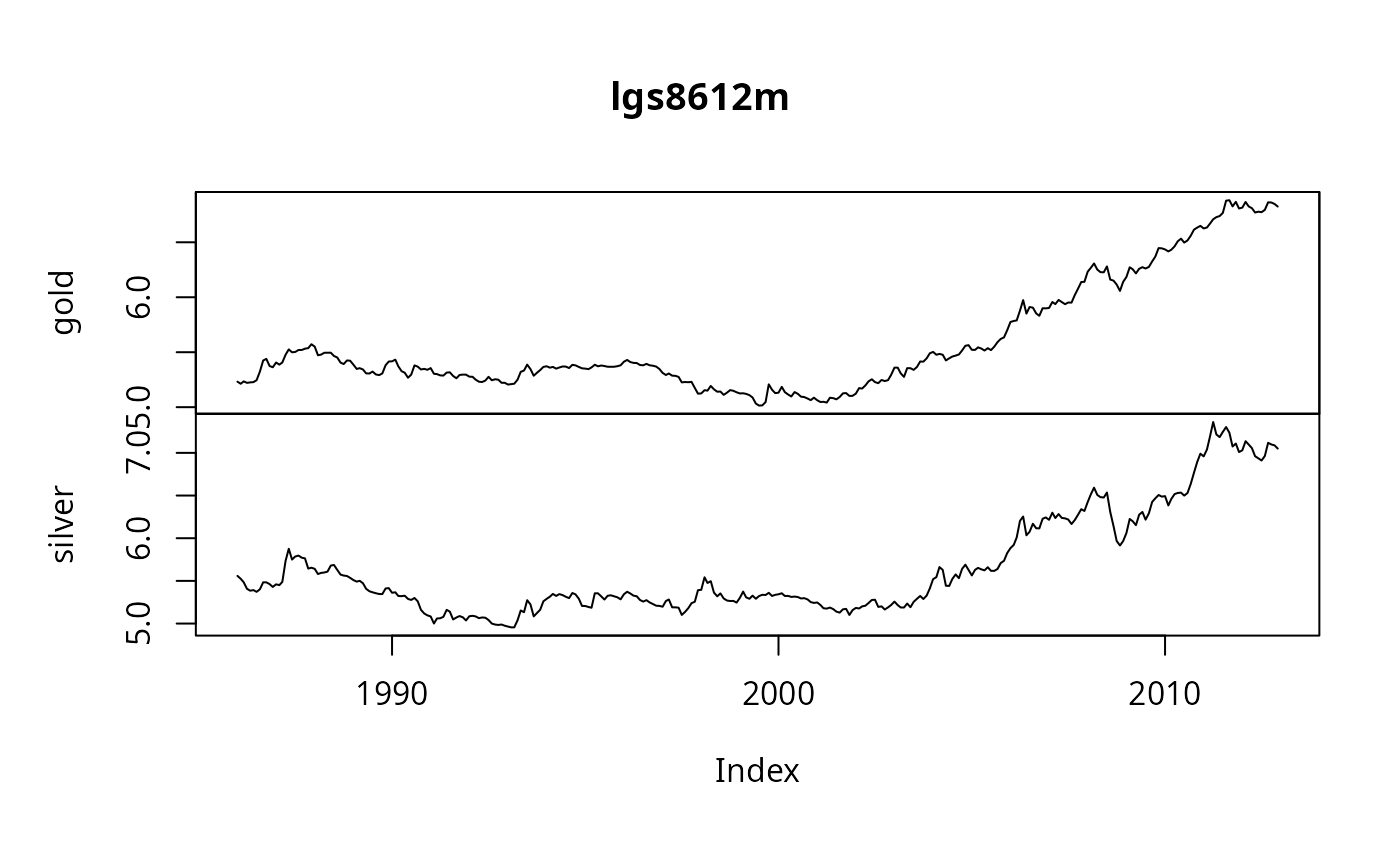

lgs8612m <- aggregate(lgs8612, as.Date(as.yearmon(time(lgs8612))), mean)

plot(lgs8612m)

# \donttest{

## ARFIMA(0,1,1) model, eq. (4.44)

library("longmemo")

WhittleEst(absgret, model = "fARIMA", p = 0, q = 1, start = list(H = 0.3, MA = .25))

#> 'WhittleEst' Whittle estimator for fractional ARIMA ('fARIMA'); call:

#> WhittleEst(x = absgret, model = "fARIMA", p = 0, q = 1, start = list(H = 0.3,

#> MA = 0.25))

#> ARMA order (p=0, q=1); time series of length n = 9130.

#>

#> H = 0.8221219

#> coefficients 'eta' =

#> Estimate Std. Error z value Pr(>|z|)

#> H 0.82212189 0.01703983 48.24707 < 2.22e-16

#> MA -0.26559749 0.02096396 -12.66924 < 2.22e-16

#> <==> d := H - 1/2 = 0.322 (0.017)

#>

#> $ vcov : num [1:2, 1:2] 0.00029 -0.000313 -0.000313 0.000439

#> ..- attr(*, "dimnames")=List of 2

#> .. ..$ : chr [1:2] "H" "MA"

#> .. ..$ : chr [1:2] "H" "MA"

#> $ periodogr.x:‘zoo’ series from 1978-01-04 to 1995-07-03

#> Data: num [1:4564] 52.12 4.29 4.45 9.9 4.59 ...

#> Index: Date[1:4564], format: "1978-01-04" "1978-01-05" ...

#> $ spec : num [1:4564, 1] 6.3 4.03 3.1 2.58 2.23 ...

library("forecast")

arfima(as.vector(absgret), max.p = 0, max.q = 1)

#>

#> Call:

#> arfima(y = as.vector(absgret), max.p = 0, max.q = 1)

#>

#> Coefficients:

#> d ma.ma1

#> 0.3492222 0.2972577

#> sigma[eps] = 0.8218654

#> a list with components:

#> [1] "log.likelihood" "n" "msg" "d"

#> [5] "ar" "ma" "covariance.dpq" "fnormMin"

#> [9] "sigma" "stderror.dpq" "correlation.dpq" "h"

#> [13] "d.tol" "M" "hessian.dpq" "length.w"

#> [17] "residuals" "fitted" "call" "x"

#> [21] "series"

# }

## p.254: VAR(2), monthly data for 1986.1 - 2012.12

library("vars")

#> Loading required package: urca

lgs8612 <- window(lgs, start = as.Date("1986-01-01"))

dim(lgs8612)

#> [1] 7044 2

lgs8612m <- aggregate(lgs8612, as.Date(as.yearmon(time(lgs8612))), mean)

plot(lgs8612m)

dim(lgs8612m)

#> [1] 324 2

VARselect(lgs8612m, 5)

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 3 2 2 3

#>

#> $criteria

#> 1 2 3 4 5

#> AIC(n) -1.274002e+01 -1.279067e+01 -1.279473e+01 -1.278206e+01 -1.276537e+01

#> HQ(n) -1.271174e+01 -1.274353e+01 -1.272874e+01 -1.269721e+01 -1.266167e+01

#> SC(n) -1.266920e+01 -1.267264e+01 -1.262949e+01 -1.256960e+01 -1.250570e+01

#> FPE(n) 2.931433e-06 2.786669e-06 2.775388e-06 2.810831e-06 2.858202e-06

#>

gs2 <- VAR(lgs8612m, 2)

summary(gs2)

#>

#> VAR Estimation Results:

#> =========================

#> Endogenous variables: gold, silver

#> Deterministic variables: const

#> Sample size: 322

#> Log Likelihood: 1157.62

#> Roots of the characteristic polynomial:

#> 1.006 0.9157 0.249 0.1188

#> Call:

#> VAR(y = lgs8612m, p = 2)

#>

#>

#> Estimation results for equation gold:

#> =====================================

#> gold = gold.l1 + silver.l1 + gold.l2 + silver.l2 + const

#>

#> Estimate Std. Error t value Pr(>|t|)

#> gold.l1 1.06084 0.07385 14.364 <2e-16 ***

#> silver.l1 0.03858 0.04120 0.936 0.350

#> gold.l2 -0.06034 0.07376 -0.818 0.414

#> silver.l2 -0.03454 0.04095 -0.844 0.400

#> const -0.02096 0.02385 -0.879 0.380

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#>

#> Residual standard error: 0.03519 on 317 degrees of freedom

#> Multiple R-Squared: 0.9952, Adjusted R-squared: 0.9951

#> F-statistic: 1.644e+04 on 4 and 317 DF, p-value: < 2.2e-16

#>

#>

#> Estimation results for equation silver:

#> =======================================

#> silver = gold.l1 + silver.l1 + gold.l2 + silver.l2 + const

#>

#> Estimate Std. Error t value Pr(>|t|)

#> gold.l1 -0.21844 0.12996 -1.681 0.0938 .

#> silver.l1 1.22837 0.07250 16.942 < 2e-16 ***

#> gold.l2 0.29021 0.12980 2.236 0.0261 *

#> silver.l2 -0.28535 0.07206 -3.960 9.26e-05 ***

#> const -0.07413 0.04198 -1.766 0.0784 .

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#>

#> Residual standard error: 0.06192 on 317 degrees of freedom

#> Multiple R-Squared: 0.9893, Adjusted R-squared: 0.9892

#> F-statistic: 7343 on 4 and 317 DF, p-value: < 2.2e-16

#>

#>

#>

#> Covariance matrix of residuals:

#> gold silver

#> gold 0.001238 0.001442

#> silver 0.001442 0.003834

#>

#> Correlation matrix of residuals:

#> gold silver

#> gold 1.000 0.662

#> silver 0.662 1.000

#>

#>

summary(gs2)$covres

#> gold silver

#> gold 0.001238045 0.001442211

#> silver 0.001442211 0.003834060

## ACF of residuals, p.256

acf(resid(gs2), 2, plot = FALSE)

#>

#> Autocorrelations of series ‘resid(gs2)’, by lag

#>

#> , , gold

#>

#> gold silver

#> 1.000 ( 0) 0.662 ( 0)

#> 0.015 ( 1) 0.012 (-1)

#> -0.138 ( 2) -0.099 (-2)

#>

#> , , silver

#>

#> gold silver

#> 0.662 ( 0) 1.000 ( 0)

#> 0.005 ( 1) 0.018 ( 1)

#> -0.088 ( 2) -0.120 ( 2)

#>

# \donttest{

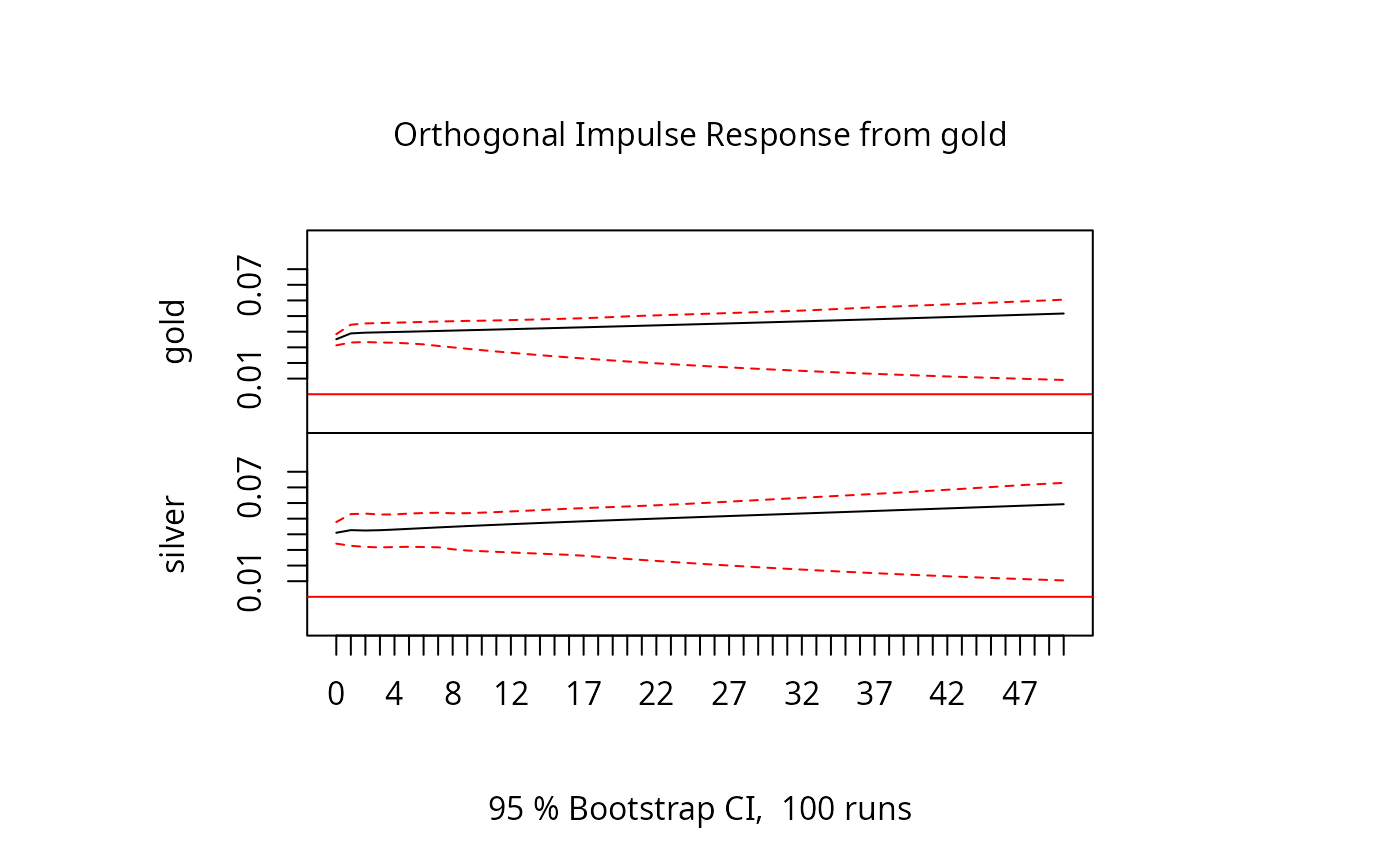

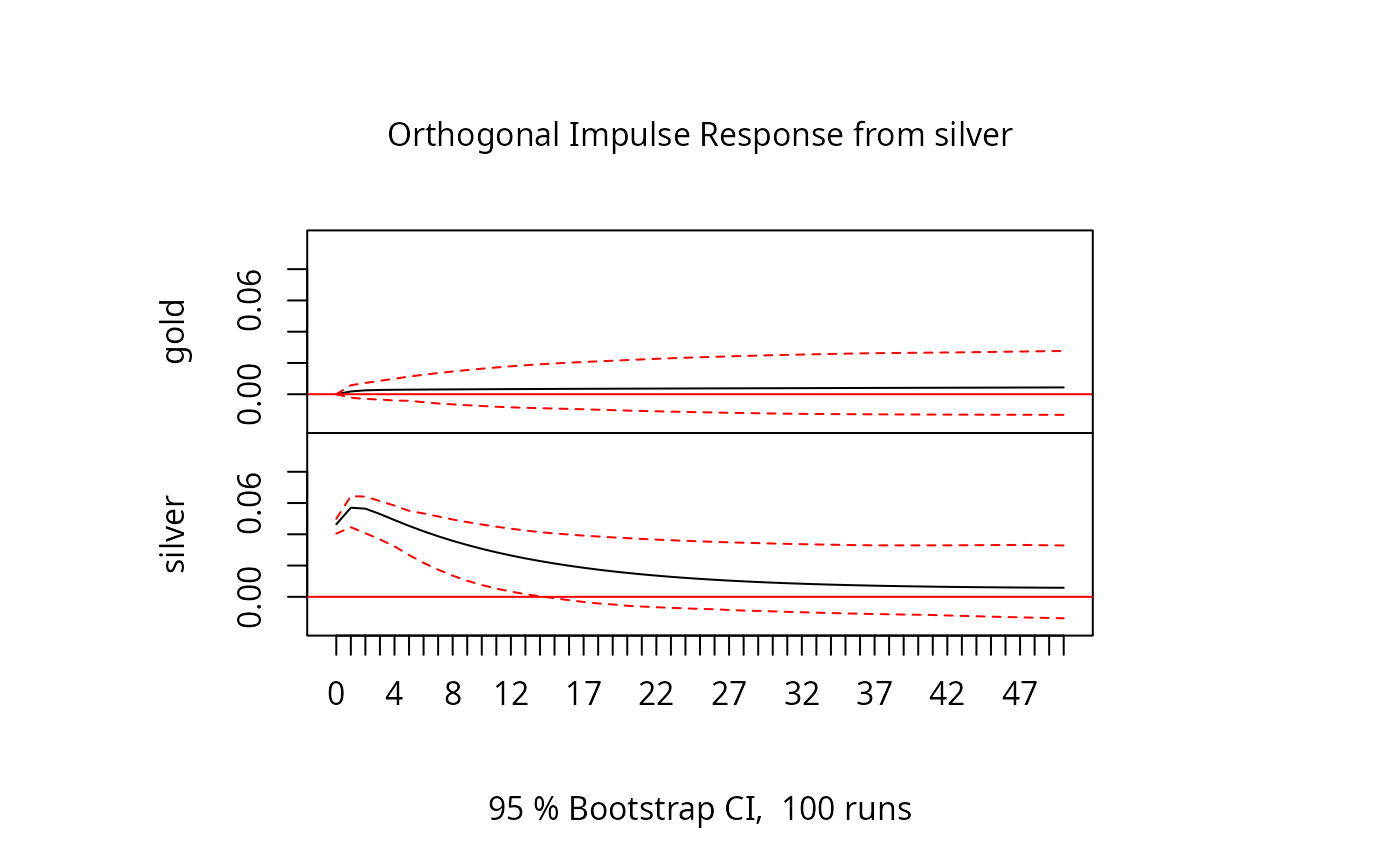

## Figure 9.1, p.260 (somewhat different)

plot(irf(gs2, impulse = "gold", n.ahead = 50), ylim = c(-0.02, 0.1))

dim(lgs8612m)

#> [1] 324 2

VARselect(lgs8612m, 5)

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 3 2 2 3

#>

#> $criteria

#> 1 2 3 4 5

#> AIC(n) -1.274002e+01 -1.279067e+01 -1.279473e+01 -1.278206e+01 -1.276537e+01

#> HQ(n) -1.271174e+01 -1.274353e+01 -1.272874e+01 -1.269721e+01 -1.266167e+01

#> SC(n) -1.266920e+01 -1.267264e+01 -1.262949e+01 -1.256960e+01 -1.250570e+01

#> FPE(n) 2.931433e-06 2.786669e-06 2.775388e-06 2.810831e-06 2.858202e-06

#>

gs2 <- VAR(lgs8612m, 2)

summary(gs2)

#>

#> VAR Estimation Results:

#> =========================

#> Endogenous variables: gold, silver

#> Deterministic variables: const

#> Sample size: 322

#> Log Likelihood: 1157.62

#> Roots of the characteristic polynomial:

#> 1.006 0.9157 0.249 0.1188

#> Call:

#> VAR(y = lgs8612m, p = 2)

#>

#>

#> Estimation results for equation gold:

#> =====================================

#> gold = gold.l1 + silver.l1 + gold.l2 + silver.l2 + const

#>

#> Estimate Std. Error t value Pr(>|t|)

#> gold.l1 1.06084 0.07385 14.364 <2e-16 ***

#> silver.l1 0.03858 0.04120 0.936 0.350

#> gold.l2 -0.06034 0.07376 -0.818 0.414

#> silver.l2 -0.03454 0.04095 -0.844 0.400

#> const -0.02096 0.02385 -0.879 0.380

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#>

#> Residual standard error: 0.03519 on 317 degrees of freedom

#> Multiple R-Squared: 0.9952, Adjusted R-squared: 0.9951

#> F-statistic: 1.644e+04 on 4 and 317 DF, p-value: < 2.2e-16

#>

#>

#> Estimation results for equation silver:

#> =======================================

#> silver = gold.l1 + silver.l1 + gold.l2 + silver.l2 + const

#>

#> Estimate Std. Error t value Pr(>|t|)

#> gold.l1 -0.21844 0.12996 -1.681 0.0938 .

#> silver.l1 1.22837 0.07250 16.942 < 2e-16 ***

#> gold.l2 0.29021 0.12980 2.236 0.0261 *

#> silver.l2 -0.28535 0.07206 -3.960 9.26e-05 ***

#> const -0.07413 0.04198 -1.766 0.0784 .

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#>

#> Residual standard error: 0.06192 on 317 degrees of freedom

#> Multiple R-Squared: 0.9893, Adjusted R-squared: 0.9892

#> F-statistic: 7343 on 4 and 317 DF, p-value: < 2.2e-16

#>

#>

#>

#> Covariance matrix of residuals:

#> gold silver

#> gold 0.001238 0.001442

#> silver 0.001442 0.003834

#>

#> Correlation matrix of residuals:

#> gold silver

#> gold 1.000 0.662

#> silver 0.662 1.000

#>

#>

summary(gs2)$covres

#> gold silver

#> gold 0.001238045 0.001442211

#> silver 0.001442211 0.003834060

## ACF of residuals, p.256

acf(resid(gs2), 2, plot = FALSE)

#>

#> Autocorrelations of series ‘resid(gs2)’, by lag

#>

#> , , gold

#>

#> gold silver

#> 1.000 ( 0) 0.662 ( 0)

#> 0.015 ( 1) 0.012 (-1)

#> -0.138 ( 2) -0.099 (-2)

#>

#> , , silver

#>

#> gold silver

#> 0.662 ( 0) 1.000 ( 0)

#> 0.005 ( 1) 0.018 ( 1)

#> -0.088 ( 2) -0.120 ( 2)

#>

# \donttest{

## Figure 9.1, p.260 (somewhat different)

plot(irf(gs2, impulse = "gold", n.ahead = 50), ylim = c(-0.02, 0.1))

plot(irf(gs2, impulse = "silver", n.ahead = 50), ylim = c(-0.02, 0.1))

plot(irf(gs2, impulse = "silver", n.ahead = 50), ylim = c(-0.02, 0.1))

# }

## Table 9.2, p.261

fevd(gs2)

#> $gold

#> gold silver

#> [1,] 1.0000000 0.000000000

#> [2,] 0.9988365 0.001163524

#> [3,] 0.9978125 0.002187521

#> [4,] 0.9971173 0.002882671

#> [5,] 0.9966392 0.003360835

#> [6,] 0.9962898 0.003710162

#> [7,] 0.9960192 0.003980766

#> [8,] 0.9957996 0.004200378

#> [9,] 0.9956151 0.004384942

#> [10,] 0.9954559 0.004544131

#>

#> $silver

#> gold silver

#> [1,] 0.4381897 0.5618103

#> [2,] 0.3930838 0.6069162

#> [3,] 0.3817063 0.6182937

#> [4,] 0.3845103 0.6154897

#> [5,] 0.3938363 0.6061637

#> [6,] 0.4063921 0.5936079

#> [7,] 0.4206183 0.5793817

#> [8,] 0.4357010 0.5642990

#> [9,] 0.4511753 0.5488247

#> [10,] 0.4667546 0.5332454

#>

## p.266

ls <- lgs8612[, "silver"]

lg <- lgs8612[, "gold"]

gsreg <- lm(lg ~ ls)

summary(gsreg)

#>

#> Call:

#> lm(formula = lg ~ ls)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.40097 -0.10317 -0.00179 0.10857 0.33631

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.971967 0.015506 62.68 <2e-16 ***

#> ls 0.816752 0.002732 298.92 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.1362 on 7042 degrees of freedom

#> Multiple R-squared: 0.9269, Adjusted R-squared: 0.9269

#> F-statistic: 8.935e+04 on 1 and 7042 DF, p-value: < 2.2e-16

#>

sgreg <- lm(ls ~ lg)

summary(sgreg)

#>

#> Call:

#> lm(formula = ls ~ lg)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.3619 -0.1284 0.0074 0.1256 0.5188

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.690802 0.021278 -32.47 <2e-16 ***

#> lg 1.134917 0.003797 298.92 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.1605 on 7042 degrees of freedom

#> Multiple R-squared: 0.9269, Adjusted R-squared: 0.9269

#> F-statistic: 8.935e+04 on 1 and 7042 DF, p-value: < 2.2e-16

#>

library("tseries")

adf.test(resid(gsreg), k = 0)

#>

#> Augmented Dickey-Fuller Test

#>

#> data: resid(gsreg)

#> Dickey-Fuller = -3.4284, Lag order = 0, p-value = 0.04912

#> alternative hypothesis: stationary

#>

adf.test(resid(sgreg), k = 0)

#>

#> Augmented Dickey-Fuller Test

#>

#> data: resid(sgreg)

#> Dickey-Fuller = -3.6544, Lag order = 0, p-value = 0.02734

#> alternative hypothesis: stationary

#>

# }

## Table 9.2, p.261

fevd(gs2)

#> $gold

#> gold silver

#> [1,] 1.0000000 0.000000000

#> [2,] 0.9988365 0.001163524

#> [3,] 0.9978125 0.002187521

#> [4,] 0.9971173 0.002882671

#> [5,] 0.9966392 0.003360835

#> [6,] 0.9962898 0.003710162

#> [7,] 0.9960192 0.003980766

#> [8,] 0.9957996 0.004200378

#> [9,] 0.9956151 0.004384942

#> [10,] 0.9954559 0.004544131

#>

#> $silver

#> gold silver

#> [1,] 0.4381897 0.5618103

#> [2,] 0.3930838 0.6069162

#> [3,] 0.3817063 0.6182937

#> [4,] 0.3845103 0.6154897

#> [5,] 0.3938363 0.6061637

#> [6,] 0.4063921 0.5936079

#> [7,] 0.4206183 0.5793817

#> [8,] 0.4357010 0.5642990

#> [9,] 0.4511753 0.5488247

#> [10,] 0.4667546 0.5332454

#>

## p.266

ls <- lgs8612[, "silver"]

lg <- lgs8612[, "gold"]

gsreg <- lm(lg ~ ls)

summary(gsreg)

#>

#> Call:

#> lm(formula = lg ~ ls)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.40097 -0.10317 -0.00179 0.10857 0.33631

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.971967 0.015506 62.68 <2e-16 ***

#> ls 0.816752 0.002732 298.92 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.1362 on 7042 degrees of freedom

#> Multiple R-squared: 0.9269, Adjusted R-squared: 0.9269

#> F-statistic: 8.935e+04 on 1 and 7042 DF, p-value: < 2.2e-16

#>

sgreg <- lm(ls ~ lg)

summary(sgreg)

#>

#> Call:

#> lm(formula = ls ~ lg)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.3619 -0.1284 0.0074 0.1256 0.5188

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.690802 0.021278 -32.47 <2e-16 ***

#> lg 1.134917 0.003797 298.92 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Residual standard error: 0.1605 on 7042 degrees of freedom

#> Multiple R-squared: 0.9269, Adjusted R-squared: 0.9269

#> F-statistic: 8.935e+04 on 1 and 7042 DF, p-value: < 2.2e-16

#>

library("tseries")

adf.test(resid(gsreg), k = 0)

#>

#> Augmented Dickey-Fuller Test

#>

#> data: resid(gsreg)

#> Dickey-Fuller = -3.4284, Lag order = 0, p-value = 0.04912

#> alternative hypothesis: stationary

#>

adf.test(resid(sgreg), k = 0)

#>

#> Augmented Dickey-Fuller Test

#>

#> data: resid(sgreg)

#> Dickey-Fuller = -3.6544, Lag order = 0, p-value = 0.02734

#> alternative hypothesis: stationary

#>